Review Article

Financial Analysts and ESG Factors in Listed Companies: A Critical Review and Future Directions

- Abstract

- Full text

- Metrics

This paper aims to provide a comprehensive and critical literature review of pivotal studies examining the interaction between analysts’ coverage and publicly traded companies' disclosure of ESG practices. It explores how analysts' coverage influences corporate sustainability and identifies gaps for future research. The review highlights that analysts catalyze corporate sustainability by driving ESG adoption, fostering transparency, and promoting responsible investment practices. This dynamic relationship benefits the companies and contributes to the broader goal of creating sustainable and resilient financial markets. However, results are more robust in developed markets, while evidence for emerging markets remains limited. This study offers a critical perspective on the relationship between analysts' coverage and ESG practices, addressing an area of growing interest in sustainable finance. By identifying gaps in the existing literature and proposing a research agenda, the paper contributes to understanding how analysts influence corporate sustainability and market practices.

Financial Analysts and ESG Factors in Listed Companies: A Critical Review and Future Directions

Fatima Berrada, Siham Meknassi

Department of Finance – ISCAE – Morocco

Abstract:

This paper aims to provide a comprehensive and critical literature review of pivotal studies examining the interaction between analysts’ coverage and publicly traded companies' disclosure of ESG practices. It explores how analysts' coverage influences corporate sustainability and identifies gaps for future research. The review highlights that analysts catalyze corporate sustainability by driving ESG adoption, fostering transparency, and promoting responsible investment practices. This dynamic relationship benefits the companies and contributes to the broader goal of creating sustainable and resilient financial markets. However, results are more robust in developed markets, while evidence for emerging markets remains limited. This study offers a critical perspective on the relationship between analysts' coverage and ESG practices, addressing an area of growing interest in sustainable finance. By identifying gaps in the existing literature and proposing a research agenda, the paper contributes to understanding how analysts influence corporate sustainability and market practices.

Keywords: Analyst Coverage, ESG Practices, Corporate Sustainability, Financial Markets, Sustainable Finance

Financial analysts, particularly sell-side analysts, play a pivotal role in financial markets as information intermediaries. Their recommendations, earnings forecasts, and price targets provide crucial insights to institutional and individual investors, significantly influencing investment decisions (Ramnath et al., 2008). Over the years, the informational value of financial analysts' publications has been extensively addressed in the literature and across different markets, including emerging markets. The results were almost unanimous, with authors finding that the market reacts to such publications (Altinkiliç & Hansen, 2009; Barber et al., 2001; Bellando et al., 2016; Moshirian et al., 2009; Womack, 1996). Financial analysts can provide helpful information for market participants' decision-making (Asquith et al., 2005; Beaver et al., 2008; Stickel, 1995; Womack, 1996).

In parallel, social and environmental pressures have increased over the past decade. Companies must reconsider organizational aspects such as corporate governance, social responsibility, and internal transparency to meet the needs of various stakeholders (Eccles et al., 2011, 2014). Concepts like Environmental, Social, and Governance (ESG) have emerged as key components of corporate sustainability, shifting the focus of investors and analysts toward non-financial performance metrics (Gillan et al., 2021). This shift in focus towards ESG is now a critical factor in shaping market perceptions and investment decisions.

This article is motivated by the profound transformation of the information environment in the financial market. The main objective is to critically examine how ESG disclosure impacts analysts’ coverage and companies’ visibility. We seek to answer the following questions:

1. How do financial analysts influence the adoption and promotion of ESG practices in listed companies?

2. To what extent does ESG disclosure improve the informational environment for financial analysts?

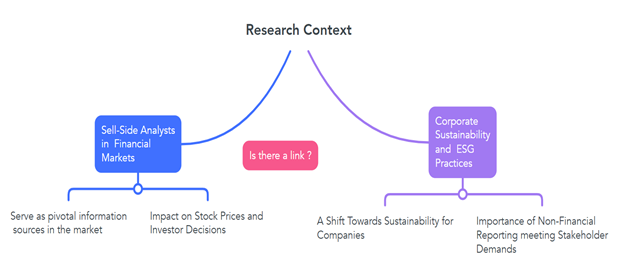

Figure 1 shows the research context in two ways: corporate sustainability and financial analysis.

Diagram Highlighting the Research Context

The paper adopts a comprehensive literature review approach, synthesizing insights from empirical and theoretical studies to identify trends, concepts, and research gaps. This paper also proposes a conceptual framework to better understand how analysts influence corporate sustainability. The framework integrates key findings from the literature and highlights the mechanisms through which financial analysts can drive or respond to ESG disclosures and practices in publicly listed companies.

The context analysis also suggests that financial analysts play a central role in promoting corporate sustainability by encouraging transparency and improving ESG performance. Analyst coverage would also significantly improve the ESG scores of the target company. However, while existing studies provide strong evidence on developed markets, little research focuses on emerging markets. The paper also highlights the need for future research to examine the financial performance of companies with strong ESG commitments that receive ongoing analyst coverage.

The paper is structured as follows. In the first section, we will begin by defining the main concepts in the literature. Then, we will indicate the different theories surrounding analysts’ coverage. In the second section, we will shed light on the results of studies that have examined the interaction between financial analyst coverage and ESG factors. We will then provide a conceptual and theoretical framework to identify unexploited areas for further research.

Main Concepts in the Literature

Investment Value of Sell-Side Analyst Recommendations

This point examines the role of financial analysts as critical information intermediaries in financial markets. Their recommendations influence stock prices, reduce information asymmetries, and shape investment decisions.

Sell-side analysts play a dual role in interpreting and discovering information (Devos et al., 2015). In the latter role, they can collect and process private information that is not always available on the market (Barber et al., 2010; Ivković & Jegadeesh, 2004). In their former role, analysts add value through their skills and ability to analyze specific securities based on public information.

The literature has extensively debated the value of financial analysts' recommendations. Analysts are competent in analyzing and synthesizing private and public information from companies and other sources for investors. Furthermore, they can provide additional information unavailable to investors and assess the covered company's future cash flow prospects (Ivković & Jegadeesh, 2004). Their recommendations contain forward-looking information that helps investors evaluate future cash flows and the company's value.

A substantial body of research has documented the effects of financial analysts' recommendations on stock prices, demonstrating that these reports have investment value (Barber et al., 2001; Bradley et al., 2014; Busse et al., 2012; Jegadeesh & Kim, 2006). Studies have also been conducted on several emerging markets (Bellando et al., 2016; Moshirian et al., 2009; Tiniç et al., 2021; Vukovic et al., 2020), though the findings are not always consistent with those of developed markets.

The seminal study by Womack (1996) highlighted significant positive (negative) price reactions to positive (negative) recommendations. The conclusion that stock prices react significantly to recommendations was subsequently confirmed for the international context (G7 countries) by Jegadeesh and Kim (2006). Further studies showed that an investment strategy of buying (selling) stocks with the most (least) favorable consensus recommendations generates significant abnormal returns (e.g., Barber et al., 2001; Michaely & Womack, 1999). Devos et al. (2015) emphasized that the informational value of financial analysts' recommendations is more significant for stocks traded in less transparent markets. Other authors have highlighted that analysts' reports benefit institutional investors, the primary consumers of sell-side analysis (Frankel et al., 2006). This importance of recommendations increases for small investors, who are less likely to seek relevant information (Kelly & Ljungqvist, 2012).

Analysts’ coverage has several effects on publicly traded companies and the market. It reduces information asymmetries, increases companies' visibility to investors, improves stock liquidity, and generates significant returns (Berrada & Meknassi, 2024). Indeed, analysts play a central role in reducing information asymmetries between insiders and outsiders (Asquith et al., 2005; Hong et al., 2000) and contribute to mitigating agency problems (Fama, 1970; Jensen & Meckling, 1976). Their coverage also enhances market informational efficiency by reducing uncertainty about the value of the covered company (Kothari et al., 2016). Collecting relevant information and transforming it into comprehensible reports improves the quality of information and, consequently, the informational efficiency of the stock market.

While the literature emphasizes the importance of analysts' recommendations, there is little research on how these recommendations adapt to the increasing relevance of ESG factors in investment decisions.

Corporate Sustainability and ESG Practices

Before analyzing how analysts interact with non-financial disclosures, we need to show the growing importance of ESG practices in corporate sustainability and their role in shaping market perceptions and investor decisions.

Over the last two decades, we've seen a move toward economies that can last. ESG practices are how companies can achieve their sustainability objectives. A company's ESG profile shows how much it deals with environmental, social, and governance issues. These issues affect how the company works and how people judge its impact. Companies must do their work while respecting society's rights and not hurting nature. By sticking to environmental, social, and governance rules, many companies have started to use business models that are better for the planet, more acceptable to society, and run in a better way (Arif Khan, 2022; Bunchabusabong et al., 2024; Galletta et al., 2022). Companies are looking for ways to incorporate ESG factors into their decisions. One key move is to add non-financial reports, which help link business value to sustainability goals. People agree that sharing ESG data is vital to show how sustainable a company is, but there's no standard way to do this yet. This needs quick action from those who make the rules. Right now, investors can't get uniform data to spot ESG risks and chances. In their research, Cherkaoui and Cherkaoui (2022) pointed out that we need standards for non-financial reports in countries and worldwide. They also suggest setting up checks to ensure that non-financial info is as trustworthy as financial data.

Eccles et al. (2011) also asked if investors care about companies' ESG performance and policies. They found that investors pay more attention to ESG criteria. Investors prioritize environmental and governance information over social information. It shows a positive change in how the market views sustainability and responsible governance.

To conclude, ESG practices have become a cornerstone of corporate sustainability, influencing how investors and analysts perceive company performance. However, the lack of standardization in ESG reporting remains a challenge for consistent evaluation.

As ESG practices become central to corporate sustainability, financial analysts increasingly face the challenge of assessing their impact on firm performance and market perception, which will be explored in the next section.

Seminal Theories Surrounding the Context

Agency Theory

Developed by Jensen and Meckling (1976), this theory describes the relationship between principals (shareholders) and agents (managers), where conflicts of interest arise due to asymmetric information. Financial analysts act as information intermediaries, reducing asymmetries between management and investors. Good governance (ESG ‘G’) reduces agency conflicts, improves transparency, and makes it easier for analysts to assess company performance correctly.

Stakeholder Theory

Proposed by Freeman (1984), this theory broadens the scope of corporate responsibilities to include all stakeholders (investors, employees, communities, environment). In our research context, financial analysts need to integrate ESG concerns to meet new investor expectations.

Signaling Theory

Introduced by Spence (1973), this theory states that companies use signals to transmit credible information to investors in the context of asymmetric information. Companies that adopt and disclose ESG practices send a positive signal of responsibility and transparency to the market.

Financial analysts use these ESG signals to reduce uncertainty and make more accurate recommendations.

Efficient Market Hypothesis (EMH)

Popularized by Fama (1970), this theory maintains that financial markets quickly and efficiently reflect all available information. Analysts' recommendations influence share prices by disseminating new information to the market. Integrating ESG information into financial analysis improves the informational efficiency of the market by including relevant non-financial data.

Institutional Theory

Developed by DiMaggio and Powell (1983), it explains how companies adopt practices in response to institutional pressures (regulations, social expectations). Analysts play an institutional role, encouraging companies to adopt ESG practices to meet the requirements of investors and regulators. Increased media attention and analysts’ coverage push companies to improve their ESG performance to maintain their legitimacy.

Interaction Between Analysts’ Coverage and ESG Practices in the Literature

This section investigates how financial analysts respond to ESG disclosures and how their coverage influences corporate sustainability practices. Sell-side analysts primarily rely on financial data to evaluate a company's financial performance and forecast future results. However, they may also consider other non-financial parameters likely impacting their evaluation.

Numerous studies have examined whether better disclosure of ESG information influences sell-side analysts' recommendations. Eccles et al. (2011) affirm that the capital market shows great interest in the level of disclosure of companies' ESG practices.

What role does the financial system play in the transition to a green and sustainable economy, and how can this contribution evolve depending on the degree of development of the financial market? These questions are receiving increased attention today due to the rising frequency and impact of environmental disasters caused by climate change and the awareness of environmental issues induced by the COVID-19 pandemic.

Corporate Governance

Financial analysts place significant importance on the governance structure of the companies they follow. According to Lang et al. (2004), analysts will likely follow companies with good internal governance. Boubaker and Labégorre (2008) affirm that analysts follow companies with a high level of disparity between ownership and control. Their Financial Reporting Quality (FRQ) plays a vital role in corporate governance by ensuring transparency within the business environment (Li et al., 2024).

Lin and Tai (2013) examined the impact of corporate governance on analysts' recommendations in an emerging market characterized by more significant information asymmetries and weaker shareholder protection. They concluded that improving corporate governance reduces agency problems, enhances the quality of information produced by financial analysts, and reduces the risks investors face.

Robust corporate governance models have improved sovereign ratings, enhanced financial performance, reduced default risk, and lowered the cost of equity (Umar et al., 2022).

We can conclude that strong corporate governance positively influences analysts’ coverage, providing greater transparency and reducing risks associated with poor governance.

Social Information Disclosure

Ioannou and Serafeim (2014) argue that CSR activities undertaken by a company can affect financial analysts' recommendations in various ways. Al-Shaer (2018) studied the impact of environmental and social information disclosure on analysts' recommendations in the UK market. The quality of such information published and disclosed by companies in their annual reports allows them to receive favorable recommendations from financial analysts. These analysts use voluntarily disclosed information from publicly traded UK companies. Moreover, financial analysts make more accurate forecasts when the information is high quality. Li et al. (2024) confirmed these results in the US market, stating the significant link between CSR and analysts' recommendations and disclosure in a transparent informational environment, such as when family control is lower and a reputable auditor audits the company.

Alazzani et al. (2021) explain that CSR increases value by improving a company's long-term financial performance. Changes in financial performance can have a direct impact on analysts' recommendations. Additionally, the substantial amount of funds invested by socially responsible and environmentally conscious investors in CSR-friendly companies could positively influence these companies' stock prices, thereby impacting analysts' recommendations. Dhaliwal et al. (2011) found that companies that publish more CSR information are more likely to attract institutional investors and be covered by financial analysts. Financial analysts help reduce information asymmetries between investors and companies by incorporating CSR information into their recommendations.

Environmental Information and Innovation

Sustainable development has become a significant feature of economies under carbon neutrality and peak carbon development goals. Zhang and Wilson (2022) explore how financial analysts evaluate stocks related to brown energy (fossil fuels) compared to green energy (renewables). They find that analysts tend to issue more buy recommendations and fewer sell recommendations for brown energy stocks than for green energy stocks, both for initiation and revisions. This optimism for brown energy stocks diminishes significantly after the Paris Agreement period. These findings indicate signs of an effective transition from brown to green energy in how financial analysts evaluate companies' prospects in the energy sector. Moreover, the authors investigated whether financial analysts' recommendations on energy companies hold value for investors. This follows numerous studies on investor reactions to analysts' recommendations (e.g., Loh & Stulz, 2011; Womack, 1996). Zhang and Wilson (2022) find that investors rely on financial analysts' recommendations for energy stocks and act accordingly. However, compared to recommendations on green energy stocks, those on brown energy stocks elicit a weaker reaction from investors, suggesting a discount on the informativeness of analysts' recommendations on brown energy stocks.

Further analysis indicates that this informational discount on brown energy has decreased, and investor confidence in analysts' opinions on brown and green energy stocks has converged in recent years. Griffin et al. (2015) concluded limited investor reactions and predicted a bleak future for brown energy. Miralles-Quirós and Miralles-Quirós (2019) showed that green energy funds outperform brown energy funds, suggesting that stock markets have already adopted the energy transition.

Khatri (2023) examined whether financial markets value a company's environmental performance, namely its energy efficiency. This study highlights the association between energy efficiency and company value. It then tests financial analysts' role in assessing energy efficiency through their coverage of companies. The findings indicate that financial analysts' coverage plays a positive and significant role in the value relevance of energy efficiency. In the context of growing environmental concerns, pressure from climate change, and achieving net-zero carbon emissions, this study provides valuable insights into the financial market, where companies' environmentally responsible behaviors hold value. Examining analysts' evaluation of brown versus green energy stocks helps understand if and how information related to the energy transition circulates in capital markets.

In a study based on a sample of 6,000 publicly traded companies in 56 countries, Fiorillo et al. (2022) investigated the influence of financial analysts on corporate green innovation. The authors find that corporate green innovation positively correlates with the number of financial analysts following the company. A positive link exists between a company's environmental innovation and the number of financial analysts covering the company. The authors attribute this result to the informational role of analysts, whose effect encourages managers to invest more in eco-innovation activities. The informative function of analysts becomes crucial for eco-innovation, which relies on intangible resources requiring correct evaluation of their capabilities. Consequently, as analysts improve information efficiency in the stock market, investors can recognize the net present value of risky long-term investments, such as those related to environmental innovation, encouraging managers to pursue them.

Zhao and Yang (2023) investigated the impact of financial analysts' coverage on the green innovation of highly polluting publicly traded Chinese companies. Financial analysts' coverage can significantly improve the green innovation of highly polluting companies. Various factors can influence corporate green innovation. Analysts' coverage can be considered an external factor and can promote green innovation in two ways. On the one hand, analysts' coverage is perceived as an essential element of external environmental governance for companies. According to institutional theory, pressure from external governance is a significant driving force for corporate green innovation. In the context of green development, increasing attention from analysts will help increase green innovation pressure on highly polluting companies, encouraging them to actively improve their production processes and enhance research and development of green technologies. On the other hand, the information asymmetry between companies and investors increases the difficulty of external financing, thus limiting the sustainability of corporate green innovation. In this case, analysts' dissemination of information on green innovation can also help external investors track the progress of green technology development, reducing financing constraints and improving green innovation in polluting companies.

Environmental issues are becoming increasingly severe, and the level of corporate green innovation needs improvement. Financial analysts' coverage can mitigate information asymmetry, exert stakeholder governance pressure, and enhance the green innovation performance of polluting companies. Analysts are essential information intermediaries in the capital market and are a significant factor in companies' external environmental governance.

In short, analysts influence companies’ ESG practices by focusing on governance, social responsibility, and environmental innovation. This influence, particularly in areas like green innovation, is well-documented. However, the role of analysts in shaping ESG priorities in highly polluting industries remains underexplored. Table 1 presents key literature insights categorized by ESG dimensions.

Key Literature Insights Categorized by ESG Dimensions

|

ESG Component |

Authors |

Topic |

Conclusion |

|

Governance |

Corporate governance and analyst coverage |

Analysts favor companies with strong governance |

|

|

Ownership and governance disparities |

Governance disparities attract analysts |

||

|

Governance impact on recommendations in emerging markets |

Improved governance reduces agency problems |

||

|

Social

|

CSR activities and recommendations |

CSR positively affects analysts’ recommendations |

|

|

Environmental and Social Disclosure in the UK |

High-quality ESG disclosure receives favorable recommendations |

||

|

CSR practices in the Malaysian market |

Transparent CSR improves recommendation quality |

||

|

CSR and long-term financial performance |

CSR improves long-term performance and stock prices |

||

|

Environmental

|

Brown vs green energy stock recommendations |

Analysts shift focus to green energy post-Paris Agreement |

|

|

Energy efficiency and company value |

Analyst coverage positively impacts energy efficiency |

||

|

Green innovation and analyst coverage |

Green innovation correlates with analyst coverage |

||

|

Green innovation in polluting companies |

Analyst coverage enhances green innovation performance |

ESG Scores and Analysts’ Forecasts

We cannot discuss ESG factors without examining the ESG scores of listed companies. This section examines the bidirectional relationship between ESG scores and analysts’ coverage.

In their paper, Umar et al. (2022) evaluate the relationship between ESG scores and the accuracy of price targets issued by financial analysts on covered companies. The authors focus on companies covered in BRICS countries between 2011 and 2021. The results demonstrate that ESG scores positively impact the accuracy of price targets. Companies with high ESG scores are likely to have fewer forecast errors. According to their study, environmental and governance factors largely explain the accuracy of forecasts, while social aspects do not have a significant impact. These findings are important for investors.

It has been proven that intensifying ESG activities increases a company's free cash flows (Gregory, 2022). Companies compliant with ESG standards tend to have more predictable cash flows and discount rates, which impacts the accuracy of financial analysts' forecasts that rely on cash flow discounting methods. The precision of financial analysts' recommendations is positively associated with the company's ESG scores.

Several studies have explored the influential role of financial analysts in promoting the ESG performance of target companies. Gao et al. (2023) found that financial analysts' coverage significantly improves the ESG scores of target companies in the Chinese market. The authors explored how analysts' coverage promotes enhancing companies' ESG performance. One key mechanism is that analysts' coverage empowers companies to become more aware of ESG issues by producing ESG-focused information. Analysts' coverage is more significant for companies exposed to higher environmental and reputational risks. The authors find that the promoting effect of analysts' coverage on companies' ESG performance is more substantial in companies with higher agency costs.

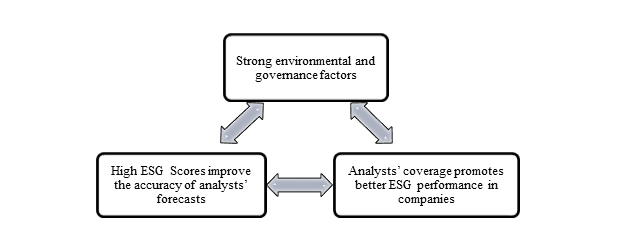

In sum, high ESG scores improve the accuracy of analysts’ forecasts, particularly through string environmental and governance factors, while analysts’ coverage promotes better ESG performance in companies (see Figure 2). This mutual relationship enhances both forecast reliability and corporate commitment to sustainability.

The ESG-Analysts Feedback Loop: Driving Performance and Forecast Accuracy

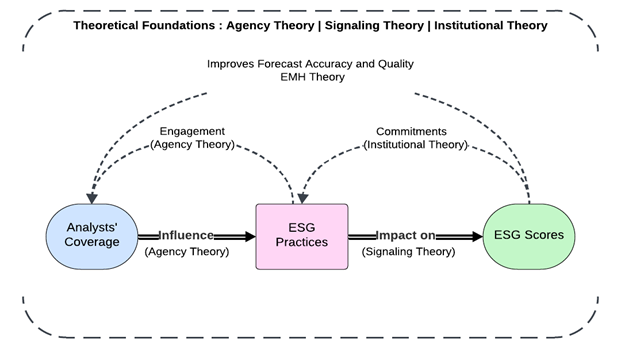

Proposed Conceptual and Theoretical Framework

The literature review reveals a dynamic relationship between analysts' coverage, ESG practices, and ESG scores. The proposed conceptual framework, as displayed in Figure 3, builds on these findings to provide a structured lens for analyzing interactions grounded in seminal theories such as Agency, Signaling, and Institutional Theory. The framework highlights the role of analysts as information intermediaries promoting corporate sustainability and how ESG performance enhances market transparency and forecast accuracy.

Integrated Conceptual and Theoretical Framework Illustrating the Interaction Between Analysts' Coverage, ESG Practices, and ESG Scores, Supported by Key Theories

Figure 3 highlights that analysts influence ESG adoption, while ESG scores improve forecast quality and encourage stronger ESG commitments, creating a reinforcing cycle of transparency and sustainability.

Under Agency theory, ESG practices, particularly in governance, strengthen analysts' confidence by improving transparency and reducing agency risks. The impact of ESG factors on ESG scores relies on the Signaling Theory, where ESG scores and non-financial reports serve as quality signals for analysts and investors.

Furthermore, ESG information reduces information asymmetries and enables a better assessment of risks and opportunities that could impact market efficiency. The feedback loop between ESG scores and ESG practices highlights institutional theory, as good ESG scores create external pressures that reinforce companies' ESG commitments. Environmental and social factors are becoming institutional standards that companies must follow to remain competitive.

This framework presents a structure to recognize the interactive dynamics between the analysts and ESG factors, their collective impact on the corporate sustainability phenomenon, and their outcome in enhancing the efficiency of the markets. It answers our research questions and establishes two dual factors of financial analysts: their impact on ESG practices and forecast accuracy through higher ESG scores.

Future Research Propositions

This literature review highlighted several important gaps in the existing literature and promising avenues for further research into the interactions between financial analyst coverage and ESG practices.

Most of the current studies focus on developed markets, where data is more accessible and ESG practices more mature. However, emerging markets present different dynamics in terms of the adoption of ESG practices, quality of information, and coverage by financial analysts.

Furthermore, although ESG is often studied as a whole, it is compulsory to analyze the three dimensions (environmental, social, and governance) separately to understand their impact on analyst recommendations and company performance.

To address these shortcomings, several lines of investigation can be envisaged. These could include empirical studies of the long-term financial effects of ESG recommendations on companies, a comparative analysis between developed and emerging markets, and a long-term financial impact of ESG recommendations on green innovation. These studies aim to determine whether adopting sustainable technologies and practices leads to better financial performance and long-term value for companies.

Conclusion

Sustainability is currently at its peak, at the heart of concerns for executives, investors, regulators, management students, and the public. In the new era of sustainable finance, companies face mounting stakeholder pressure to engage in ESG activities. This pressure drives them to integrate ESG objectives into their core activities, reflecting the increasing demand from a broader range of stakeholders. However, a recent wave of researchers underscores that ESG considerations should not overshadow other factors. Edmans (2023) emphasizes that ESG practices should transition from a niche sub-domain to a common practice. ESG should be considered alongside other intangible assets influencing financial and social value, such as management quality, corporate culture, and innovation capacity.

This article explored the role of financial analysts in promoting and evaluating the ESG practices of listed companies while proposing a conceptual and theoretical framework to illustrate these dynamics. The main results show that analysts, as information intermediaries, have a positive influence on the adoption and transparency of ESG practices while at the same time benefiting from the improved accuracy of their forecasts as a result of these disclosures. This dynamic relationship benefits the companies and contributes to the broader goal of creating sustainable and resilient financial markets.

This study contributes to the literature by enriching debates on analysts’ coverage and its interaction with ESG practices. It provides an integrated framework for analyzing these relationships from several theoretical perspectives, highlighting the role of analysts as catalysts for transparency and sustainability in financial markets. For companies, these results show that better disclosure of ESG practices can attract increased analysts’ coverage, improving their visibility and reputation with investors. At the same time, financial analysts are encouraged to integrate ESG criteria into their valuations to meet the growing expectations of responsible investors and regulators. Figure 4 synthesizes key contributions to analysts' coverage and ESG sustainability outcomes.

Key Contributions to Analysts' Coverage and ESG Sustainability Outcomes

References

Al-Shaer, H. (2018). Do environmental-related disclosures help enhance investment recommendations? UK-based evidence. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-03-2016-0020

Alazzani, A., Wan-Hussin, W. N., Jones, M., & Al-hadi, A. (2021). ESG Reporting and Analysts’ Recommendations in GCC: The Moderation Role of Royal Family Directors. Journal of Risk and Financial Management, 14(2), 1–20. https://doi.org/10.3390/jrfm14020072

Altinkiliç, O., & Hansen, R. S. (2009). On the information role of stock recommendation revisions. Journal of Accounting and Economics, 48(1), 17–36. https://doi.org/10.1016/j.jacceco.2009.04.005

Arif Khan, M. (2022). ESG disclosure and Firm performance: A bibliometric and meta analysis. Research in International Business and Finance, 61. https://www.sciencedirect.com/science/article/abs/pii/S0275531922000563?via%3Dihub

Asquith, P., Mikhail, M. B., & Au, A. S. (2005). Information content of equity analyst reports. Journal of Financial Economics, 75(2), 245–282. https://doi.org/10.1016/j.jfineco.2004.01.002

Barber, B., Lehavy, R., McNichols, M., & Trueman, B. (2001). Can investors profit from the prophets? Security analyst recommendations and stock returns. Journal of Finance, 56(2), 531–563. https://doi.org/10.1111/0022-1082.00336

Barber, B. M., Lehavy, R., & Trueman, B. (2010). Ratings changes, ratings levels, and the predictive value of analysts’ recommendations. Financial Management, 39(2), 533–553. https://doi.org/10.1111/j.1755-053X.2010.01083.x

Beaver, W., Cornell, B., Landsman, W. R., & Stubben, S. R. (2008). The impact of analysts’ forecast errors and forecast revisions on stock prices. Journal of Business Finance and Accounting, 35(5–6), 709–740. https://doi.org/10.1111/j.1468-5957.2008.02079.x

Bellando, R., Ben Braham, Z., & Galanti, S. (2016). The profitability of financial analysts’ recommendations: evidence from an emerging market. Applied Economics, 48(46), 4410–4418. https://doi.org/10.1080/00036846.2016.1158918

Berrada, F., & Meknassi, S. (2024). Effets du suivi des entreprises cotées en bourse par les analystes financiers : une revue de littérature. International Journal of Accounting Finance Auditing Management and Economics, 5(4), 383–396. https://doi.org/10.5281/zenodo.11001359

Boubaker, S., & Labégorre, F. (2008). Ownership structure, corporate governance and analyst following: A study of French listed firms. Journal of Banking and Finance, 32(6), 961–976. https://doi.org/10.1016/j.jbankfin.2007.07.010

Bradley, D., Clarke, J., Lee, S., & Ornthanalai, C. (2014). Are analysts’ recommendations informative? Intraday evidence on the impact of time stamp delays. Journal of Finance, 69(2), 645–673. https://doi.org/10.1111/jofi.12107

Bunchabusabong, K., Tiwasuppachai, J., & Kunathikornkit, S. (2024). Comparative analysis of sustainability communication strategies of Thai and global brand restaurants on social media and websites. European Journal of Studies in Management and Business, 32, 28-59. https://doi.org/10.32038/mbrq.2024.32.02

Busse, J. A., Clifton Green, T., & Jegadeesh, N. (2012). Buy-side trades and sell-side recommendations: Interactions and information content. Journal of Financial Markets, 15(2), 207–232. https://doi.org/10.1016/j.finmar.2011.08.001

Cherkaoui, A., & Cherkaoui, Z. (2022). Du reporting de la performance globale à la stratégie de reporting ESG : pratiques des entreprises faisant appel public à l’épargne au Maroc [From overall performance reporting to ESG reporting strategy: practices of companies making public appeals to savings in Morocco]. Revue Congolaise de Gestion, 32(2). https://doi.org/10.3917/rcg.032.0131

Devos, E., Hao, W., Prevost, A. K., & Wongchoti, U. (2015). Stock return synchronicity and the market response to analyst recommendation revisions. Journal of Banking and Finance, 58, 376–389. https://doi.org/10.1016/j.jbankfin.2015.04.021

Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Accounting Review, 86(1), 59–100. https://doi.org/10.2308/accr.00000005

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.1515/9780691229270-005

Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835–2857. https://doi.org/10.1287/mnsc.2014.1984

Eccles, R. G., Serafeim, G., & Krzus, M. P. (2011). Market interest in nonfinancial information. Journal of Applied Corporate Finance, 23(4), 113–127. https://doi.org/10.1111/j.1745-6622.2011.00357.x

Edmans, A. (2023). The end of ESG. Financial Management, 52(1), 3–17. https://doi.org/10.1111/fima.12413

Fama, E. F. (1970). Efficient market hypothesis: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417.

Fiorillo, P., Meles, A., Mustilli, M., & Salerno, D. (2022). How does the financial market influence firms’ Green innovation? The role of equity analysts. Journal of International Financial Management and Accounting, 33(3), 428–458. https://doi.org/10.1111/jifm.12152

Frankel, R., Kothari, S. P., & Weber, J. (2006). Determinants of the informativeness of analyst research. Journal of Accounting and Economics, 41(1–2), 29–54. https://doi.org/10.1016/j.jacceco.2005.10.004

Freeman, R. . (1984). Strategic Management: a Stakeholder Approach.

Galletta, S., Mazzù, S., & Naciti, V. (2022). A bibliometric analysis of ESG performance in the banking industry: From the current status to future directions. Research in International Business and Finance, 62. https://doi.org/10.1016/j.ribaf.2022.101684

Gao, H., Wang, H., & Wen, H. (2023). Does Analyst coverage affect corporate ESG performance? evidence from China. SSRN Electronic Journal, 59, 1–41. https://doi.org/10.2139/ssrn.4425095

Gillan, S. L., Koch, A., & Starks, L. T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66(June 2020), 101889. https://doi.org/10.1016/j.jcorpfin.2021.101889

Gregory, R. P. (2022). ESG activities and firm cash flow. In Global Finance Journal, 52. https://doi.org/10.1016/j.gfj.2021.100698

Griffin, P. A., Jaffe, A. M., Lont, D. H., & Dominguez-Faus, R. (2015). Science and the stock market: Investors’ recognition of unburnable carbon. Energy Economics, 52, 1–12. https://doi.org/10.1016/j.eneco.2015.08.028

Hong, H., Kubik, J. D., & Solomon, A. (2000). Security analysts’ career concerns and herding of earnings forecasts. The RAND Journal of Economics, 31(1), 121. https://doi.org/10.2307/2601032

Ioannou, I., & Serafeim, G. (2014). The impact of corporate social responsibility on investment recommendations: analysts’ perceptions and shifting institutional logics. Strategic Management Journal, 1–43. https://doi.org/10.1002/smj

Ivković, Z., & Jegadeesh, N. (2004). The timing and value of forecast and recommendation revisions. Journal of Financial Economics, 73(3), 433–463. https://doi.org/10.1016/j.jfineco.2004.03.002

Jegadeesh, N., & Kim, W. (2006). Value of analyst recommendations: International evidence. Journal of Financial Markets, 9(3), 274–309. https://doi.org/10.1016/j.finmar.2006.05.001

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm : managerial behavior , agency costs and ownership structure related papers. Journal of Financial Economics, 3(4), 305–360. http://hupress.harvard.edu/catalog/JENTHF.html%0AAlso

Kelly, B., & Ljungqvist, A. (2012). Testing Asymmetric-Information Asset Pricing Models. 212. https://doi.org/10.1093/rfs/hhr134

Khatri, I. (2023). The role of analyst coverage and value-relevance of energy efficiency. Review of Accounting and Finance, 22(2), 249–265. https://doi.org/10.1108/RAF-08-2022-0211

Kothari, S. P., So, E. C., & Verdi, R. (2016). Analysts ’ forecasts and asset pricing : A survey. Annual Review of Financial Economics, 8, 197–219. https://doi.org/10.1146/annurev-financial-121415-032930

Lang, M. H., Lins, K. V., & Miller, D. P. (2004). Concentrated control, analyst following, and valuation: Do analysts matter most when investors are protected least? Journal of Accounting Research, 42(3), 589–623. https://doi.org/10.1111/j.1475-679X.2004.t01-1-00142.x

Li, Z., Athanasiadis, K.A., Fygkioris, M.I., Koufopoulos, D.N. (2024). Financial reporting quality, CEO age, and investment efficiency: Evidence from the U.S. market. New Challenges in Accounting and Finance, 11, 29-53. https://doi.org/10.32038/NCAF.2024.11.03

Lin, J., & Tai, V. W. (2013). Corporate governance and analyst behavior : Evidence from an emerging market. Asia-Pacific Journal of Financial Studies, 42(1), 228–261. https://doi.org/10.1111/ajfs.12013

Loh, R. K., & Stulz, R. M. (2011). When are analyst recommendation changes influential? Review of Financial Studies, 24(2), 593–627. https://doi.org/10.1093/rfs/hhq094

Michaely, R., & Womack, K. L. (1999). Conflict of interest and the credibility of underwriter analyst recommendations. Review of Financial Studies, 12(4), 653–686. https://doi.org/10.1093/rfs/12.4.653

Miralles-Quirós, J. L., & Miralles-Quirós, M. M. (2019). Are alternative energies a real alternative for investors? Energy Economics, 78, 535–545. https://doi.org/10.1016/j.eneco.2018.12.008

Moshirian, F., Ng, D., & Wu, E. (2009). The value of stock analysts’ recommendations: Evidence from emerging markets. International Review of Financial Analysis, 18(1–2), 74–83. https://doi.org/10.1016/j.irfa.2008.11.001

Ramnath, S., Rock, S., & Shane, P. (2008). The financial analyst forecasting literature: A taxonomy with suggestions for further research. International Journal of Forecasting, 24(1), 34–75. https://doi.org/10.1016/j.ijforecast.2007.12.006

Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374.

Stickel, S. (1995). The anatomy of the performance of buy and sell recommendations. Financial Analysts Journal. https://doi.org/10.2469/faj.v51.n5.1933

Tiniç, M., Tanyeri, B., & Bodur, M. (2021). Who to trust? Reactions to analyst recommendations of domestic versus foreign brokerage houses in a developing stock market. Finance Research Letters, 43(October 2020). https://doi.org/10.1016/j.frl.2021.101950

Umar, M., Mirza, N., Rizvi, S. K. A., & Naqvi, B. (2022). ESG scores and target price accuracy: Evidence from sell-side recommendations in BRICS. International Review of Financial Analysis, 84. https://doi.org/10.1016/j.irfa.2022.102389

Vukovic, D., Ugolnikov, V., & Maiti, M. (2020). Analyst says a lot, but should you listen? Evidence from Russia. Journal of Economic Studies, 47(4), 729–745. https://doi.org/10.1108/JES-10-2018-0352

Wan-hussin, W. N., Qasem, A., Aripin, N., & Ariffin, M. S. (2021). Corporate responsibility disclosure, information environment and analysts ’ recommendations : evidence from Malaysia. Sustainability, 13, 1–27. https://doi.org/10.3390/su13063568

Womack, K. L. (1996). Do brokerage analysts’ recommendations have investment value ? The Journal of Finance, 51(1), 137–167. https://doi.org/10.1111/j.1540-6261.1996.tb05205.x

Zhang, X., & Wilson, C. (2022). Transition from brown to green: Analyst optimism, investor discount, and Paris Agreement. Energy Economics, 116. https://doi.org/10.1016/j.eneco.2022.106391

Zhao, X., & Yang, M. (2023). Can analyst coverage improve green innovation?- Empirical research based on China’s heavy polluting enterprises. SHS Web of Conferences, 163, 03019. https://doi.org/10.1051/shsconf/202316303019

Page 1 of

Download Count : 45

Visit Count : 134

Keywords

Analyst Coverage; ESG Practices; Corporate Sustainability; Financial Markets; Sustainable Finance

Author(s) Information

How to cite tis article

Berrada, F., & Meknassi, S. (2024). Financial analysts and ESG factors in listed companies: A critical review and future directions. New Challenges in Accounting and Finance, 12, 14-29. https://doi.org/10.32038/NCAF.2024.12.02

Acknowledgments

Not applicable.

Funding

Not applicable.

Conflict of Interests

No, there are no conflicting interests.

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/