Original Research

Board Gender Diversity, Audit Effort, and Financial Reporting Quality

- Abstract

- Full text

- Metrics

This study aims to examine the role of board and audit committee gender diversity in audit effort and financial reporting quality. The research follows a quasi-experimental, ex-post-facto design. To test the research hypotheses, financial data from 163 companies listed on the Tehran Stock Exchange between 2012 and 2022 are analyzed using multivariate regression and panel data techniques. The findings reject all four hypotheses. Specifically, the results of the first hypothesis test indicate that the gender composition of the audit committee has a significant negative impact on audit effort, meaning that the presence of women on the audit committee leads to a reduction in auditors' efforts and, consequently, lower audit fees. Testing the second hypothesis test shows that the presence of women in the audit committee reduces the likelihood of selecting larger, higher-quality audit firms for auditing financial reports. This suggests a lack of female participation in auditor selection and negotiation processes. As for the third hypothesis, the findings reveal no significant impact of board gender on obtaining an unqualified audit opinion, as the presence of women on the audit committee does not reduce the likelihood of the company receiving such opinions from auditors. Finally, the results of the fourth hypothesis test show that female members on the audit committee and board of directors have no significant impact on the quality of financial reporting in Iranian companies.

Board Gender Diversity, Audit Effort, and Financial Reporting Quality

Saeed Alipour*, Davood Mostafazadeh

Department of Accounting, Ardabil Branch, Islamic Azad University, Ardabil, Iran

Department of Financial Management, Central Tehran Branch, Islamic Azad University, Tehran, Iran

ABSTRACT

This study aims to examine the role of board and audit committee gender diversity in audit effort and financial reporting quality. The research follows a quasi-experimental, ex-post-facto design. To test the research hypotheses, financial data from 163 companies listed on the Tehran Stock Exchange between 2012 and 2022 are analyzed using multivariate regression and panel data techniques. The findings reject all four hypotheses. Specifically, the results of the first hypothesis test indicate that the gender composition of the audit committee has a significant negative impact on audit effort, meaning that the presence of women on the audit committee leads to a reduction in auditors' efforts and, consequently, lower audit fees. Testing the second hypothesis test shows that the presence of women in the audit committee reduces the likelihood of selecting larger, higher-quality audit firms for auditing financial reports. This suggests a lack of female participation in auditor selection and negotiation processes. As for the third hypothesis, the findings reveal no significant impact of board gender on obtaining an unqualified audit opinion, as the presence of women on the audit committee does not reduce the likelihood of the company receiving such opinions from auditors. Finally, the results of the fourth hypothesis test show that female members on the audit committee and board of directors have no significant impact on the quality of financial reporting in Iranian companies.

Keywords: Auditor Size, Audit Committee Gender Diversity, Board Gender Diversity, Audit Fees, Financial Reporting Quality

JEL Classification: G34, M42, J16

Gender diversity among corporate directors is a widely debated topic in both academia and practice. This study is motivated by the need to explore one of the potential outcomes of female board membership: its effect on the financial reporting environment and mechanisms to enhance reporting quality. Iran's economic environment differs significantly from other regions, given its unique legal framework concerning women's participation in economic activities.

Nevertheless, evidence indicates a rising trend of women joining the boards of companies listed on the Tehran Stock Exchange. This trend and its future trajectory, along with the analysis of its potential consequences, highlight the relevance of research in this area. There is evidence suggesting that board gender diversity influences the quality of corporate governance (e.g., Adams & Ferreira, 2009; Nielsen & Huse, 2010).

Discussions around economic and social equity have fueled debates on the need to address the underrepresentation of women on corporate boards. A distinct body of literature examines the impact of female directors on internal corporate governance rather than focusing on the causal relationship between board gender diversity and corporate performance or risk. Adams and Ferreira (2009) found that female directors enhance board meeting attendance and that CEO turnover sensitivity to stock performance is greater in firms with more gender-diverse boards, indicating a positive impact of women on board oversight (Post & Byron, 2015).

Literature Review

Female workforce participation is a growing phenomenon across most global economies, and Iran is not an exception. Despite ongoing improvements, the underrepresentation of women in senior corporate roles remains a persistent issue worldwide. The historical dominance of men in senior corporate positions has perpetuated gender inequalities in access to executive and board roles, resulting in two major negative outcomes. First, excluding a significant portion of the workforce from top corporate positions conflicts with the principle of social justice, which advocates for equal representation of all demographic groups (Dahlerup et al., 2002). Second, from an economic standpoint, disregarding a substantial portion of the talent pool appears inefficient.

Some countries have implemented legislation to promote female representation on corporate boards, while others have opted for softer approaches, such as board diversity recommendations. Mandating boardroom gender quotas has sparked controversy, as it is seen as undermining the meritocratic principles of board nominations. Critics argue that such interventions may lead to the appointment of less competent individuals, and various studies have highlighted this concern (e.g., Choudhury, 2015; Gopalan & Watson, 2015; Szydło, 2015).

In Iran's economic environment, there is no mandatory requirement for female representation on corporate boards. Evidence suggests that approximately 19% of board members in Iranian publicly traded companies are women (Kazemi Oloum et al., 2019). Similarly, research by Mam Salehi and Eskandarli (2019) points to an average female board participation rate of 18%.

Although there is a general trend toward narrowing the gender gap on corporate boards, empirical evidence on the impact of board gender diversity on firm performance and risk remains inconclusive. However, studies suggest that women are less likely than men to engage in unethical workplace behaviors for financial gain (Heminway, 2007; Kaplan et al., 2009; Khazanchi, 1995). Moreover, female executives tend to be more risk-averse than their male counterparts, leading to lower involvement in earnings management practices (Krishnan & Parsons, 2008).

Analyzing the impact of gender diversity on boards of directors and audit committees offers an opportunity to examine the potential benefits for companies that voluntarily adopt gender diversity in board composition. Previous studies have linked female board representation to increased audit efforts, often reflected in higher audit fees (Aldamen et al., 2018; Miglani & Ahmed, 2019; Sellami & Cherif, 2020) or in contracting with Big Four audit firms (Kibiya et al., 2016).

Earlier findings by Post and Byron (2015) and Konrad et al. (2008) support Kanter's (1977) critical mass theory, showing that having at least three female directors allows women to meaningfully influence boardroom decisions. However, in Iran's public company environment, where female underrepresentation is a social norm, conducting such research is both innovative and significant.

Fernández-Méndez and Pathan (2022) explored female directors, audit effort, and financial reporting quality. Their findings suggest that board gender diversity and audit committees positively influence audit demand and audit outcomes, particularly when women serve as non-executive directors. Experienced and highly involved female directors, especially those chairing the board or audit committee, play a critical role in enhancing audit efforts and outcomes. Importantly, these positive effects were observed even without reaching a specific critical mass of women. Furthermore, gender diversity was found to improve auditor independence despite lower non-audit fees.

Oradi and Izadi (2020) examined the relationship between audit committee gender diversity and financial reporting. Their findings revealed that, after controlling for other factors, the presence of at least one female member on the audit committee reduces the likelihood of financial restatements, a conclusion supported by robustness tests. Additionally, female independent directors and financial experts on audit committees were strongly associated with fewer financial restatements. Their study also found that gender-diverse audit committees are more likely to employ higher-quality auditors. Overall, these findings align with literature suggesting that women excel in oversight roles, adopt more conservative decision-making approaches, and make more ethical choices.

Mohammadi and Yousefvand (2022) studied the impact of board and audit committee gender diversity on managerial capability and transparency in companies listed on the Tehran Stock Exchange. Their results showed that the presence of women on audit committees has a significant effect on managerial capability. Moreover, board gender diversity was found to have a significant impact on both managerial capability and transparency.

Abdi et al. (2020) investigated the relationship between gender diversity and the likelihood of financial restatements, testing group dynamics theory. Their findings suggested that having at least one female member on the audit committee reduces the likelihood of financial restatements. However, no significant effect was observed for female board membership on restatement reduction. Nonetheless, the presence of women in governance structures, particularly on audit committees, was associated with improved financial reporting quality.

Given the discussions above, this study aims to examine the role of board gender diversity in the financial reporting environment of publicly traded companies in Iran. To achieve this objective, the following hypotheses are proposed:

H1: Board and audit committee gender diversity is positively associated with audit fees.

H2: Board and audit committee gender diversity is positively associated with the likelihood of being audited by large audit firms.

H3: Board and audit committee gender diversity is positively associated with the likelihood of receiving an unqualified audit opinion.

H4: Board and audit committee gender diversity is negatively associated with earnings management.

Method

The present research employs a quasi-experimental and ex-post facto design. The data are collected from various sources, including the Tehran Stock Exchange database, Rahavard Novin software, and other information sources. Data analysis is conducted using panel data analysis (year-by-year review) and multiple linear regression.

Data Analysis

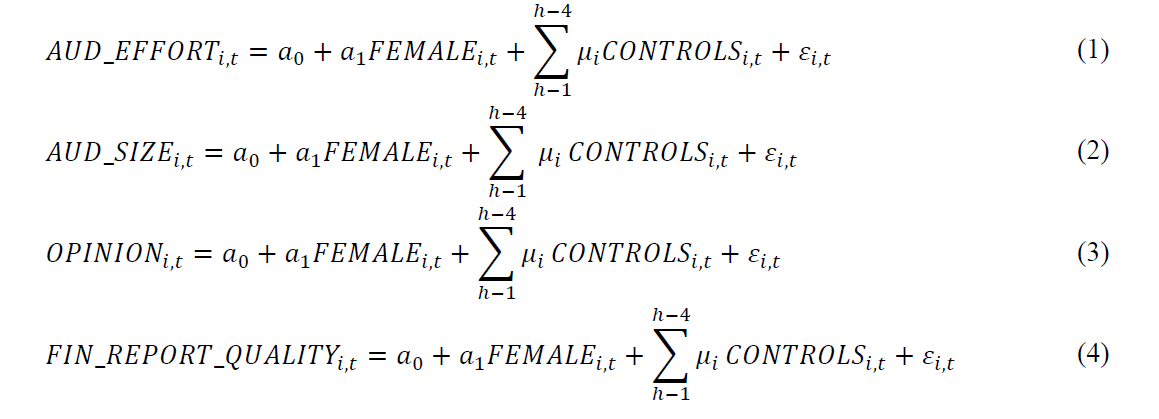

Following Fernández-Méndez and Pathan (2022), models 1, 2, 3, and 4 will be used to test the first, second, third, and fourth research hypotheses, respectively.

The variables used in these models are as follows:

Dependent Variables:

o (Audit Effort): Natural logarithm of audit fees.

o (Audit Firm Size): Coded as 1 if the company's financial statements are audited by either Iran Audit Organization or Mofid Rahbar Audit Firm, and 0 otherwise.

o (Audit Opinion): Coded as 1 for unqualified audit opinions, and 0 otherwise.

o (Financial Reporting Quality): Measured by accrual-based earnings management using the Modified Jones Model (Dechow et al., 1995).

Independent Variable:

o (Board/Audit Committee Gender Diversity): Number of female members on the board of directors ( )/the audit committee ( ).

Control Variables:

o (Firm Size): Natural logarithm of total assets.

o (Financial Leverage): Ratio of total liabilities to total assets.

o (Sales Growth): Current year's sales growth compared to the previous year.

o (Profitability): Return on assets (ROA), calculated as earnings before interest and taxes divided by total assets.

Findings

Descriptive Statistics

The descriptive statistics for the variables are presented in Table 1. The average audit effort, measured by the natural logarithm of audit fees, is 4.67. The average financial reporting quality is .14. The findings reveal that only 7% of board members and 9% of audit committee members are female. The average financial leverage is .54, indicating that liabilities exceed equity. The average sales growth rate is 32%, and the average profitability is .161. Additionally, 57% of the sampled companies were audited by large audit firms, and 25% of auditor reports were unqualified.

Descriptive Statistics of the Variables

|

Variable |

M |

Mdn |

Max |

Min |

SD |

Observations |

|

AUD_EFFORT |

4.67 |

6.32 |

13.47 |

0.00 |

3.53 |

1793 |

|

FIN_REPORT_QUALITY |

0.14 |

0.09 |

2.86 |

0.00 |

0.17 |

1793 |

|

FEMALE1 |

0.06 |

0.00 |

1.00 |

0.00 |

0.25 |

1793 |

|

FEMALE2 |

0.09 |

0.00 |

1.00 |

0.00 |

0.29 |

1793 |

|

SIZE |

14.60 |

14.38 |

21.32 |

10.16 |

1.71 |

1793 |

|

LEV |

0.54 |

0.55 |

2.07 |

0.01 |

0.22 |

1793 |

|

GROWTH |

0.32 |

0.26 |

1.20 |

-0.27 |

0.39 |

1793 |

|

PROFIT |

0.16 |

0.13 |

0.84 |

-0.58 |

0.17 |

1793 |

|

AUD_SIZE |

Percentage of large audit firms: 57% |

|||||

|

OPINION |

Percentage of unqualified opinions: 25% |

|||||

Correlation Analysis

Table 2 presents the correlation coefficients among the research variables, indicating that no variables are perfectly correlated. In other words, each variable remains independent from the others.

Correlations Among the Variables

|

Variable |

AUD_ EFFORT |

FIN_REPORT _QUALITY |

FEMALE1 |

FEMALE2 |

SIZE |

LEV |

GROWTH |

PROFIT |

|

AUD_ EFFORT |

1 |

|||||||

|

FIN_REPORT _QUALITY |

-.00 |

1 |

||||||

|

FEMALE1 |

.02 |

-.00 |

1 |

|||||

|

FEMALE2 |

-.02 |

.04 |

.08 |

1 |

||||

|

SIZE |

-.16 |

.01 |

-.07 |

-.10 |

1 |

|||

|

LEV |

-.01 |

-.11 |

-.07 |

-.00 |

-.07 |

1 |

||

|

GROWTH |

-.02 |

.16 |

.02 |

.01 |

.21 |

-.17 |

1 |

|

|

PROFIT |

.00 |

.17 |

.08 |

-.07 |

.20 |

-.59 |

.35 |

1 |

Stationarity Test

The Levin–Lin–Chu test is used to assess the stationarity of the variables. Table 3 presents the test results. The significance level for all the variables is less than .05, indicating stationarity and ensuring that no spurious regression occurs when using these variables.

Levin–Lin–Chu Test Results

|

Variable |

Statistic |

p |

Result |

|

AUD_EFFORT |

-11.72 |

.000 |

Stationary |

|

FIN_REPORT_QUALITY |

-27.02 |

.000 |

Stationary |

|

FEMALE1 |

-2.01 |

.021 |

Stationary |

|

FEMALE2 |

-10.64 |

.000 |

Stationary |

|

SIZE |

-10.30 |

.000 |

Stationary |

|

LEV |

-15.69 |

.000 |

Stationary |

|

GROWTH |

-17.14 |

.000 |

Stationary |

|

PROFIT |

-12.57 |

.000 |

Stationary |

Testing Hypothesis 1

The first hypothesis states: “Board and audit committee gender diversity are positively associated with audit fees.” Table 4 presents the results of testing this hypothesis.

Results of Testing H1

|

Variable |

Coefficient |

Standard Error |

Statistic |

Sig. |

VIF |

|

FEMALE1 |

.00 |

.00 |

1.68 |

.090 |

1.02 |

|

FEMALE2 |

-.30 |

.08 |

-3.77 |

.000 |

1.02 |

|

SIZE |

.01 |

.00 |

4.64 |

.000 |

1.08 |

|

LEV |

-.01 |

.02 |

-0.83 |

.402 |

1.56 |

|

GROWTH |

-.00 |

.00 |

-0.21 |

.833 |

1.18 |

|

PROFIT |

-.02 |

.01 |

-1.56 |

.118 |

1.78 |

|

R2 |

0.99 |

||||

|

Adjusted R2 |

0.99 |

||||

|

F-statistic |

1501.51 (p = .000) |

||||

|

Durbin-Watson Statistic |

1.94 |

||||

|

Lagrange Multiplier (LM) Test |

23.51 (p = .000) |

||||

|

Hausman Test Statistic |

41.36 (p = .000) |

||||

|

White Test (Homoscedasticity) |

12.88 (p = .000) |

||||

Given that the significance level of the F-statistic in the tested model is less than .05, it can be concluded that the overall model is significant. Additionally, the Durbin-Watson statistic falls between 1.5 and 2.5, indicating that there is no autocorrelation in the residuals.

In the first model, the significance level of the LM test statistic is .000, which supports the null hypothesis and suggests that panel data methods should be used for estimation. Since the model is panel-based, the Hausman test is employed to determine the appropriate panel data method (fixed or random effects). The significance level of the Hausman test in the first research model is less than .05, indicating that the fixed effects method is preferred over the random effects method.

According to the results, the variance inflation factor (VIF) for all the variables used in testing H1 is less than 10, indicating that there is no significant multicollinearity among the explanatory variables in this model. The results of the White test indicate the presence of heteroscedasticity in the residuals of the first research model. Consequently, the White correction and the Generalized Least Squares (GLS) method are applied to address this issue.

The adjusted R-squared value for the tested model is .99, suggesting that approximately 99% of the variations in the dependent variable are explained by the explanatory variables. The findings indicate that the gender composition of the board of directors is positively associated with auditor effort at the 9% significance level. However, the gender composition of the audit committee is negatively associated with audit effort at the 1% significance level.

The findings suggest that the presence of women on the board of directors leads to an increase in audit fees, reflecting greater audit effort. In contrast, the presence of female members on the audit committee reduces audit effort. Based on these results, the first hypothesis regarding the gender composition of the board of directors is not supported.

Testing Hypothesis 2

The results of testing H2, which states "board and audit committee gender diversity are positively associated with the likelihood of being audited by large audit firms," are shown in Table 5.

Results of Testing H2

|

Variable |

Coefficient |

Standard Error |

Statistic |

Sig. |

VIF |

|

FEMALE1 |

0.04 |

.24 |

0.19 |

.845 |

1.02 |

|

FEMALE2 |

-1.83 |

.35 |

-5.11 |

.000 |

1.02 |

|

SIZE |

0.34 |

.03 |

9.65 |

.000 |

1.08 |

|

LEV |

3.03 |

.36 |

8.29 |

.000 |

1.56 |

|

GROWTH |

-0.46 |

.17 |

-2.71 |

.006 |

1.18 |

|

PROFIT |

2.23 |

.50 |

4.46 |

.000 |

1.78 |

|

McFadden's R2 |

0.11 |

||||

|

LR Statistic |

227.93 (p = .000) |

||||

Since the dependent variable in the tested model is binary (1 or 0), logistic regression is used to test the hypothesis. Given the significance level of the LR statistic in the tested model, which is less than .05, it can be concluded that the overall model is significant. McFadden's R2 for the tested model is .11, indicating that approximately 11% of the variation in the dependent variable is explained by the explanatory variables, which is appropriate for logistic regressions.

The findings indicate that board gender diversity does not have a significant impact on selecting large, high-quality auditors. However, they also show that the presence of women in the audit committee leads to fewer selections of large, high-quality audit firms. Based on these findings, the second hypothesis is not supported.

Testing Hypothesis 3

The results of testing H3, which states “board and audit committee gender diversity are positively associated with the likelihood of receiving an unqualified audit opinion,” are shown in Table 6.

Results of Testing H3

|

Variable |

Coefficient |

Standard Error |

Statistic |

Sig. |

VIF |

|

FEMALE1 |

0.00 |

0.20 |

0.04 |

.961 |

1.02 |

|

FEMALE2 |

-0.84 |

0.17 |

-4.90 |

.000 |

1.02 |

|

SIZE |

-0.14 |

0.03 |

-4.64 |

.000 |

1.08 |

|

LEV |

0.06 |

0.27 |

0.23 |

.812 |

1.56 |

|

GROWTH |

0.28 |

0.13 |

2.08 |

.037 |

1.18 |

|

PROFIT |

2.58 |

0.40 |

6.37 |

.000 |

1.78 |

|

McFadden's R2 |

0.04 |

||||

|

LR Statistic |

117.18 (p = .000) |

||||

Again, the dependent variable in the tested model is binary (1 or 0), and thus, logistic regression is used to test the hypothesis. Given the significance level of the LR statistic in the tested model, which is less than .05, it can be concluded that the overall model is significant. McFadden's R2 for the tested model is .04, indicating that approximately 5% of the variation in the dependent variable is explained by the explanatory variables, which is appropriate for logistic regressions.

The findings show that board gender diversity is not significantly associated with receiving an unqualified audit opinion, while the presence of women in the audit committee leads to a lower likelihood of companies receiving unqualified opinions from auditors. Based on these findings, the third hypothesis is not supported.

Testing Hypothesis 4

The results of testing H4, which posits “board and audit committee gender diversity are negatively associated with earnings management,” are presented in Table 7.

Results of Testing H4

|

Variable |

Coefficient |

Standard Error |

Statistic |

Sig. |

VIF |

|

FEMALE1 |

.00 |

.00 |

0.73 |

.460 |

1.02 |

|

FEMALE2 |

-.00 |

.01 |

-0.26 |

.788 |

1.02 |

|

SIZE |

.01 |

.00 |

6.20 |

.000 |

1.08 |

|

LEV |

.07 |

.02 |

3.44 |

.000 |

1.56 |

|

GROWTH |

.01 |

.00 |

2.54 |

.011 |

1.18 |

|

PROFIT |

.12 |

.02 |

4.35 |

.000 |

1.78 |

|

R2 |

0.31 |

||||

|

Adjusted R2 |

0.24 |

||||

|

F-statistic |

4.42 (p = .000) |

||||

|

Durbin-Watson Statistic |

2.09 |

||||

|

Lagrange Multiplier (LM) Test |

4.69 (p = .000) |

||||

|

Hausman Test Statistic |

69.86 (p = .000) |

||||

|

White Test (Heteroskedasticity) |

8.51 (p = .000) |

||||

Given that the F-statistic significance is below .05, the overall model is significant. The Durbin-Watson statistic falls between 1.5 and 2.5, indicating no autocorrelation in the residuals. Since the significance level of the Limer Test is .000, panel data estimation should be used. The Hausman Test significance is below 5%, indicating that the fixed-effects method is preferred over the random-effects method.

The VIF values for all explanatory variables are below 10, suggesting that there is no significant multicollinearity. The White Test indicates heteroskedasticity in the model, which is addressed using the White correction and GLS method. The adjusted R2 of .24 indicates that about 24.3% of the variance in the dependent variable is explained by the explanatory variables.

The results show no significant effect of female representation in the board of directors or audit committee on earnings management. Therefore, the fourth hypothesis is not supported.

Conclusion

The findings indicate an inverse relationship between board/audit committee gender diversity and auditor effort (measured by audit fees). Due to the low number of women in these positions, however, their impact may not align with prior research, as evidenced in the Iranian economic environment. Moreover, female representation in the board had no significant effect on financial reporting quality, possibly due to their low numbers and limited influence.

This study also revealed that female audit committee members reduce the likelihood of receiving unqualified opinions, indicating lower financial reporting quality. This may stem from a lack of expertise and limited female representation in high-ranking roles in Iranian companies. Additionally, some appointments may have been based on relationships rather than qualifications.

Our findings contradict those of Fernández-Méndez and Pathan (2022), who observed that gender diversity positively affected audit efforts and outcomes, with experienced female managers improving audit processes and outcomes while enhancing auditor independence.

Based on the present findings, it is recommended that more women be included in the board and audit committee structures. Women should be more involved in corporate decision-making, and their appointments should be based on qualifications and experience. Future studies are encouraged to examine the role of female board and audit committee members in different industries to account for potential industry-specific effects.

References

Abdi, M., Kazemi Olum, M., Rezaeian, H., & Neiri, H. (2020). Gender diversity and the likelihood of financial restatement: testing group dynamics theory. Financial Accounting Knowledge, 7(3), 145–166. [In Persian] https://doi.org/10.30479/jfak.2020.12241.2602

Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309. https://doi.org/10.1016/j.jfineco.2008.10.007

Aldamen, H., Hollindale, J., & Ziegelmayer, J. (2018). Female audit committee members and their influence on audit fees. Accounting and Finance, 58(1), 57–89. https://doi.org/10.1111/acfi.12248

Choudhury, B. (2015). Gender diversity on boards: Beyond quotas. European Business Law Review, 26(1). https://doi.org/10.54648/eulr2015012

Dahlerup, D., Griffin, G., & Braidotti, R. (2002). Three waves of feminism in Denmark. Thinking Differently, 341–350. https://B2n.ir/d67413

Dechow, P., Sloan, R. & Sweeney, A. (1995). Detecting earnings management. Accounting Review, 70(2): 193–225. https://www.jstor.org/stable/248303

Fernández-Méndez, C., & Pathan, S. T. (2022). Female directors, audit effort and financial reporting quality. Spanish Journal of Finance and Accounting/Revista Española de Financiación y Contabilidad, 1–42. https://doi.org/10.1080/02102412.2021.2009298

Gopalan, S., & Watson, K. (2015). An agency theoretical approach to corporate board diversity. San Diego Law Review, 52, 1. http://dx.doi.org/10.2139/ssrn.2479645

Heminway, J. M. (2007). Sex, trust, and corporate boards. Hastings Women’s LJ, 18, 173. https://repository.uclawsf.edu/hwlj/vol18/iss2/3

Kanter, R. (1977). Men and women of the corporation. Basic Books. https://B2n.ir/y68984

Kaplan, S., Pany, K., Samuels, J., & Zhang, J. (2009). An examination of the association between gender and reporting intentions for fraudulent financial reporting. Journal of Business Ethics, 87, 15–30. https://doi.org/10.1007/s10551-008-9866-1

Kazemi Oloum, M., Imani Barandagh, M., & Abdi, Mostafa. (2019). Examining the effect of gender diversity in the board of directors and audit committee on earnings quality. Accounting Knowledge Journal, 10(1), 137–168. [In Persian] https://doi.org/10.22103/jak.2019.11887.2655

Khazanchi, D. (1995). Unethical behavior in information systems: The gender factor. Journal of Business Ethics, 14, 741–749. https://doi.org/10.1007/BF00872327

Kibiya, M. U., Che-Ahmad, A., & Amran, N. A. (2016). Audit committee independence, financial expertise, share ownership and financial reporting quality: Further evidence from Nigeria. International Journal of Economics and Financial Issues, 6(7), 125–131. https://www.researchgate.net/publication/311038021_Audit_Committee_Independence_Financial_Expertise_Share_Ownership_and_Financial_Reporting_Quality_Further_Evidence_from_Nigeria

Konrad, A. M., Kramer, V., & Erkut, S. (2008). The impact of three or more women on corporate boards. Organizational Dynamics, 37(2), 145–164. https://doi.org/10.1016/j.orgdyn.2008.02.005

Krishnan, G. V., & Parsons, L. M. (2008). Getting to the bottom line: An exploration of gender and earnings quality. Journal of Business Ethics, 78, 65–76. http://dx.doi.org/10.1007/s10551-006-9314-z

Mam Salehi, P., & Eskandarli, T. (2019). Gender diversity in board members and the value relevance of corporate social responsibility reporting. Experimental Accounting Research, 9(2), 351–372. [In Persian] https://doi.org/10.22051/jera.2018.18419.1889

Miglani, S., & Ahmed, K. (2019). Gender diversity on audit committees and its impact on audit fees: evidence from India. Accounting Research Journal. https://doi.org/10.1108/ARJ-01-2018-0001

Mohammadi, M., & Yousefvand, D. (2022). Investigating the impact of board and audit committee gender diversity on managerial ability and transparency in companies listed on the Tehran Stock Exchange. New Research Approaches in Management and Accounting, 5(16), 114–137. [In Persian] https://majournal.ir/index.php/ma/article/view/660 https://majournal.ir/index.php/ma/article/view/660

Nielsen, S., & Huse, M. (2010). The contribution of women on boards of directors: Going beyond the surface. Corporate governance: An International Review, 18(2), 136–148. https://doi.org/10.1111/j.1467-8683.2010.00784.x

Oradi, J., & Izadi, J. (2020). Audit committee gender diversity and financial reporting: evidence from restatements. Managerial Auditing Journal, 35(1), 67–92. https://doi.org/10.1108/MAJ-10-2018-2048

Post, C., & Byron, K. (2015). Women on boards and firm financial performance: A meta-analysis. Academy of Management Journal, 58(5), 1546–1571. https://www.jstor.org/stable/24758233

Sellami, Y., & Cherif, I. (2020). Female audit committee directorship and audit fees. Managerial Auditing Journal, 35(3), 398–428. https://doi.org/10.1108/MAJ-12-2018-2121

Szydło, M. (2015). Gender equality on the boards of EU companies: between economic efficiency, fundamental rights and democratic legitimization of economic governance. European Law Journal, 21(1), 97–115. https://doi.org/10.1111/eulj.12074

Page 1 of

Download Count : 39

Visit Count : 154

Keywords

Audit Committee Gender Diversity; Auditor Size; Board Gender Diversity; Audit Fees; Financial Reporting Quality

Author(s) Information

How to cite this article:

Alipour, S., & Mostafazadeh, D. (2024). Board gender diversity, audit effort, and financial reporting quality. New Challenges in Accounting and Finance, 12, 30–41. https://doi.org/10.32038/NCAF.2024.12.03

Acknowledgments

Not applicable.

Funding

Not applicable.

Conflict of Interests

No, there are no conflicting interests.

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/