Case Study

The impact of Relationship Marketing on Brand Equity in the Banking Sector in Iran

- Abstract

- Full text

- Metrics

During the last few decades, business philosophy has shifted from marketing orientation to Relationship Marketing Orientation (RMO). Service oriented organizations, such as banks, increasingly apply RMO to enhance their brand management practices, such as brand loyalty and brand image. The main purpose of this study is to investigate the influence of relationship marketing orientation and its dimensions (trust, bonding, communication, shared values, empathy and reciprocity) on the Brand Equity in Saderat Bank. Data were collected from 339 customers across various branches of Saderat Bank in Ardabil, Iran. Confirmatory factor analysis and structural equation modeling were used to analyze the measurements and relationships among the variables. The findings of this study demonstrate that RMO has a positive effect on the brand equity of Saderat Bank. Specifically, dimensions including trust, bonding, empathy, and reciprocity have direct and significant effects on brand equity, with the effect of trust being significantly higher. However, communication and shared values showed no significant effects on brand equity. The findings of this study offer practical applications for enhancing the brand equity of banks and other financial institutions, particularly Islamic banks, by exploring the cultural variation of relationship marketing.

The impact of Relationship Marketing on Brand Equity in the Banking Sector in Iran

Farzad S. Ardabili1,*, Leon Vratar2, Petra Cajnko2

1 Department of Management, Ard.C., Islamic Azad University, Ardabil, Iran

2 University of Maribor, Faculty of Natural Sciences and Mathematics, Slovenia

ABSTRACT

During the last few decades, business philosophy has shifted from marketing orientation to Relationship Marketing Orientation (RMO). Service oriented organizations, such as banks, increasingly apply RMO to enhance their brand management practices, such as brand loyalty and brand image. The main purpose of this study is to investigate the influence of relationship marketing orientation and its dimensions (trust, bonding, communication, shared values, empathy and reciprocity) on the Brand Equity in Saderat Bank. Data were collected from 339 customers across various branches of Saderat Bank in Ardabil, Iran. Confirmatory factor analysis and structural equation modeling were used to analyze the measurements and relationships among the variables. The findings of this study demonstrate that RMO has a positive effect on the brand equity of Saderat Bank. Specifically, dimensions including trust, bonding, empathy, and reciprocity have direct and significant effects on brand equity, with the effect of trust being significantly higher. However, communication and shared values showed no significant effects on brand equity. The findings of this study offer practical applications for enhancing the brand equity of banks and other financial institutions, particularly Islamic banks, by exploring the cultural variation of relationship marketing.

KEYWORDS: Relationship Marketing Orientation, Brand Equity, Saderat Bank, Perceived Quality,

In recent years, as digital technologies and social media have advanced, banks have adopted various marketing strategies to gain a competitive edge. Aligning with environmental shifts, they aim to enhance their brand positioning by fostering stronger relationships with their customers. These environmental transformations have propelled service-oriented institutions toward virtualization, resulting in a continuous decline in direct, face-to-face interactions between customers and service providers. Banks are no exception to this trend; they strive to leverage customer connections by any possible means to establish sustainable interactions. The aggressive competitive strategies of various banks make long-term customer retention exceedingly challenging. Consequently, within this highly volatile and competitive landscape, banks find it imperative to develop diverse methodologies for long-term customer retention, going beyond mere service provision aimed at customer acquisition (Jang et al., 2021; Wongsansukcharoen, 2022). To sustain such bilateral relationships, mechanisms must be implemented that ensure mutual benefit, encouraging both parties to maintain the long-term relationship (Alrubaiee & Al-Nazer, 2010; Yoganathan et al., 2015) and ultimately yielding a competitive advantage. Given its strategic role within an organization and its capacity to generate a competitive advantage, brand equity is of paramount importance. This role becomes even more valuable in the service sector, where unique characteristics emerge as a direct result of employee-customer interactions. Consequently, organizations such as banks can utilize brand equity as a powerful tool to build a sustainable competitive advantage.

Almost all employees and customers have prior experience interacting with one another, providing banks with a critical opportunity to focus on establishing mutually beneficial, reciprocal relationships. Contemporary customers have unprecedented access to information; by easily comparing the services of various banks and financial institutions, they can readily switch to competitors. Therefore, while rival banks may employ other marketing strategies linked to their brand equity, relationship marketing can be applied directly to individual customers. This provides a distinct opportunity for banks to create and continuously enhance value by exerting a direct, personalized influence on each customer (So & Speece, 2000; Yoganathan et al., 2015).

In light of the aforementioned points, a primary challenge currently facing most financial institutions is identifying strategies to enhance customer brand loyalty, understand perceived service quality, and retain existing customers. The present study investigates the relationship between brand equity and relationship marketing in the banking sector, aiming to assist banks and financial institutions in establishing long-term relationships with their clientele. Furthermore, the proliferation of financial institutions and escalating competition highlight the critical importance of developing relationship marketing, alongside other strategic initiatives, within an environment that is continuously transitioning toward virtual service delivery.

Literature Review

Relationship marketing encompasses a set of activities aimed at forging long-term, mutually beneficial bonds between an organization and its customers (Rosário & Casaca, 2023). Fundamentally, it represents a paradigm shift from a traditional marketing approach toward a relationship-centric one (Ferrell et al., 2010), where focuses is on the creation and maintenance of the relationship between the two parties to an exchange, i.e., supplier and consumer, through developing the desire to be mutually empathic, reciprocal, and to trust and form bonds (Hau & Ngo, 2012).

Following its introduction by Berry (1983), relationship marketing quickly attracted the attention of marketing researchers. Its conceptual foundation, built upon the three constructs of attracting, maintaining, and enhancing, has been widely incorporated into the service marketing strategies of numerous service providers (Colgate & Danaher, 2000; Sayil et al., 2019). Banks, in particular, recognizing the critical impact of customer satisfaction on repeat service patronage, adopted the relationship marketing approach to survive in the competitive financial market (Ogbechi et al., 2018) and to improve brand equity through the establishment of long-term customer relationships (Fatema et al., 2013; Razavi et al., 2025).

In the highly competitive financial services industry, building strong relational ties establishes mutual trust and commitment, both of which are critical psychological antecedents to a robust and valuable brand image (Mukerjee, 2018). Furthermore, when banks employ effective relationship marketing tactics; such as personalized communication, customized financial solutions, and proactive conflict resolution, they significantly elevate the customers’ perceived quality and foster deep brand loyalty (Ranjbarian et al., 2012).

Although some studies have indicated that relationship marketing has no effect on bank customers’ loyalty and satisfaction (Djajanto et al., 2019), in general, the relationship marketing approach fosters repeat interactions and builds trust by engaging customers in the service delivery process (Wongsansukcharoen, 2022). Trust and perceived quality are fundamental components of brand equity. Consequently, sustained relational efforts ensure customers feel valued, leading to enduring brand resonance (Monfort et al., 2025) that ultimately translates into a sustainable competitive advantage and higher overall brand equity for the bank. Therefore, RMO provides the strategic relational framework necessary to build this value through its six core constructs: trust, communication, bonding, shared values, empathy, and reciprocity (Sin et al., 2005).

The foundation of robust brand equity relies heavily on trust and shared values. Trust minimizes perceived customer risk and enhances brand credibility, which directly drives brand loyalty; a primary dimension of brand equity (Loureiro & Sarmento, 2018; van Esterik-Plasmeijer & Van Raaij, 2017). Similarly, when a brand and its consumers possess shared values, it fosters positive brand associations and deepens consumer-brand identification (Rather et al., 2018; Santos et al., 2022; Tran et al., 2024).

Furthermore, communication and empathy are critical for building a favorable brand image and perceived quality (Monfort et al., 2025), and brand image and brand love have significat role in relationship with customers loyalty (Turk, 2021). The results of loyal customer is the base for creating favourable brand associations (Oyenuga & Vu, 2024). In banking, effective RMO tactics such as personalized communication, proactive conflict resolution, and customized financial solutions demonstrate empathy, showing that the institution understands the customer’s specific financial goals (Ranjbarian et al., 2012; Veloutsou, 2015). This emotional resonance easily translates into strong brand preference.

Finally, bonding and reciprocity transform casual companies’ clients into dedicated brand advocates. Structural and emotional bonding create psychological barriers to switching, solidifying brand resonance and customer retention in a market flooded with alternatives (Biedenbach et al., 2011; Mathur, 2024). Concurrently, reciprocity ensures that customers feel their ongoing loyalty is mutually rewarded by the bank (Teichmann, 2021; Yau et al., 2000). Reciprocity is grounded in Social Exchange Theory, which posits that social behavior is the result of an exchange process aimed at maximizing benefits and minimizing costs (Ahmad et al., 2023).

Therefore, the research hypothesis can be stated as follows:

H1: Relationship marketing has a direct positive effect on brand equity

H1a: Trust has a direct positive effect on brand equity

H1b: Bonding has a direct positive effect on brand equity

H1c: Communication has a direct positive effect on brand equity

H1d: Shared values have a direct positive effect on brand equity

H1e: Empathy has a direct positive effect on brand equity

H1f : Reciprocity has a direct positive effect on brand equity

Method

Sample and Procedure

To collect research data from the target population, individuals holding an account at one of Bank Saderat's Ardabil branches, a link to the questionnaire was randomly sent to 840 individuals via virtual networks. Prior to the main survey items, the questionnaire included a screening question asking respondents whether they held an account with Bank Saderat and were customers of that bank. Only those who answered “yes” were permitted to proceed with the remaining questions. From these individuals, who were members of various social media groups such as WhatsApp, a total of 351 responses were received, out of which 339 questionnaires were completed correctly and deemed valid. The first section of the questionnaire consisted of demographic questions, including gender, age, and education level. The second section encompassed items pertaining to relationship marketing and brand equity.

The demographic characteristics of the respondents (N = 339) were analyzed based on gender, age, education level, and the number of years holding an account with the bank. Regarding gender, the sample was predominantly male, comprising 79.6 (n = 270) of the respondents, while females accounted for the remaining 20.4 (n = 69). In terms of age, the largest segment of participants fell into the 30 to 40 age range (n = 133, 39.2), followed by those younger than 30 (n = 93, 27.4). Participants aged 40 to 50 accounted for 20.4 (n = 69) of the sample, and those aged 50 and older represented the smallest age group at 13.0 (n = 44). The participants' educational backgrounds showed that the highest proportion of respondents held a Master’s degree (MSc) (n = 116, 34.2), followed by those with a Diploma (n = 113, 33.3). Participants holding a Bachelor’s degree accounted for 19.5 (n = 66), and those with a Ph.D. made up 13.0 (n = 44) of the sample.

Finally, regarding the duration of participants’ relationship with the bank, the largest group had held an account for less than 5 years (n = 145, 42.8). Those with an account duration of 5-10 years comprised 31.3% (n = 106) of the sample. Long-term customers holding accounts for 10 to 15 years and for more than 15 years represented 13.9 (n = 47) and 12.1 (n = 41), respectively, of the respondents.

Instrument

Relationship marketing . To measure relationship marketing, the instrument developed by Sin et al. (2005) was utilized. This scale consists of 4 items measuring trust, 4 measuring commitment, 3 measuring the communication dimension, 4 assessing empathy, and 3 assessing reciprocity. This questionnaire has been employed in various studies within Iran, and the validity and reliability of its Persian version have been confirmed (Mohammadian & Aslani Afrashteh, 2022). The items are provided in Appendix A.

Brand Equity. To measure brand equity, the scale developed by Kim et al. (2005) was employed. This instrument comprises three dimensions: brand loyalty, brand image, and perceived quality. Respondents evaluated the statements pertaining to all three dimensions using a scale ranging from “strongly disagree” to “strongly agree.” Specifically, 6 items were used to measure brand loyalty, while 8 items were utilized for each of the perceived quality and brand image dimensions (Appendix A).

Results

Preliminary Analysis

Table 1 displays the means, standard deviations, and correlation coefficients of the variables. Consistent with the literature, brand equity has a significant and positive relationship with all constructs of relationship marketing and a negative relationship with participants' gender (r = -.12, p < .05) and a positive relationship with years of relationship (r = .19, p < .01). In this study, the effects of gender and years of relationship on brand equity were controlled.

Correlation Index between Variables

|

Variables |

M |

SD |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

|

Gender |

1.20 |

.40 |

— |

|

|

|

|

|

|

|

|

Years of relationship |

9.25 |

1.02 |

-.09 |

— |

|

|

|

|

|

|

|

Trust |

4.13 |

.75 |

-.08 |

.06 |

— |

|

|

|

|

|

|

Bonding |

4.03 |

.73 |

-.12* |

.16** |

.67** |

— |

|

|

|

|

|

Communication |

3.78 |

.85 |

-.15** |

.21** |

.54** |

.64** |

— |

|

|

|

|

Shared values |

3.68 |

.86 |

-.09 |

.18** |

.53** |

.63** |

.64** |

— |

|

|

|

Empathy |

3.59 |

.99 |

-.11* |

.17** |

.55** |

.62** |

.63** |

.72** |

.— |

|

|

Reciprocity |

3.92 |

.98 |

-.10* |

.16** |

.50** |

.57** |

.47** |

.58** |

.64** |

— |

|

Brand Equity |

3.92 |

.67 |

-.12* |

.19** |

.69** |

.71** |

.63** |

.65** |

.72** |

.62** |

To examine the constructs and the validity and reliability of each variable, a Confirmatory Factor Analysis (CFA) was conducted. Table 2 shows the obtained factor loadings for each item. According to the results, all items had factor loadings higher than .5, except for one brand loyalty item, which had a factor loading of .22 and was subsequently excluded from the analysis. The Cronbach’s alpha and Composite Reliability results for all constructs are higher than .7, indicating that all constructs are internally consistent. The Average Variance Extracted (AVE) results for all constructs were also higher than .5.

Validity of the Constructs and Factor Loadings of the Items

|

Construct |

Items |

Loading |

|

Trust AVE (.77), CR (.93), rho_A = .90 α = .90 |

I trust Saderat bank |

.89 |

|

Saderat bank is reliable |

.91 |

|

|

The policies and practices of Saderat bank are trustworthy and practices of Saderat bank are trustworthy |

.88 |

|

|

The service processes of Saderat bank ensure customers’ privacy |

.83 |

|

|

Bonding AVE (.72), CR (.91), rho_A = .87 α = .87 |

|

|

|

We rely on each other |

.79 |

|

|

We try to establish a long-term relationship |

.88 |

|

|

We work in close cooperation |

.86 |

|

|

We keep in touch constantly |

.86 |

|

|

Communication AVE (.75), CR (.90), rho_A = .84 α = .84 |

We frequently communicate and express our opinions to each other We can show our discontent towards each other via communication We can communicate honestly |

.87 .86 .87 |

|

Shared values AVE (.71), CR (.90), rho_A = .86 α = .86 |

We share the same worldview We share the same opinions in many aspects We share the same values I have relationship with my bank because of its good values |

.89 .87 .86 .73 |

|

Empathy AVE (.81), CR (.92), rho_A = .88 α = .88 |

My bank always looks things from customers’ view My bank knows how others feel My bank cares about customers’ feelings |

.88 .90 .91 |

|

Reciprocity AVE (.57), CR (.79), rho_A = .70 α = .70 |

My bank regards “never forget a good turn” as its business slogan. My bank keeps its promises to others in any situation If customers gave assistance to the bank, bank's staff would repay their kindness |

.52 .86 .83 |

|

Brand Loyalty AVE (.57), CR (.85), rho_A = .88 α = .77 |

I regularly go to this bank I have the intention to stay with this bank I usually consider this bank as my first choice compared to other banks I would recommend this bank to others I would prefer to switch to a next popular bank (reverse coded) The bank's staff treat me as a special and valued customer |

.85 .85 .85 .82 n.a .74

|

|

Construct |

Items |

Loading |

|

Perceived Quality AVE (.61), CR (.92), rho_A = .91 α = .91 |

My bank implements the up-to-date facilities The bank provides its services at promised times The bank staff quickly handle customers’ complaints The bank gives more facilities to its customers The staff's knowledge and confidence are adequate The bank services are consistent with customers’ expectations The bank staff understand my special needs and serve me The bank is convenient to access |

.78 .80 .80 .82 .80 .81 .78 .66 |

|

Brand Image AVE (.59), CR (.92), rho_A = .90 α = .90 |

The bank provides a high level of service The bank solves my problems relating to bank This bank suits any class of people I feel something unique in this bank The bank has enough branches to serve its customers The bank has a long history The image of this bank is distinctive from that of other banks My bank's name is familiar to me |

.81 .78 .79 .79 .69 .69 .83 .77 |

Table 3 presents the results of the Fornell-Larcker criterion. According to Table 3, all research constructs demonstrate discriminant validity. And the square root of the average variance extracted by a construct is greater than the correlation between the construct and any other construct in the relevant rows and columns.

Discriminant Validity of the Scale

|

|

|

Fornell–Larcker criterion |

|

|

|||||

|

Variables |

Bonding |

Brand Image |

Brand loyalty |

Communication |

Empathy |

Perceived Quality |

Reciprocity |

Shared values |

Trust |

|

Bonding |

.85 |

|

|

|

|

|

|

|

|

|

Brand Image |

.64 |

.77 |

|

|

|

|

|

|

|

|

Brand Loyalty |

.69 |

.76 |

.82 |

|

|

|

|

|

|

|

Communication |

.64 |

.56 |

.61 |

.87 |

|

|

|

|

|

|

Empathy |

.62 |

.65 |

.64 |

.63 |

.90 |

|

|

|

|

|

Perceived Quality |

.66 |

.84 |

.80 |

.61 |

.69 |

.78 |

|

|

|

|

Reciprocity |

.68 |

.64 |

.71 |

.59 |

.73 |

.69 |

.75 |

|

|

|

Shared values |

.63 |

.60 |

.58 |

.64 |

.72 |

.64 |

.68 |

.84 |

|

|

Trust |

.67 |

.63 |

.64 |

.54 |

.55 |

.66 |

.59 |

.54 |

.88 |

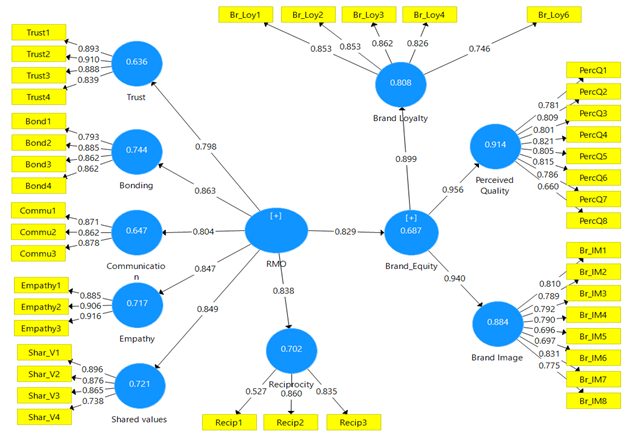

According to the findings presented in Table 4 and Figure 1, Relationship Marketing had a significant impact on BE (β = .82, t = 39.12, p < .01). Similar results also achieved when analyzing the effects of relationship marketing constructs on brand equity. Trust (β = .26, t = 5.43, p < .000), bonding (β = .15, t = 2.85, p < .004), empathy (β = .22, t = 3.41, p < .01), and reciprocity (β = .22, t = 4.01, p < .000), all demonstrated significant positive effects on brand equity.

However, communication did not have a statistically significant effect on brand equity at the .05 significance level (B = .08, t = 1.80, p = .07), although the coefficient indicates a positive direction. Likewise, shared values did not show a positive significant relationship with brand equity (B = .05, t = .88, p = .37).

Regression Analysis

Table 4

Regression Results

|

Variable |

B |

Std. error |

t |

p |

|

|

RMO -> Brand Equity |

.82 |

.02 |

39.12 |

.000 |

H1 Supported |

|

Trust -> Brand Equity |

.26 |

.04 |

5.43 |

.000 |

Supported |

|

Bonding -> Brand Equity |

.15 |

.05 |

2.85 |

.004 |

Supported |

|

Communication -> Brand Equity |

.08 |

.04 |

1.80 |

.071 |

Not Supported |

|

Empathy -> Brand Equity |

.22 |

.06 |

3.41 |

.000 |

Supported |

|

Shared values -> Brand Equity |

.05 |

.05 |

0.88 |

.375 |

Not Supported |

|

Reciprocity -> Brand Equity |

.22 |

.05 |

4.01 |

.000 |

Supported |

|

Note. N = 339 |

|||||

Discussion and Conclusion

The objective of this study is to investigate the impact of relationship marketing on the brand equity of Bank Saderat, an Islamic bank operating in Iran. The findings indicate that relationship marketing orientation exerts a positive and significant effect on brand equity. These results are consistent with prior literature (Mohammadian & Aslani Afrashteh, 2022; Yoganathan, 2015) and demonstrate that banks can substantially enhance their brand equity by adopting a relationship-oriented approach.

Furthermore, the impact of the various dimensions of relationship marketing on the brand equity of Bank Saderat was examined. Among these dimensions, trust exhibited the most substantial positive and significant effect on brand equity (B = .26). This finding aligns with prior research (Ogbechi et al., 2018; Sayil et al., 2019; Eskandari et al., 2017; Yoganathan et al., 2015), underscoring the critical importance of cultivating customer trust. Consequently, banks must formulate targeted strategies to establish, maintain, and continuously enhance trust with their clientele. However, it should be noted that the origins of this trust within the context of the current study may also stem from factors such as the religious nature of the bank, and are not necessarily exclusively tied to service quality (Wahyoedi, 2021).

Similarly, empathy demonstrated an approximately equivalent effect of .22 on brand equity. This suggests that when employees exhibit empathy, such as allocating time to genuinely comprehend customer needs, customers develop enhanced trust and perceive lower levels of risk (Morgan & Hunt, 1994). This trust and relational engagement subsequently fortify and elevate the bank’s brand (Yoganathan et al., 2015). Ultimately, by observing the empathetic disposition of the bank’s personnel, customers feel valued and perceive themselves as significant to the institution; this dynamic leads to a heightened emotional attachment and positively reinforces the customer’s overall perception of the bank’s brand equity (Yoganathan et al., 2015).

Reciprocity involves the mutual exchange of value, which in the bank means the customer provides patronage, data, and loyalty, and in return the bank provides rewards, preferential rates, or specialized services. Therefore, reciprocal actions by a bank (e.g., waiving a fee for a long-term customer, offering loyalty-based interest rate bumps) signal fairness and relational investment to the consumer. This behavior significantly enhances the “perceived quality” dimension of brand equity, as customers perceive the service as of higher value than competitors' (Chen & Myagmarsuren, 2011). This process also creates a psychological contract between the bank and the customer. When a bank demonstrates reciprocal behavior, customers feel an intrinsic obligation to maintain the relationship and value this relationship, which is related to brand equity. This reciprocal loop solidifies brand loyalty, which is widely considered the core driver of brand equity (Chen & Myagmarsuren, 2011) because it guarantees future revenue streams and reduces marketing costs.

Communication and shared values had no significant impact on brand equity. Contrary to the findings of Yoganathan et al. (2015) and Sayil et al. (2019), responses from Bank Saderat customers did not support the impact of these two variables on brand equity. One possible reason is the uniform application of communication methods across other banks, which leads to a lack of perceived differentiation among customers; consequently, they do not perceive any substantial difference in this regard. In contrast, Sayil et al. (2019), who conducted their study in a Muslim society, found that relationship marketing effectively influenced bank brand equity because it was rooted in trust and communication between the bank and its customers.

Bank customers may frequently utilize banking services; if these repeated interactions extend across various types of services, it could indicate that the foundational factors of this relationship, such as trust and communication, have been properly established between the customer and the bank. Therefore, in the present study, the inability of communication to serve as a significant predictor of brand equity—despite its expected high correlation with trust—may stem from other factors, including content-related issues. This is because the mere repetition of utilizing bank services does not necessarily imply loyalty or the establishment of a relationship, and may be driven by other motives (Kumar et al., 2003). In particular, the lack of impact of shared values suggests that the bank’s intended values were not effectively communicated to customers, and customer perceptions were not aligned with the bank’s target values. Therefore, Bank Saderat must conduct a more rigorous assessment of the quality and content of its customer communications to develop strategies that foster shared values and enhance communication effectiveness by increasing customer engagement.

The significant effects of effective relationship marketing constructs on a bank’s equity brand indicate that cognitive and emotional relationship investments are critical drivers of brand value. Emotional, structural, and behavioral foundations shift the customer’s perception of the bank from a mere financial utility to a trusted financial partner, thereby elevating overall customer-based brand equity.

A comparative analysis of bank-customer communications across various Islamic countries, with a particular focus on the content of face-to-face and online reciprocal interactions, may reveal noteworthy distinctions across diverse societies and similar cultures. Furthermore, in Iran, higher interest rates typically serve as the primary basis for competition among financial institutions seeking to attract customers. Consequently, this dynamic has likely engendered a conflict in customers’ perceptions regarding banks and the quality of services rendered; from the customers’ viewpoint, the services provided may not generate substantial value when weighed against the prevailing bank interest rates and the financial returns offered, especially in a country where rates are the same for all banks.

Limitations

This research was conducted among the customers of Bank Saderat Iran. Bank Saderat is a state-owned bank that operates under the supervision of the Central Bank of Iran and provides services within the framework of Islamic banking regulations. Due to its state-owned nature, there is no significant differentiation between the services offered by this bank, such as interest rates, banking profit margins, and operating hours, and those of other banks in Iran. However, it should be noted that numerous financial institutions operate alongside traditional banks in Iran, which influences individuals’ perceptions when comparing financial services and rates. Consequently, one limitation of the present study is respondents’ lack of experiential knowledge of international banks and their services.

Furthermore, regarding the measurement items for trust in the bank, customers formulate their responses based on past service experiences and the history of bankruptcies and liquidations among financial institutions. Therefore, the dimension of customer trust in Iranian banks may be tied to the inherent stability of the banks, the absence of bankruptcy risk, and the fear of losing deposited capital. In fact, customers believe that, because Bank Saderat is a state-owned entity, the possibility of losing their capital is non-existent compared to that of other financial institutions. Thus, when responding to the survey, customers may base their trust in Bank Saderat on its government backing, emphasizing service continuity and protection against dissolution. Alternatively, in line with contexts relevant to Islamic countries, the religious orientation of these banks and financial institutions may be of substantial importance to customers.

From a managerial perspective, this research highlights that in competitive environments characterized by homogeneous competitor activities, creative strategies must be utilized to establish differentiation among customers. Creating differentiation that is clearly perceived by customers as a positive distinction from competitors can have a substantial impact on marketing effectiveness. Additionally, managers must diligently strive to create and sustain shared values. Routine operations and promotional campaigns do not necessarily translate into a uniform perception of these values; therefore, the creation of shared value must be prioritized in all customer interactions.

References

Ahmad, R., Nawaz, M. R., Ishaq, M. I., Khan, M. M., & Ashraf, H. A. (2023). Social exchange theory: Systematic review and future directions. Frontiers in Psychology, 13, 1015921. https://doi.org/10.3389/fpsyg.2022.1015921

Alrubaiee, L., & Al-Nazer, N. (2010). Investigate the Impact of relationship Marketing Orientation on Customer Loyalty: The Customer’s Perspective. International Journal of Marketing Studies, II, 155–174. https://doi.org/10.5539/ijms.v2n1p155

Berry, L. L. (1983). Relationship marketing. In L. L. Berry, G. L. Shostack, & G. Upah. (Eds.), Emerging perspectives on services marketing (pp. 25–28). Chicago, IL: American Marketing Association.

Biedenbach, G., Bengtsson, M., & Wincent, J. (2011). Brand equity in the business-to- business context: Examining the role of core value. Industrial Marketing Management, 40(3), 446–454. https://doi.org/10.1016/j.indmarman.2010.06.002

Chen, C. F., & Myagmarsuren, O. (2011). Brand equity, relationship quality, relationship value, and customer loyalty: Evidence from the telecommunications services. Total Quality Management & Business Excellence, 22(9), 957–974. https://doi.org/10.1080/14783363.2011.593872

Colgate, M. R., & Danaher, P. J. (2000). Implementing a customer relationship strategy: The asymmetric impact of poor versus excellent execution. Journal of the Academy of Marketing Science, 28(3), 375–387. https://doi.org/10.1177/0092070300283006

Djajanto, L., Afiatin, Y., & Haris, Z. A. (2019). The impact of relationship marketing on customer value, satisfaction and loyalty: evidence from banking sector in Indonesia. International Journal of Economic Policy in Emerging Economies, Inderscience Enterprises Ltd, 12(2), 207–214. http://dx.doi.org/10.1504/IJEPEE.2019.099695

Eskandari, H., Aali, S., & Heris, A. B. (2017). The impact of relationship marketing tactics and dimensions of the relationship quality on customer loyalty. Management and Business Research Quarterly, 1, 1–13. https://doi.org/10.32038/mbrq.2017.01.01

Fatema, M., Azad, I., & Masum, A. K. M. (2013). Impact of brand image and brand loyalty in measuring brand equity of Islami Bank Bangladesh Ltd. Asian Business Review, 2(1), 42–46. https://ideas.repec.org/a/ris/asbure/0141.html

Ferrell, O. C., Gonzalez-Padron, T. L., Hult, G. T. M., & Maignan, I. (2010). From market orientation to stakeholder orientation. Journal of Public Policy & Marketing, 29(1), 93–96. https://doi.org/10.1509/jppm.29.1.93

Hau, L. N., & Ngo, L. V. (2012). Relationship marketing in Vietnam: An empirical study. Asia Pacific Journal of Marketing and Logistics, 24(2), 222–235. https://doi.org/10.1108/13555851211218039

Jang, M., Jung, Y., Kim, S. (2021). Investigating managers’ understanding of chatbots in the Korean financial industry. Computers in Human Behavior, 120, 106747. https://doi.org/10.1016/j.chb.2021.106747.

Kim, H., Kim, W. G., & An, J. A. (2005). The effect of consumer –based brand equity on firm financial performance. Journal of Consumer Marketing, 20(4), 335–351. https://doi.org/10.1108/07363760310483694

Kumar, V., Bohling, T. R., & Ladda, R. N. (2003). Antecedents and consequences of relationship intention: Implications for transaction and relationship marketing. Industrial Marketing Management, 32(8), 667–676. https://doi.org/10.1016/j.indmarman.2003.06.007

Loureiro, S. M. C., & Sarmento, E. M. (2018). Enhancing brand equity through emotions and experience: the banking sector. International Journal of Bank Marketing, 36(5), 868–883. https://doi.org/10.1108/IJBM-03-2017-0061

Mohammadian, M., & Aslani Afrashteh, A. (2022). Dimensions of relationship marketing and its impact on brand equity in banking industry (Case of Hekmat Iranian Bank). Journal of Engineering Management and Soft Computing, 7(2), 199–220. https://10.22091/jemsc.2018.2008.1052

Mathur, M. (2024). Social-relational capabilities: strategic transformation of brand resources to increase brand equity. The International Review of Retail, Distribution and Consumer Research, 34(1), 73–103. https://doi.org/10.1080/09593969.2023.2207033

Monfort, A., López-Vázquez, B., & Sebastián-Morillas, A. (2025). Building trust in sustainable brands: Revisiting perceived value, satisfaction, customer service, and brand image. Sustainable Technology and Entrepreneurship, 4(3), 100105. https://doi.org/10.1016/j.stae.2025.100105

Morgan, R. M., & Hunt, S. D. (1994). The commitment-trust theory of relationship marketing. Journal of Marketing, 58(3), 20–38. https://doi.org/10.1177/002224299405800302

Mukerjee, K. (2018). The impact of brand experience, service quality and perceived value on word of mouth of retail bank customers: Investigating the mediating effect of loyalty. Journal of Financial Services Marketing, 23(1), 12–24. https://doi.org/10.1057/s41264-018-0039-8

Ogbechi, A. D., Okafor, L. I., & Orukotan, C. I. (2018). Effect of relationship marketing on customer retention and loyalty in the money deposit bank industry. African Research Review, 12(2), 23–34. http://dx.doi.org/10.4314/afrrev.v12i2.3

Oyenuga, M. O., & Vu, C. N. (2024). Brand equity and customer life cycle in start-ups. Marketing and Branding Research, 11(1), 51–78. https://doi.org/10.32038/mbr.2024.11.01.05

Ranjbarian, B., Sanayei, A., Kaboli, M. R., & Hadadian, A. (2012). An analysis of brand image, perceived quality, customer satisfaction and brand loyalty in Iranian banks. International Journal of Business and Management, 7(6), 53–61. https://doi.org/10.5539/ijbm.v7n6p53

Rather, R. A., Tehseen, S., & Parrey, S. H. (2018). Promoting customer brand engagement and brand loyalty through customer brand identification and value congruity. Spanish Journal of Marketing-ESIC, 22(3), 319–337. https://doi.org/10.1108/SJME-06-2018-0030

Razavi, S. M. J., Tolabi-Mazraeno, A., & Kotobi, F. (2025). The role of relationship marketing on brand equity: The mediating role of brand identification and brand experience (A Case Study of Isfahan Sport Clubs). Journal of Sport Marketing Studies, 6(2), 1–14. https://doi.org/10.22034/sms.2025.142399.1419

Rosário, A. & Casaca. J. A. (2023). Relational marketing and customer satisfaction: A systematic literature review. Estudios Gerenciales, 39(169), 516–532. https://doi.org/10.18046/j.estger.2023.169.6218

Santos, Z. R., Coelho, P. S., & Rita, P. (2022). Fostering Consumer–Brand Relationships through social media brand communities. Journal of Marketing Communications, 28(7), 768–798. https://doi.org/10.1080/13527266.2021.1950199

Sayil, E. M., Akyol, A., & Golbasi Simsek, G. (2019). An integrative approach to relationship marketing, customer value, and customer outcomes in the retail banking industry: a customer-based perspective from Turkey. The Service Industries Journal, 39(5–6), 420–461. https://doi.org/10.1080/02642069.2018.1516755

Sin, L. Y., Tse, A. C., Yau, O. H., Chow, R. P., Lee, J. S., & Lau, L. B. (2005). Relationship marketing orientation: Scale development and cross-cultural validation. Journal of Business Research, 58(2), 185–194. https://doi.org/10.1016/S0148-2963(02)00493-9

So, S. L. M., Speece, M. W. (2000). Perceptions of relationship marketing among account managers of commercial banks in a Chinese environment. International Journal of Bank Marketing, 18(7), 27–315. https://doi.org/10.1108/02652320010359534

Teichmann, K. (2021). Loyal customers’ tipping points of spending for services: a reciprocity perspective". European Journal of Marketing, 55(13), 202–229. https://doi.org/10.1108/EJM-10-2019-0781

Tran, K. T., Truong, A. T. T., Truong, V. A. T., & Luu, T. T. (2024). Leveraging brand coolness for building strong consumer-brand relationships: different implications for products and services. Journal of Product & Brand Management, 33(2), 258–272. https://doi.org/10.1108/JPBM-05-2023-4476

Turk, B. (2021). Brand's Image, Love, and Loyalty: Is it Enough for Word of Mouth Marketing? Management and Business Research Quarterly, 18, 16-27. https://doi.org/10.32038/mbrq.2021.18.02

van Esterik-Plasmeijer, P. W., & Van Raaij, W. F. (2017). Banking system trust, bank trust, and bank loyalty. International Journal of Bank Marketing, 35(1), 97–111. https://doi.org/10.1108/IJBM-12-2015-0195

Veloutsou, C. (2015). Brand evaluation, satisfaction and trust as predictors of brand loyalty: The mediator-moderator effect of brand relationships. Journal of Consumer Marketing, 32(6), 405–421. https://doi.org/10.1108/JCM-02-2014-0878

Wahyoedi, S., Sudiro, A., Sunaryo, S., & Sudjatno, S. (2021). The effect of religiosity and service quality on customer loyalty of Islamic banks mediated by customer trust and satisfaction. Management Science Letters, 11, 187–194. http://growingscience.com/beta/msl/4186-the-effect-of-religiosity-and-service-quality-on-customer-loyalty-of-islamic-banks-mediated-by-customer-trust-and-satisfaction.html

Wongsansukcharoen, J. (2022). Effect of community relationship management, relationship marketing orientation, customer engagement, and brand trust on brand loyalty: The case of a commercial bank in Thailand. Journal of Retailing and Consumer Services, 64. 102826. https://doi.org/10.1016/j.jretconser.2021.102826

Yau, O. H., McFetridge, P. R., Chow, R. P., Lee, J. S., Sin, L. Y., & Tse, A. C. (2000). Is relationship marketing for everyone? European Journal of Marketing, 34(9/10), 1111–1127. https://doi.org/10.1108/03090560010342561

Yoganathan, D., Jebarajakirthy, C., & Thaichon, P. (2015). The influence of relationship marketing orientation on brand equity in banks. Journal of Retailing and Consumer Services. 26, 14–22. https://doi.org/10.1016/j.jretconser.2015.05.006

Page 1 of

Download Count : -

Visit Count : 71

Keywords

Relationship Marketing Orientation; Brand Equity; Saderat Bank; Perceived Quality

Author(s) Information

How to cite this paper

Ardabili, F. S., Vratar, L. & Cajnko, P. (2025). The impact of relationship marketing on brand equity in the Banking sector in Iran. Marketing and Branding Research, 12(1), 90-103. https://doi.org/10.32038/mbr.2025.12.01.05

Author Contributions

Farzad S. Ardabili: Writing – review & editing, Writing – original draft, Validation, Methodology, Formal analysis, Data collection and Data curation, Conceptualization.

Petra Cajnko: Formal analysis, Data curation, Review & editing, Conceptualization.

Leon Vratar: Review & editing, Investigation, Formal analysis, Data curation, Conceptualization.

Acknowledgements

The author(s) thank the editor and anonymous reviewers for their constructive feedback, which substantially improved the clarity and quality of this manuscript.

Disclosure Statement

No potential conflict of interest was reported by the authors.

Funding Acknowledgements

Not applicable.

Ethics Approval

Not applicable.

Data Availability

The datasets and code used and/or analyzed during the current study are available in Mendely at doi:10.17632/4brf84t9xs.1

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/