Review Article

Fintech and SME Financial Inclusion: A Systematic Literature Review and Bibliometric Analysis

- Abstract

- Full text

- Metrics

Small and Medium-Sized Enterprises (SMEs) continue to encounter significant obstacles in securing finance, often due to information asymmetry, limited credit histories, and inadequate collateral. Developments in Financial Technology (FinTech) have reshaped capital access by enhancing information exchange, reducing transaction costs, and introducing alternative financing models. This study offers a systematic review of empirical research on FinTech and SME financial inclusion between 2008 and 2025, using scientific methods such as PRISMA, PSALSAR, Biblioshiny, and Bibliometrix in RStudio. The findings indicate a relatively recent and fragmented body of literature, with a concentration of studies in China, Indonesia, and other emerging economies. Evidence consistently supports FinTech’s contribution to mitigating financing barriers, particularly in developing contexts. Nonetheless, notable limitations remain, such as a dependence on secondary data, restricted geographic scope, and a scarcity of longitudinal analyses. The paper identifies these gaps and proposes directions for future research to better understand how FinTech can foster sustainable and inclusive financing for SMEs in diverse economic environments.

Fintech and SME Financial Inclusion: A Systematic Literature Review and Bibliometric Analysis

|

1 Professor Habilitation to conduct research (HDR), Doctor in Finance & Banking & Fintech, Groupe ISCAE, Morocco 2 Internal Auditor, PhD Candidate in Finance, Groupe ISCAE, Morocco |

ABSTRACT

Small and Medium-Sized Enterprises (SMEs) continue to encounter significant obstacles in securing finance, often due to information asymmetry, limited credit histories, and inadequate collateral. Developments in Financial Technology (FinTech) have reshaped capital access by enhancing information exchange, reducing transaction costs, and introducing alternative financing models. This study offers a systematic review of empirical research on FinTech and SME financial inclusion between 2008 and 2025, using scientific methods such as PRISMA, PSALSAR, Biblioshiny, and Bibliometrix in RStudio. The findings indicate a relatively recent and fragmented body of literature, with a concentration of studies in China, Indonesia, and other emerging economies. Evidence consistently supports FinTech’s contribution to mitigating financing barriers, particularly in developing contexts. Nonetheless, notable limitations remain, such as a dependence on secondary data, restricted geographic scope, and a scarcity of longitudinal analyses. The paper identifies these gaps and proposes directions for future research to better understand how FinTech can foster sustainable and inclusive financing for SMEs in diverse economic environments.

KEYWORDS:

Fintech, Financial Inclusion, Small and Medium-sized Enterprises, Systematic Literature Review, Bibliometric Analysis

JEL Classification:

G10, G30, O16

Introduction

Small and Medium-sized Enterprises (SMEs) are recognized globally as engines of economic development, contributing significantly to employment, innovation, and Gross domestic product (GDP), especially in developing and emerging economies. Despite their macroeconomic relevance, SMEs face persistent challenges in accessing formal financial services due to limited collateral, high-risk perceptions by traditional lenders, and information asymmetries (Beck & Demirguc-Kunt, 2006; Sanga & Aziakpono, 2023).

Financial inclusion, the provision of affordable and appropriate financial services, has emerged as a critical mechanism to alleviate these challenges and empower SMEs. The rapid development of Financial Technology (FinTech) offers novel pathways to enhance financial inclusion, particularly through tools such asobile banking, peer-to-peer (P2P) lending, crowdfunding, and blockchain-based solutions (Gomber et al., 2017; Ha et al., 2025). These technologies have disrupted traditional financial intermediation, increasing access, lowering transaction costs, and improving service quality (Arner et al., 2017).

Several studies have investigated how FinTech can catalyze inclusive finance for SMEs. For instance, Barroso and Laborda (2022) highlight how digital transformation within the FinTech sector is reconfiguring financial ecosystems to be more inclusive. Jain et al. (2023) argue that understanding the evolving risk landscape of FinTech is crucial to designing policies that ensure sustainable inclusion. In parallel, Suryono et al. (2020) emphasize the importance of managing both technological and institutional challenges to harness FinTech effectively in developing economies.

Despite this growing body of work, existing research remains fragmented. Much of the literature focuses on specific FinTech innovations or country-level case studies, without a holistic synthesis of findings related specifically to SME financial inclusion (Afjal, 2023; Lee & Shin, 2018). Moreover, there is a lack of integrated analyses that combine systematic review methodologies with bibliometric insights to track the evolution of scholarly discourse (Lee & Teo, 2015; Tello-Gamarra et al., 2022). This limits our understanding of the conceptual structure, influential actors, and emerging trends within the field.

Furthermore, the role of contextual factors, such as regulatory frameworks, digital infrastructure, and financial literacy, remains underexplored in the discourse on FinTech-enabled financial inclusion (Firmansyah et al., 2022). These factors are particularly relevant in developing and emerging economies, where the promise of FinTech often collides with systemic constraints.

To our knowledge, no systematic literature review has specifically examined the impact of FinTech on the financial inclusion of SMEs. While some reviews address financial inclusion more broadly, they often overlook the unique challenges and opportunities FinTech presents for SMEs.

To address these gaps, the present study undertakes a systematic literature review combined with a bibliometric analysis of articles published from 2008 to 2025 to evaluate how FinTech is influencing the financial inclusion of SMEs. The research is guided by the following questions:

What are the empirical publication trends on FinTech and the financial inclusion of SMEs?

What insights can be drawn from the empirical literature regarding the impact of FinTech on the financial inclusion of SMEs?

What are the current research gaps, challenges, and future research directions in the field of FinTech and SME financial inclusion?

This study offers a timely and comprehensive synthesis of the literature, mapping the evolution of scholarly interest in this area while identifying thematic clusters and future directions. It contributes not only to academic knowledge but also provides actionable insights for policymakers, financial institutions, and SME support organizations seeking to enhance financial inclusion through technological innovation.

Method

A Systematic Literature Review (SLR) is a standardized, transparent, scientific, and replicable method for identifying, evaluating, and synthesizing existing research (Tranfield et al., 2003; Xiao & Watson, 2019). To enhance methodological transparency and rigor, systematic reviews commonly rely on structured protocols such as the PRISMA guidelines (Page et al., 2021) and the PSALSAR framework (Mengist et al., 2020), which provide comprehensive guidance for reporting, appraisal, synthesis, and analysis.

Consistent with prior research in environmental science, social science, and economics, this study applies the PSALSAR and PRISMA protocols to ensure transparency and rigour (Ismail et al., 2021; Mengist et al., 2020; Yu et al., 2022). PSALSAR, offers a sequential structure for evaluating literature, identifying gaps, and mapping thematic trends. PRISMA, initially designed for health research, has been widely adopted in business and finance to standardize the reporting of systematic reviews. The revised PRISMA 2020 version includes a checklist that guides the review process, from formulating objectives to selecting and synthesizing relevant studies (Page et al., 2021).

PSALSAR Framework

|

Steps |

Outcomes |

Methods |

|

|

Protocol |

Scope of the study |

Scope |

Review studies about the how FinTech impacted SME financial inclusion for the period 2008–2025 |

|

Search |

Search strategy |

Search databases |

Scopus and World of Science |

|

|

|

Search strings Key Words |

Related Words |

|

|

|

FinTech |

"Financial Technology" OR “Fintech” OR “FinTech Solutions” OR "Blockchain" OR "Mobile" OR "Digital" OR "Crowdfunding" OR "Crowd-lending" OR "Mobile Money" OR "Mobile Payments" OR "Digital Payment" OR "Marketplace Lending" OR "Peer-to-Peer lending" OR "P2P" OR "Alternative Financing" |

|

|

|

AND |

|

|

|

|

SME |

SMEs" OR "SME" OR "Small Businesses" OR "Small Firms" OR "Small and Medium Enterprises" OR "MSMEs" OR "Micro, Small, and Medium Enterprises" OR "Micro, Small, and Medium-Sized Enterprises" OR "Startups" |

|

Steps |

Outcomes |

Methods |

|

|

|

|

Financial Inclusion |

"Financial Inclusion" OR "Financial Access" OR "Finance" OR "Credit" OR "Loan" OR "Access to Finance" OR "Inclusive Finance" OR "Access to Financial Services" OR "Banking Inclusion" OR "Economic Inclusion" OR "Access to Credit" OR "Underbanked" |

|

Appraisal |

Selection of publication |

Methodology |

- PRISMA flow chart and checklist |

|

|

|

Eligibility |

Inclusion criteria: - Language: English - Year: 2008 to 2025 - Subject Area: Economics, Econometrics and Finance, social science, management, business, banking and finance, computer science and development studies - Document Type: Peer- reviewed articles, book chapters, and conference material Exclusion criteria: - Any content not related to FinTech and SME financing - Proceedings papers, early access, editorial material and review articles |

|

Synthesis |

Data extraction and categorization |

- Data extraction template is based on the PRISMA checklist - Excel, Mendeley and Bibliometrix R software are employed to categorize data for further analysis |

|

|

Analysis |

Data analysis |

- Descriptive analysis, content analysis and literature classification |

|

|

|

Results and discussion |

- Combining the findings and drawing conclusions and recommendations |

|

|

Report |

Article writing |

- Presenting the findings and recommendations in journal article format |

|

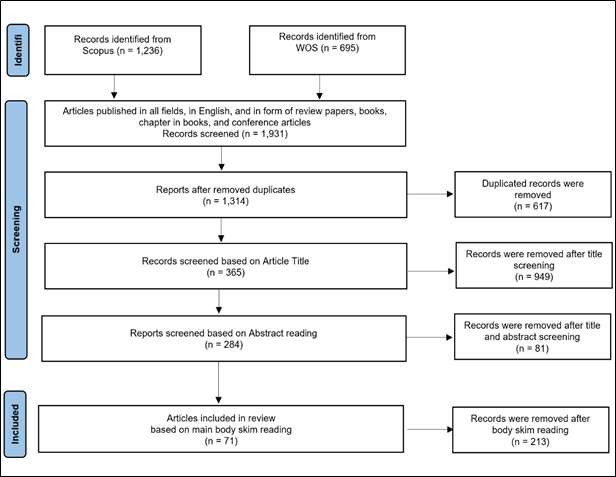

This study utilizes two leading academic databases, Scopus and Web of Science (WoS), both of which are globally recognized citation indexing platforms commonly employed in systematic literature reviews (Singh et al., 2021; Zhu & Liu, 2020). The search strategy and article selection process were guided by the structured protocols of PSALSAR (Mengist et al., 2020) and PRISMA (Page et al., 2021), as detailed in Table 1 and illustrated in Figure 1 from 2008 to 2025, when FinTech 3.0 started. For data organization and analysis, the study used Mendeley for reference management, Bibliometrix R for bibliometric analysis (Aria & Cuccurullo, 2017; R Core Team, 2024), and Excel for classification and synthesis (Barroso & Laborda, 2022; Kaur et al., 2021).

PRISMA Flowchart for Screening Process on Systematic Literature Review

Artificial Intelligence (AI) tools were employed in this study to enhance the clarity and readability of certain sections through paraphrasing, ensuring the text remained precise and accessible without altering its meaning. AI assistance was also used in a limited capacity to support minor aspects of the study design to improve the logical flow of the review framework. All substantive analysis, interpretation, and conclusions were conducted and validated by the authors.

Results from Bibliometric Analysis

The following subsection addresses research question 1 by presenting a bibliometric analysis of publication trends in the empirical literature on FinTech and SME financial inclusion, based on the 71 studies identified through the systematic review process.

Publication Trends Over Time and Location

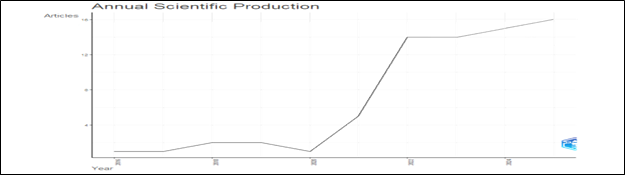

FinTech 3.0, which began around 2008 following the global financial crisis, marked a shift toward technology-driven financial services led by startups and digital platforms (Arner et al., 2017). However, empirical research examining the intersection of FinTech and SME financing remained limited until 2016 and only gained significant momentum nearly a decade later. According to the findings of this review, scholarly interest in this area has grown rapidly since 2021, with 83% of the selected empirical articles published between 2022 and 2025, reflecting increased attention to digital financial inclusion in the post-pandemic context. The publications increased by 7% in 2025, with a total of 16 articles recorded through October 2025, compared to the full-year count of 15 articles in 2024. This surge may be attributed to greater data availability and the accelerated adoption of digital financial services. As shown in Figure 2, this trend highlights the expanding academic focus on the role of FinTech in addressing SME financing gaps.

Publication Trends Over Time

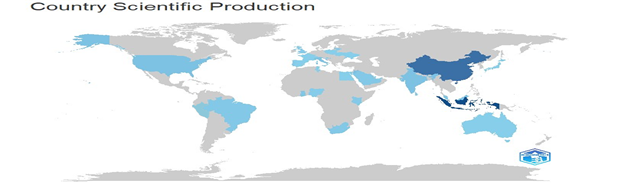

The analysis of country-level contributions reveals a strong concentration in Asia, with Indonesia (71 articles) and China (51) accounting for the majority of empirical studies on FinTech and SME financing. Jordan (9), the United States (8), and India (7) also feature prominently, while representation from Africa remains limited, with only Ghana, South Africa, Kenya, and Nigeria contributing multiple studies. This geographic distribution reflects both data availability and regional prioritization of digital financial inclusion (see Figure 3).

Institutionally, Udayana University (Indonesia) leads with 9 publications, followed by the Chinese universities Dongbei University of Finance and Economics with 6 publications, and Jiangsu University of Science and Technology with 5, underscoring Asia’s academic engagement with the topic. However, the overall pattern highlights notable underrepresentation from much of Africa, the Middle East, and Latin America, suggesting opportunities for broader global inquiry into FinTech’s role in SME financing.

Publication Trends Over Location

Publications based on FinTech and SME Financial Inclusion Trends

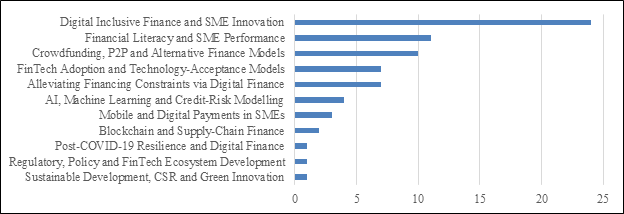

As illustrated in Figure 4, the empirical literature on FinTech and SMEs coalesces around eleven thematic clusters, with a strong emphasis on reducing financing constraints, improving SME performance, fostering innovation, and advancing financial inclusion. The leading trend, Digital Inclusive Finance and SME Innovation (24 articles), reflects the central role of digital tools in driving SME growth. This is followed by significant focus areas such as Financial Literacy (11), Alternative Finance Models like crowdfunding and P2P (10), FinTech Adoption (7), and efforts to alleviate financing constraints (9). Other relevant topics include the use of AI and credit-risk modelling (4), and mobile payments (3). Niche themes such as blockchain, post-COVID resilience, sustainability, and regulation are also explored, though less extensively. These trends highlight FinTech’s growing influence on SME access to finance, innovation, and digital transformation.

Trend of Empirical Publications on FinTech and SME Financial Inclusion

Publications Based on the Methodology Used

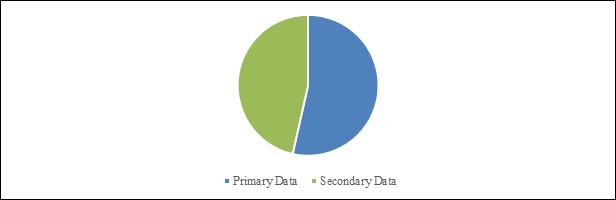

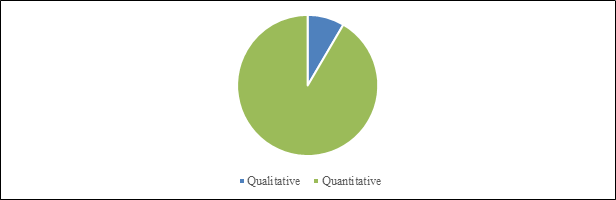

After analyzing 71 peer-reviewed publications on fintech and SME financing, we observed a clear methodological orientation across data sources, data types, and analytical approaches. Out of the total, 38 studies relied on primary data while 33 used secondary data, as indicated in Figure 5. Figure 6 highlights a significant majority (65 publications) adopting quantitative methods, whereas only 6 employed qualitative approaches

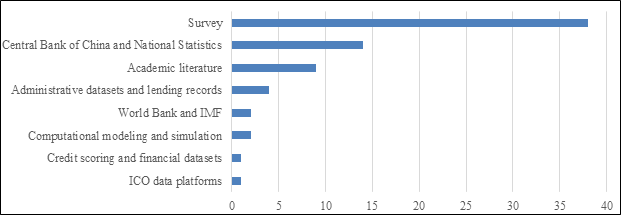

Regarding data sources, surveys were the most frequently used, appearing in 38 articles. This was followed by national statistics and datasets from the Central Bank of China (14 articles), academic literature (9), and administrative datasets and lending records (4). Other sources included computational modeling and simulation (2) and international organizations like the World Bank and International Monetary Fund (IMF) (2), or the use of credit scoring datasets, Initial Coin Offering (ICO) platforms (1 each).

Overall, the analysis reveals a strong emphasis on empirical and survey-based research, as reflected in Figure 7, with a focus on firm-level and individual-level data. The limited use of global datasets suggests that research in this domain tends to be rooted in national or local contexts, reflecting the diverse financial ecosystems and regulatory environments across countries.

Trend of Publications by Type of Data

Figure 6

Trend of Publications by Methodology

Figure 7

Trend of Publications Based on Data Sources

Findings from Content Analysis

This section addresses research question 2, which explores the insights from empirical literature on the impact of FinTech on the financial inclusion of SMEs. The findings reveal that FinTech contributes to SME inclusion through two primary channels. First, by expanding access to essential financial services such as credit, payments, and savings, especially for underserved or informal businesses. Second, by driving improved financial performance and resilience through digital tools, platforms, and financial literacy enhancement. Accordingly, the literature is structured into two key categories: FinTech-driven access to financial services for SMEs and FinTech-enabled performance enhancement for SMEs as sown in Table 1 and Table 2, respectively.

FinTech-driven Access to Financial Services for SMEs

FinTech significantly enhances SME financial inclusion through multiple pathways. It alleviates financing constraints by reducing capital costs, streamlining fund sourcing, managing leverage, and enabling more strategic asset allocation (Chen & Yoon, 2022; Feng et al., 2023; Ismanto et al., 2023). Digital financial literacy and user confidence play a crucial role in unlocking these benefits, especially when supported by platforms like social media (Mutamimah & Indriastuti, 2023; Rahadian & Thamrin, 2023).

Artificial Intelligence (AI) -driven credit scoring and big data analytics have revolutionized SME credit assessment, improving lending decisions (Malakauskas & Lakstutiene, 2021). Moreover, alternative financing models offer democratized, flexible access to capital, especially in early-stage and underserved markets (Mdoe & Kinyanjui, 2018; Zilber et al., 2016). Together, these innovations broaden the financial ecosystem, reduce structural barriers, and contribute to a more inclusive and efficient SME financing landscape.

FinTech-driven access to financial services for SMEs

|

Fintech Theme |

Findings |

Authors |

|

FinTech expands SME access to finance |

FinTech alleviates SMEs’ financing constraints:

- FinTech helps in significantly lowering the cost of capital, enabling SMEs to access funds at more affordable rates. - FinTech improves fund sourcing by enhancing the speed and transparency of funding processes, allowing SMEs to secure capital more efficiently and with greater confidence. - FinTech helps manage leverage by offering tailored financial solutions that align with SMEs' risk profiles and repayment capacities, reducing dependency on traditional high-debt structures. - FinTech facilitates greater access to financial resources, enabling SMEs to allocate assets more strategically. - FinTech mitigates inefficient asset allocation by narrowing financing gaps, especially in firms with high investment potential. - FinTech supports improved investment patterns by relieving funding bottlenecks, allowing SMEs to prioritize operational growth over financial speculation. - FinTech expands credit access to underserved regions and improvs loan performance, counterbalancing the restrictive lending behavior of stable banks. - FinTech streams access to financing, especially for firms with limited collateral or credit history. - Privately-owned, small-sized, and high-growth firms benefit the most from FinTech solutions, as they typically face stricter financing barriers in traditional markets. - Fintech offers a broader and more flexible range of financial services, reducing the rigidity and limitations imposed by conventional lending systems. - Inclusive digital systems fostered by collaborative ecosystems reduce structural barriers to finance.

|

Bani Atta (2025), Jaiswal et al. (2022), Ismanto et al. (2023), Dai et al. (2023), Bu et al. (2024), Chen & Yoon (2022), Feng et al. (2023), Lu et al. (2022), Barkley & Schweitzer (2021), Łasak (2022), and (Yan, 2025). |

|

|

Digital financial literacy reduces financial gaps:

- Digitally literate SMEs can better access credit and integrate into the formal financial system. - The use of social media platforms strengthens the positive relationship between financial literacy and financial inclusion, acting as a moderating factor. - Perceived ease of use and perceived usefulness are key determinants driving SMEs’ adoption of digital financial products. - Fintech alone doesn’t directly improve financial performance, but financial inclusion is boosted by fintech and digital literacy.

|

Rahadian & Thamrin (2023), Kovšca et al. (2024), Naufalin et al. (2024), Moreira-Santos et al. (2022), Mutamimah & Indriastuti (2023), and di Prisco & Strangio (2025). |

|

|

Fintech uses AI-Driven Credit Scoring to asses credit worthiness:

- Machine learning algorithms outperform traditional scoring methods in SME contexts via enabling more precise loan decisions for SMEs with minimal financial history. - AI can analyze alternative data sources (e.g., invoices, sales flows) to assess borrower reliability. - AI scoring expands access by reducing dependency on collateral or lengthy credit histories. - Real-time data processing by AI tools allows dynamic credit risk updates. - Predictive analytics reduce default risks by better segmenting SME borrower profiles. - Continuous model training improves scoring performance as more SME data is collected. - Big Data tools assist in analyzing non-financial SME data for more accurate lending decisions. - AI enhances lender confidence by accurately evaluating SME creditworthiness, especially in data-scarce environments. - Key financial indicators such as EBITDA and cash reserves are effectively leveraged by AI, filling knowledge gaps left by conventional credit assessments. Fintech plays an important role in mitigating the information asymmetries: - Enhanced data analytics and automated tools allow fintech providers to better assess SME creditworthiness. - Real-time financial data reduces the reliance on traditional collateral-based assessments. - Reduced asymmetries lower the risk premium charged to SMEs, improving financing terms. |

Bitetto et al. (2024), Hardik (2024), Rehman et al. (2023), and Malakauskas & Lakstutiene (2021). |

|

|

Fintech plays an important role in mitigating the information asymmetries:

- Enhanced data analytics and automated tools allow fintech providers to better assess SME creditworthiness. - Real-time financial data reduces the reliance on traditional collateral-based assessments. - Reduced asymmetries lower the risk premium charged to SMEs, improving financing terms.

|

|

|

Fintech presents alternative financing business models to SMEs |

The Crowdfunding and Crowdlending:

- Crowdfunding enables direct access to capital and serves as a viable, though small-scale, funding source for tech startups, particularly in the early stages. - Crowdlending introduces innovative funding structures, often combining social capital with digital efficiency to finance growth. - Alternative finance reduces dependence on conventional credit systems, expanding the funding landscape for underserved entrepreneurs. - Transparent loan information (e.g., credit ranking, duration) strongly influences crowdfunding success, validating the role of signaling in reducing information asymmetry. - Crowdfunding fills a critical financing gap for startups offering an inclusive, democratized financing mechanism, particularly suitable for emerging economies with underdeveloped capital markets. - Crowdlending appeals to MSMEs for its lower financial costs and flexible loan conditions compared to traditional financing. - Entrepreneurs show high willingness to adopt crowdlending, indicating growing acceptance of technology-based financial tools. - A well-designed regulatory framework is essential to ensure financial innovation aligns with consumer protection and systemic stability.

|

Kuma et al. (2024), Zilber et al. (2016), Ahmed (2025), Gómez et al. (2022), and Ilenkov (2019). |

|

|

Peer-to-Peer (P2P):

- Scalability of P2P platforms expands financial inclusion, as broader outreach enables more SMEs to access funding. - P2P lending democratizes finance by reducing dependence on traditional intermediaries, thus leveling the playing field for small and informal businesses. - Small firms and micro-companies dominate the participant base, demonstrating the model’s relevance for underserved market segments. - A proposed classification system (English, Dutch, closed auctions) could structure and professionalize P2P platforms, aiding market maturity. - Despite legal and institutional challenges, interest in P2P lending is growing, suggesting a viable alternative financing model for short- to mid-term needs of agro SMEs.

|

Edward et al. (2023), Wang & Liu (2018), Katsamakas & Sánchez-Cartas (2022), and Bondarenko et al. (2017). |

|

|

Initial Coin Offering (ICO) and Blockchain:

- ICOs and Blockchain solutions provide startups with an alternative to traditional financing, enabling greater autonomy and direct access to global investors without relying on banks. - Startups opt for ICOs to retain control, avoid equity dilution, and leverage the decentralized nature of blockchain platforms. - Key factors influencing ICO success include hardcap limits, total token supply, bonus structures, and the size of the founding team, as identified through econometric analysis. - Blockchain infrastructure supports transparency and automation, making ICOs an appealing model for tech-savvy startups in need of flexible and scalable funding. - Credit risk can propagate across the supply chain through blockchain networks, requiring heightened monitoring of interconnected entities. - Blockchain mitigates information asymmetry by providing real-time, immutable records, enhancing lenders' visibility into SME operations and transactions.

|

Xiao et al. (2022), Meriem & Henchiri (2024), and Sochimin (2025). |

|

|

Mobile phones and e-wallets:

- Mobile money usage significantly improves MSMEs’ access to formal credit, increasing the likelihood by 6.05–8.8 percentage points. - Mobile banking and digital wallets help bridge information gaps by creating transaction histories and enhancing traceability of financial behavior. - Mobile banking enables wider access to financial services by overcoming geographic and infrastructural barriers, especially in rural or underserved areas. - Mobile banking supports usage quality by offering convenient, user-friendly platforms that simplify transactions and encourage regular engagement with financial services. |

FinTech-enabled Performance Enhancement for SMEs

FinTech significantly strengthens SMEs by improving access to finance, enhancing profitability, and supporting business sustainability (Alshehadeh & Al-Khawaja, 2022; Candraningrat et al., 2021; Ristati et al., 2024). It boosts resilience through improved financial and digital literacy and promotes innovation by easing funding constraints, especially for tech-driven, agile firms (Frimpong et al., 2022; Ravikumar et al., 2025; Yao & Yang, 2022). Digital tools also enhance operational efficiency, streamline financial management, and reduce costs (Li, 2024). Overall, FinTech is a key enabler of SME growth, resilience, and competitiveness.

FinTech-enabled performance enhancement for SMEs

|

Fintech Theme |

Findings |

Authors |

|

Building Strength and Sustainability |

Fintech drives SMEs' profitability and growth:

- Improved inclusion leads to better profitability indicators such as Return on Assets (ROA), Return on Equity (ROE), and Earnings per Share (EPS). - FinTech facilitates wider access to financial services, especially for marginalized groups and SMEs, enabling business expansion. - FinTech contributes to regional and national economic growth by supporting MSME development. |

Alshehadeh & Al-Khawaja (2022), Meiryani et al. (2021), and Candraningrat et al. (2021), and Verma et al. (2025). |

|

|

Fintech enhances SMEs' business resiliency:

- Financial inclusion and financial decision-making jointly mediate the impact of literacy on resilience. - Financial literacy and digital literacy directly enhance MSMEs’ financial resilience, inclusion, and decision-making quality. - Digital finance and Digital financial literacy jointly influence both financial inclusion and financial resilience FR of micro and small enterprises. - Digital financial inclusion enhances Total Factor Productivity (TFP), improves internal control mechanisms, and reducing agency problems. |

Mediaty et al. (2025), Mishra & Choudhury (2025), Zhang, Dong, et al. (2025), and Ariana et al. (2024). |

|

|

Fintech increases SMEs' sustainability:

- FinTech enhances SME sustainability indirectly by improving financial inclusion, which then supports long-term business viability - Digital financial inclusion promotes high-quality development and sustainability of SMEs by improving access to digital financial services. |

|

|

Driving Innovation and Operational Excellence |

Fintech helps improving Innovation for SMEs:

- Digital finance significantly boosts SME innovation by improving access to funding and enabling experimentation. - Innovation is indirectly supported through: alleviation of financing constraints, enhanced risk tolerance for investments in Research and Development (R&D) and product development, reduction of information asymmetries between SMEs and funders. - The innovation-enhancing effect is stronger for non-state-owned and high-tech enterprises, which are often more agile and better positioned to absorb digital finance tools. - Firm characteristics such as region, ownership structure and technological readiness influence the effectiveness of digital finance in stimulating innovation. - Mobile technologies support innovation, especially in product and marketing development, but have limited impact on process innovation.

|

Yao & Yang (2022), Umar et al. (2025), Ravikumar et al. (2025), Sun & Zhang (2024), Gitonga & Moyi (2019), Elgammal et al. (2023), Wang et al. (2025), Gu et al. (2023), and Zheng & Ye (2024). |

|

|

Digital Financial Literacy drives SMEs' development:

- Financial literacy directly contributes to business success and boosts the performance of SMEs. - FinTech adoption acts as a mediator, linking financial literacy with enhanced SME performance. - Financial inclusion also significantly enhances performance, enabling better access to credit and formal financial systems. - Financial awareness has a stronger impact on sustainability than access to digital finance. - Service providers should enhance usability and increase awareness to promote broader adoption of digital financial tools.

|

Kurniasari & Lestari (2024), Rahayu et al. (2023), Thathsarani & Jianguo (2022), Frimpong et al. (2022), Gunawan et al. (2023), Msomi & Kandolo (2023), Daud et al. (2022), Sari et al. (2023), Rahadjeng et al. (2023), and (Mohamed & Otake, 2025). |

|

|

Fintech enhances SMEs' efficiency:

- Mobile payments streamline daily transactions, leading to more efficient financial management. - Digital payment systems contribute to refining overall financial management approaches in SMEs. - Digital transformation contributes to improved financial results by streamlining operations, enhancing productivity, and reducing inefficiencies. - Cost efficiency is a central mechanism, achieved through a combination of low-cost financing strategies and digitized operations. - Digital finance significantly improves SME development quality, particularly by optimizing financial processes and service delivery, as well as reducing processing time. - Digital finance improves financial resource allocation efficiency, ensuring funds are better directed toward productive and growth-oriented SMEs. |

Zhang, Mi, et al. (2025), Suryanto et al. (2020), Sanga & Aziakpono (2024), Li (2024), Rita & Nastiti (2024), and Xie & Liu (2022). |

Research Gaps and Recommendations for Future Research Endeavors

The 71 empirical studies reviewed reveal several challenges that limit FinTech's full potential for supporting SME development, particularly in developing and emerging economies. We summarize these key research gaps and propose corresponding future research directions below, addressing research question 3.

Research Challenges

Out of the 71 empirical studies reviewed, only 6 employed qualitative methods to examine the role of FinTech in SME development. The overwhelming dominance of quantitative approaches limits understanding of the behavioral, institutional, and cultural factors that influence adoption and outcomes. As a result, the findings often miss the complex decision-making processes and lived experiences of SMEs interacting with digital finance systems.

Surveys were the main data source in 38 out of 71 studies, while fewer than 25 leveraged transactional or platform-level datasets (e.g., ICO data, lending logs, blockchain records). This results in a disconnect between reported perceptions and actual financial behavior, reducing the validity of some findings.

Most studies are region-specific or platform-specific, such as those focusing solely on China, Indonesia, or select African economies. Only 12 of 71 studies analyzed FinTech and SMEs using country-level or multi-country comparative data, limiting the generalizability of the results. Sector-wise, studies often overlook agriculture, informal trade, and rural enterprises where FinTech could have a high impact.

Out of the 71 studies, only 10 adopted clear theoretical models such as the Technology Acceptance Model, Resource-Based View, or Institutional Theory. The absence of theoretical anchoring weakens explanatory power and the contribution to the broader FinTech and SME literature.

Future Research Suggestion

Future studies should incorporate qualitative or mixed-methods approaches to capture SME behavior, perceptions, and resistance to FinTech adoption. In-depth interviews, case studies, and ethnographic methods can enrich understanding beyond statistical correlations.

Research should focus on integrating digital trace data, Application Programming Interface (API)-based records, and blockchain transaction logs to evaluate the real impact of FinTech tools. Collaboration with platforms and regulators can enable access to such granular datasets.

Future research should expand geographical and sectoral coverage, particularly across underserved regions such as North Africa, Central Asia, and the Middle East. Cross-country analyses can offer comparative insights and inform the design of context-specific digital finance policies.

Studies should embed analyses within established or emerging theoretical frameworks to strengthen causal explanations. Theory-driven research can also support policy formulation and comparative evaluations across contexts.

Conclusion

This systematic literature review examined how FinTech has contributed to improving MSME financial inclusion and development in emerging and developing economies between 2008 and 2025. The review followed the PRISMA and PSALSAR frameworks to ensure transparency, replicability, and rigor throughout the review process. A total of 1,931 peer-reviewed studies were initially identified through Scopus and WOS, but only 71 empirical studies were selected for full analysis after screening.

The findings confirm that FinTech plays a pivotal role in addressing SME financing constraints through alternative financing channels (such as P2P lending, crowdfunding, mobile money, and blockchain-based finance), enhanced credit assessment methods (notably AI-driven credit scoring), and improved financial infrastructure. These innovations have led to better access to funding, improved firm performance, and increased business resilience and sustainability.

Nevertheless, the review highlights several research challenges, including geographic and methodological concentration, overreliance on secondary and cross-sectional data, limited cross-country studies, and under-exploration of sectoral and regulatory heterogeneity. These gaps constrain the generalizability and scalability of current findings.

Future research should broaden the geographical scope, prioritize firm-level and longitudinal analyses, and explore the interactions among FinTech, regulatory environments, and SME characteristics. Furthermore, more attention is needed on how FinTech ecosystems can support underserved MSMEs in fragile and low-income contexts. Strengthening this research agenda will be crucial for maximizing FinTech’s role in driving inclusive and sustainable financial systems globally.

Funding

This research received no external funding.

Author Contributions

Conceptualization, S.H.K. and N.S.; methodology, S.H.K. and N.S.; software, N.S; validation, S.H.K; formal analysis, S.H.K. and N.S.; investigation, S.H.K. and N.S.; resources, S.H.K. and N.S.; data curation, S.H.K. and N.S.; writing, original draft preparation, N.S; writing, review and editing, S.H.K; visualization, N.S; supervision, S.H.K; project administration, S.H.K.

Conflict of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Generative AI Use Disclosure Statement

No generative AI tools were used in the writing or analysis of this manuscript.

Data Availability Statement

No new data were created or analyzed in this study.

Acknowledgments

Not applicable.

References

Afjal, M. (2023). Bridging the financial divide: a bibliometric analysis on the role of digital financial services within FinTech in enhancing financial inclusion and economic development. Humanities and Social Sciences Communications, 10(1), 1–27. https://doi.org/10.1057/S41599-023-02086-Y

Ahmed, H. (2025). Crowdfunding and entrepreneurial/SME finance: regulatory framework for financial inclusion. Journal of Banking Regulation. https://doi.org/10.1057/S41261-025-00273-2

Al-Hakim, M. S., Al-Hamad, A. A.-S., & Ghaith, M. A. (2021). The role of financial inclusion in bridging SMEs financing gap the viewpoint of credit employees at Jordanian Islamic Banks. Islamic Quarterly, 65(3), 355–380. https://www.scopus.com/pages/publications/85136148439?inward

Alhalwachi, L., Bukhowa, B., Danish, F., Alkhater, N., Zainaldeen, Z., Eshaq, M., & Aldhamin, M. (2025). The development of FinTech ecosystems in emerging markets: A study on mobile money and financial inclusion in the Kingdom of Bahrain. Studies in Systems, Decision and Control, 568, 227–237. https://doi.org/10.1007/978-3-031-71526-6_20

Alshehadeh, A. R., & Al-Khawaja, H. A. (2022). Financial technology as a basis for financial inclusion and its impact on profitability: Evidence from commercial banks. International Journal of Advances in Soft Computing and Its Applications, 14(2), 125–138. https://doi.org/10.15849/IJASCA.220720.09

Aria, M., & Cuccurullo, C. (2017). bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of Informetrics. https://doi.org/10.1016/j.joi.2017.08.007

Ariana, I. M., Wiksuana, I. G. B., Candraningrat, I. R., & Baskara, I. G. K. (2024). The effects of financial literacy and digital literacy on financial resilience: Serial mediation roles of financial inclusion and financial decisions. Uncertain Supply Chain Management, 12(2), 999–1014. https://doi.org/10.5267/J.USCM.2023.12.008

Arner, D. W., Barberis, J., Buckley, R. P., Arner, D., & Barberis, J. (2017). FinTech, RegTech and the reconceptualization of financial regulation. Northwestern Journal of International Law & Business, 37(3), 371. http://hub.hku.hk/handle/10722/235796

Bani Atta, A. A. (2025). Financial technology platforms and enhancing SME financing in Jordan. Discover Sustainability, 6(1). https://doi.org/10.1007/s43621-025-01345-z

Barkley, B., & Schweitzer, M. (2021). The rise of fintech lending to small businesses: Businesses’ perspectives on borrowing∗. International Journal of Central Banking, 17(1), 35–65. https://www.scopus.com/pages/publications/85102683758?inward

Barroso, M., & Laborda, J. (2022). Digital transformation and the emergence of the Fintech sector: Systematic literature review. Digital Business, 2(2), 100028. https://doi.org/10.1016/J.DIGBUS.2022.100028

Beck, T., & Demirguc-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. Journal of Banking & Finance, 30(11), 2931–2943. https://doi.org/10.1016/J.JBANKFIN.2006.05.009

Bitetto, A., Cerchiello, P., Filomeni, S., Tanda, A., & Tarantino, B. (2024). Can we trust machine learning to predict the credit risk of small businesses? Review of Quantitative Finance and Accounting, 63(3), 925–954. https://doi.org/10.1007/S11156-024-01278-0

Bondarenko, N. E., Maksimova, T. P., & Zhdanova, O. A. (2017). Peer-to-peer lending as a mechanism for attracting financial resources into smaller forms of business within the system of Russia’s agro-industrial complex. Espacios, 38(62). https://www.scopus.com/pages/publications/85040625335?inward

Bu, Y., Du, X., Wang, Y., Liu, S., Tang, M., & Li, H. (2024). Digital inclusive finance: A lever for SME financing? International Review of Financial Analysis, 93. https://doi.org/10.1016/J.IRFA.2024.103115

Candraningrat, I. R., Abundanti, N., Mujiati, N. W., Erlangga, R., & Jhuniantara, I. M. G. (2021). The role of financial technology on development of MSMEs. Accounting, 7(1), 225–230. https://doi.org/10.5267/J.AC.2020.9.014

Chen, H., & Yoon, S. S. (2022). Does technology innovation in finance alleviate financing constraints and reduce debt-financing costs? Evidence from China. Asia Pacific Business Review, 28(4), 467–492. https://doi.org/10.1080/13602381.2021.1874665

Dai, D., Fu, M., Ye, L., & Shao, W. (2023). Can digital inclusive finance help small- and medium-sized enterprises deleverage in China? Sustainability (Switzerland), 15(8). https://doi.org/10.3390/SU15086625

Daud, I., Nurjannah, D., Mohyi, A., Ambarwati, T., Cahyono, Y., Haryoko, A. D. E., Handoko, A. L., Putra, R. S., Wijoyo, H., Ari-Yanto, A., & Jihadi, M. (2022). The effect of digital marketing, digital finance and digital payment on finance performance of indonesian smes. International Journal of Data and Network Science, 6(1), 37–44. https://doi.org/10.5267/J.IJDNS.2021.10.006

di Prisco, D., & Strangio, D. (2025). Technology and financial inclusion: a case study to evaluate potential and limitations of Blockchain in emerging countries. Technology Analysis and Strategic Management, 37(4), 448–461. https://doi.org/10.1080/09537325.2021.1944617

Edward, M. Y., Fuad, E. N., Ismanto, H., Atahau, A. D. R., & Robiyanto. (2023). Success factors for peer-to-peer lending for SMEs: Evidence from Indonesia. Investment Management and Financial Innovations, 20(2), 16–25. https://doi.org/10.21511/IMFI.20(2).2023.02

Elgammal, M. M., Al Bakri, A. A., & AlJanahi, A. D. Y. (2023). The effect of new and traditional sources of financing on the performance of small and entrepreneurship businesses: The case of Qatar. Cogent Economics and Finance, 11(2). https://doi.org/10.1080/23322039.2023.2183667

Feng, Y., Meng, M., & Li, G. (2023). Impact of digital finance on the asset allocation of small- and medium-sized enterprises in China: Mediating role of financing constraints. Journal of Innovation and Knowledge, 8(3). https://doi.org/10.1016/J.JIK.2023.100405

Firmansyah, E. A., Masri, M., Anshari, M., Hairul, M., & Besar, A. (2022). Factors affecting Fintech adoption: A systematic literature review. FinTech 2023, 2(1), 21–33. https://doi.org/10.3390/FINTECH2010002

Frimpong, S. E., Agyapong, G., & Agyapong, D. (2022). Financial literacy, access to digital finance and performance of SMEs: Evidence From Central region of Ghana. Cogent Economics and Finance, 10(1). https://doi.org/10.1080/23322039.2022.2121356

Gitonga, A., & Moyi, E. (2019). Mobile technology as an enabler of innovation in Kenya’s Micro, small and medium establishments. 2019 IST-Africa Week Conference, IST-Africa 2019. https://doi.org/10.23919/ISTAFRICA.2019.8764844

Gomber, P., Koch, J. A., & Siering, M. (2017). Digital Finance and FinTech: current research and future research directions. Journal of Business Economics, 87(5), 537–580. https://doi.org/10.1007/S11573-017-0852-X/METRICS

Gómez, G., Barranzuela, J. A. N., & Ojeda, L. M. M. (2022). Crowdlending as a financing alternative for MSMEs in Peru. Retos, 12(23), 161–177. https://doi.org/10.17163/RET.N23.2022.10

Gu, F., Gao, J., Zhu, X., & Ye, J. (2023). The impact of digital inclusive finance on SMEs’ technological innovation activities—Empirical analysis based on the data of new third board enterprises. PLoS ONE, 18(11 NOVEMBER). https://doi.org/10.1371/JOURNAL.PONE.0293500

Gunawan, A., Jufrizen, & Pulungan, D. R. (2023). Improving MSME performance through financial literacy, financial technology, and financial inclusion. International Journal of Applied Economics, Finance and Accounting, 15(1), 39–52. https://doi.org/10.33094/IJAEFA.V15I1.761

Ha, D., Le, P., & Nguyen, D. K. (2025). Financial inclusion and fintech: a state-of-the-art systematic literature review. Financial Innovation, 11(1), 1–42. https://doi.org/10.1186/S40854-024-00741-0

Hardik, N. (2024). Digitalisation promotes adoption of soft information in SME credit evaluation: the case of Indian banks. Digital Finance, 6(1), 23–54. https://doi.org/10.1007/S42521-023-00078-W

Ilenkov, D. (2019). Technology crowdfunding in Russia: Alternative finance for start-ups. International Journal of Economics and Business Administration, 7(2), 3–11. https://doi.org/10.35808/IJEBA/210

Ismail, M. Z., Ramly, Z. M., & Hamid, R. A. (2021). Systematic review of cost overrun research in the developed and developing countries. International Journal of Sustainable Construction Engineering and Technology, 12(1), 196–211. https://doi.org/10.30880/IJSCET.2021.12.01.020

Ismanto, H., Wibowo, P. A., & Shofwatin, T. D. (2023). Bank stability and fintech impact on MSMEs’ credit performance and credit accessibility. Banks and Bank Systems, 18(4), 105–115. https://doi.org/10.21511/BBS.18(4).2023.10

Jain, R., Kumar, S., Sood, K., Grima, S., & Rupeika-Apoga, R. (2023). A systematic literature review of the risk landscape in Fintech. Risks, 11(2), 36. https://doi.org/10.3390/RISKS11020036

Jaiswal, R., Seth, V., & Kasera, M. (2022). Digital banking innovations improving financial access for agribusiness sector in emerging economies. ECS Transactions, 107(1), 11755–11764. https://doi.org/10.1149/10701.11755ECST

Katsamakas, E., & Sánchez-Cartas, J. M. (2022). Network formation and financial inclusion in P2P lending: A computational model. Systems, 10(5). https://doi.org/10.3390/SYSTEMS10050155

Kaur, G., Singh, M., & Singh, S. (2021). Mapping the literature on financial well-being: A systematic literature review and bibliometric analysis. International Social Science Journal, 71(241–242), 217–241. https://doi.org/10.1111/ISSJ.12278

Kovšca, V., Vincek, Z. L., & Murić, D. (2024). Contemporary forms of financing for small and medium-sized enterprise: Country case study of Croatia. TEM Journal, 13(1), 818–829. https://doi.org/10.18421/TEM131-84

Kuma, F. K., Yusoff, M. E., Ameyaw, F., & Jayamana, J. (2024). A critical review of peer-to-peer crowdfunding model as alternate finance for start-ups. International Journal of Business, 29(2), 1–14. https://doi.org/10.55802/IJB.029(2).001

Kurniasari, F., & Lestari, E. D. (2024). Development of financial literacy and fintech adoption on women smes business performance in Indonesia. Eastern-European Journal of Enterprise Technologies, 5(13(131)), 67–75. https://doi.org/10.15587/1729-4061.2024.312613

Łasak, P. (2022). The role of financial technology and entrepreneurial finance practices in funding small and medium-sized enterprises. Journal of Entrepreneurship, Management and Innovation, 18(1), 7–34. https://doi.org/10.7341/20221811

Lee, D. K. C., & Teo, E. G. S. (2015). Emergence of Fintech and the basic principles. SSRN Electronic Journal. https://doi.org/10.2139/SSRN.2668049

Lee, I., & Shin, Y. J. (2018). Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, 61(1), 35–46. https://doi.org/10.1016/J.BUSHOR.2017.09.003

Li, Q. (2024). The impact of mobile payments on the financial management efficiency of small and medium-sized enterprises. International Journal of Interactive Mobile Technologies, 18(21), 171–184. https://doi.org/10.3991/IJIM.V18I21.52245

Lu, Z., Wu, J., Li, H., & Nguyen, D. K. (2022). Local bank, digital financial inclusion and SME financing constraints: Empirical evidence from China. Emerging Markets Finance and Trade, 58(6), 1712–1725. https://doi.org/10.1080/1540496X.2021.1923477

Malakauskas, A., & Lakstutiene, A. (2021). The application of artificial intelligence tools in creditworthiness modelling for SME entities [Paper presentation]. 2021 IEEE International Conference on Technology and Entrepreneurship, ICTE 2021. https://doi.org/10.1109/ICTE51655.2021.9584528

Mdoe, I. J., & Kinyanjui, G. K. (2018). Mobile telephony, social networks and credit access: Evidence from MSMEs in Kenya. Cogent Economics and Finance, 6(1). https://doi.org/10.1080/23322039.2018.1459339

Mediaty, Maryanti, Arifin, A. H., Mas’ud, A. A., & Dinar. (2025). Enhancing digital financial inclusion: Adoption factors of digital accounting among MSMEs in Indonesia. International Journal of Innovative Research and Scientific Studies, 8(3), 1423–1434. https://doi.org/10.53894/IJIRSS.V8I3.6818

Meiryani, M., Hanna Uli Pakpahan, N., Wahyuningtias, D., Mad Daud, Z., & Liawatimena, S. (2021). The role of financial technology for development of micro, small and medium enterprises (Msmes) in Indonesia. ACM International Conference Proceeding Series, 60–65. https://doi.org/10.1145/3507509.3507518

Mengist, W., Soromessa, T., & Legese, G. (2020). Method for conducting systematic literature review and meta-analysis for environmental science research. MethodsX, 7, 100777. https://doi.org/10.1016/J.MEX.2019.100777

Meriem, L., & Henchiri, J. E. (2024). The success factors of initial coin offerings in startup financing. Decentralized Finance and Tokenization in FinTech, 271–284. https://doi.org/10.4018/979-8-3693-3346-4.CH015

Mishra, A. S., & Choudhury, S. (2025). Enhancing financial inclusion and business growth of micro-enterprises in rural India: assessing the moderating role of bank support. Journal of Human Behavior in the Social Environment. https://doi.org/10.1080/10911359.2025.2503439

Mohamed, H. A., & Otake, T. (2025). The role of Islamic FinTech in digital financial inclusion and sustainable development post covid-19: cross-country analysis. International Journal of Islamic and Middle Eastern Finance and Management, 18(3), 649–671. https://doi.org/10.1108/IMEFM-02-2024-0100

Moreira-Santos, D., Au-Yong-Oliveira, M., & Palma-Moreira, A. (2022). Fintech services and the drivers of their implementation in small and medium enterprises. Information (Switzerland), 13(9). https://doi.org/10.3390/INFO13090409

Msomi, T. S., & Kandolo, K. M. (2023). Sustaining small and medium-sized enterprises through financial awareness, access to digital finance in South Africa. Investment Management and Financial Innovations, 20(1), 317–327. https://doi.org/10.21511/IMFI.20(1).2023.27

Mutamimah, M., & Indriastuti, M. (2023). Fintech, financial literacy, and financial inclusion in Indonesian SMEs. International Journal of Entrepreneurship and Innovation Management, 27(1–2), 137–150. https://doi.org/10.1504/IJEIM.2023.129331

Naufalin, L. R., Krisnarisanti, A., Dinanti, A., & Anggraeni, A. I. (2024). Factors affecting the digital financial product adoption on Batik SMEs. Quality - Access to Success, 25(199), 10–18. https://doi.org/10.47750/QAS/25.199.02

Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., Chou, R., Glanville, J., Grimshaw, J. M., Hróbjartsson, A., Lalu, M. M., Li, T., Loder, E. W., Mayo-Wilson, E., McDonald, S., … Moher, D. (2021). The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. The BMJ, 372. https://doi.org/10.1136/BMJ.N71

R Core Team. (2024). R: A Language and Environment for Statistical Computing. https://www.R-project.org/

Rahadian, A., & Thamrin, H. (2023). Analysis of factors affecting MSME in using Fintech lending as alternative financing: Technology acceptance model approach. Brazilian Business Review, 20(3), 301–322. https://doi.org/10.15728/BBR.2023.20.3.4.EN

Rahadjeng, E. R., Pratikto, H., Mukhlis, I., Restuningdiah, N., & Mala, I. K. (2023). The impact of financial literacy, financial technology, and financial inclusion on SME business performance in Malang Raya, Indonesia. Journal of Social Economics Research, 10(4), 146–160. https://doi.org/10.18488/35.V10I4.3509

Rahayu, S. K., Budiarti, I., Firdaus, D. W., & Onegina, V. (2023). Digitalization and informal MSME: Digital financial inclusion for MSME development in the formal economy. Journal of Eastern European and Central Asian Research, 10(1), 9–19. https://doi.org/10.15549/JEECAR.V10I1.1056

Ravikumar, T., Raghunandan, G., Benedict, J., & Krishna, T. A. (2025). Digital financial inclusion and financial resilience of micro and small entrepreneurs in Post-COVID-19 in Karnataka. Finance India, 39(1), 129–146. https://www.scopus.com/pages/publications/105005992254?inward

Rehman, S. U., Al-Shaikh, M., Washington, P. B., Lee, E., Song, Z., Abu-AlSondos, I. A., Shehadeh, M., & Allahham, M. (2023). FinTech adoption in SMEs and bank credit supplies: A study on manufacturing SMEs. Economies, 11(8). https://doi.org/10.3390/ECONOMIES11080213

Ristati, Zulham, & Akhyar, C. (2024). The effect of financial technology and financial literacy on the sustainability of MSMEs in Lhokseumawe city with financial inclusion as a mediating variable. Journal of Ecohumanism, 3(8), 2969–2978. https://doi.org/10.62754/JOE.V3I8.4940

Rita, M. R., & Nastiti, P. K. Y. (2024). The influence of financial bootstrapping and digital transformation on financial performance: evidence from MSMEs in the culinary sector in Indonesia. Cogent Business and Management, 11(1). https://doi.org/10.1080/23311975.2024.2363415

Sanga, B., & Aziakpono, M. (2023). FinTech and SMEs financing: A systematic literature review and bibliometric analysis. Digital Business, 3(2), 100067. https://doi.org/10.1016/J.DIGBUS.2023.100067

Sanga, B., & Aziakpono, M. (2024). FinTech developments and their heterogeneous effect on digital finance for SMEs and entrepreneurship: evidence from 47 African countries. Journal of Entrepreneurship in Emerging Economies, 17(7), 127–155. https://doi.org/10.1108/JEEE-09-2023-0379

Sari, Y. W., Nugroho, M., & Rahmiyati, N. (2023). The effect of financial knowledge, financial behavior and digital financial capabilities on financial inclusion, financial concern and performance in MSMEs in East Java. Uncertain Supply Chain Management, 11(4), 1745–1758. https://doi.org/10.5267/J.USCM.2023.6.016

Singh, V. K., Singh, P., Karmakar, M., Leta, J., & Mayr, P. (2021). The journal coverage of Web of Science, Scopus and Dimensions: A comparative analysis. Scientometrics, 126(6), 5113–5142. https://doi.org/10.1007/S11192-021-03948-5/METRICS

Sochimin. (2025). The role of financial technology as a catalyst for financial literacy intentions and financial inclusion in Micro, Small and Medium Enterprises (MSMEs) in central Java. Quality - Access to Success, 26(205), 107–114. https://doi.org/10.47750/QAS/26.205.11

Sun, J., & Zhang, J. (2024). Digital financial inclusion and innovation of MSMEs. Sustainability (Switzerland), 16(4). https://doi.org/10.3390/SU16041404

Sun, R., Shang, Q., Zu, A., & Gan, S. (2025). How does digital finance affect financing constraints of SMEs? Evidence from China. Applied Economics. https://doi.org/10.1080/00036846.2025.2453248

Suryanto, S., Rusdin, R., & Dai, R. M. (2020). Fintech as a catalyst for growth of micro, small and medium enterprises in Indonesia. Academy of Strategic Management Journal, 19(5), 1–12. https://www.scopus.com/pages/publications/85098198612?inward

Suryono, R. R., Budi, I., & Purwandari, B. (2020). Challenges and trends of financial technology (Fintech): A systematic literature review. Information, 11(12), 590. https://doi.org/10.3390/INFO11120590

Tello-Gamarra, J., Campos-Teixeira, D., Longaray, A. A., Reis, J., & Hernani-Merino, M. (2022). Fintechs and institutions: A systematic literature review and future research agenda. Journal of Theoretical and Applied Electronic Commerce Research, 17(2), 722–750. https://doi.org/10.3390/JTAER17020038

Thathsarani, U. S., & Jianguo, W. (2022). Do digital finance and the technology acceptance model strengthen financial inclusion and SME performance? Information (Switzerland), 13(8). https://doi.org/10.3390/INFO13080390

Tranfield, D., Denyer, D., & Smart, P. (2003). Towards a methodology for developing evidence-informed management knowledge by means of systematic review. British Journal of Management, 14(3), 207–222. https://doi.org/10.1111/1467-8551.00375

Umar, U. H., Baita, A. J., Hamadou, I., & Abduh, M. (2025). Digital finance and SME financial inclusion in Africa. African Journal of Economic and Management Studies, 16(1), 18–33. https://doi.org/10.1108/AJEMS-08-2023-0323

Verma, A., Das, K. C., & Misra, P. (2025). Digital finance and MSME performance in India: evidence from World Bank Enterprise Survey data. Journal of Economic Studies, 52(5), 887–903. https://doi.org/10.1108/JES-12-2023-0744

Wang, J., Yao, Y., Ge, H., & Wang, J. (2025). The impact of digital inclusive finance on SME innovation. Sustainability (Switzerland), 17(8). https://doi.org/10.3390/SU17083633

Wang, L., & Liu, H. (2018). Financing of small and medium enterprises based on internet finance. IOP Conference Series: Materials Science and Engineering, 394(5). https://doi.org/10.1088/1757-899X/394/5/052015

Xiao, P., Salleh, M. I. bin, & Cheng, J. (2022). Research on factors affecting SMEs’ credit risk based on blockchain-driven supply chain finance. Information (Switzerland), 13(10). https://doi.org/10.3390/INFO13100455

Xiao, Y., & Watson, M. (2019). Guidance on conducting a systematic literature review. Journal of Planning Education and Research, 39(1), 93–112. https://doi.org/10.1177/0739456X17723971

Xie, C., & Liu, C. (2022). The nexus between digital finance and high-quality development of SMEs: evidence from China. Sustainability (Switzerland), 14(12). https://doi.org/10.3390/SU14127410

Yan, J. (2025). How the use of alternative information in risk management fintech platforms influences SME lending: a qualitative case study. Qualitative Research in Financial Markets, 17(1), 1–20. https://doi.org/10.1108/QRFM-08-2023-0198

Yao, L., & Yang, X. (2022). Can digital finance boost SME innovation by easing financing constraints?: Evidence from Chinese GEM-listed companies. PLoS ONE, 17(3 March). https://doi.org/10.1371/JOURNAL.PONE.0264647

Yu, Y., Junjan, V., Yazan, D. M., & Iacob, M. E. (2022). A systematic literature review on Circular Economy implementation in the construction industry: a policy-making perspective. Resources, Conservation and Recycling, 183, 106359. https://doi.org/10.1016/J.RESCONREC.2022.106359

Zhang, Y., Dong, X., Wang, Y., & Li, H. (2025). Research on the theoretical logic and mechanism of digital inclusive finance in promoting the high-quality development of small and medium-sized enterprises. International Review of Economics and Finance, 101. https://doi.org/10.1016/J.IREF.2025.104202

Zhang, Y., Jin, X., & Li, H. (2025). The impact of digital financial inclusion on the high-quality development of small- and medium-sized enterprises—Evidence from China. International Review of Financial Analysis, 102, 104074. https://doi.org/10.1016/J.IRFA.2025.104074

Zhang, Y., Mi, X., Li, H., & Wang, X. (2025). Evolutionary game analysis of digital inclusive finance for high-quality development of small and medium-sized enterprises. International Review of Financial Analysis, 105. https://doi.org/10.1016/J.IRFA.2025.104388

Zheng, W., & Ye, Z. (2024). The incentive effect of digital finance on innovation of small- and medium-sized enterprises considering heterogeneity: An empirical study based on Chinese-listed firms. Sustainability (Switzerland), 16(19). https://doi.org/10.3390/SU16198533

Zhu, J., & Liu, W. (2020). A tale of two databases: The use of Web of Science and Scopus in academic papers. Scientometrics, 123(1), 321–335. https://doi.org/10.1007/s11192-020-03387-8

Zilber, S. N., Silveira, F., de Carvalho, L. F., & Imbrizi, abricio G. (2016). Crowd funding as an alternative for new ventures funding in emerging countries. International Business Management, 10(4), 575–584. https://doi.org/10.3923/IBM.2016.575.584

Page 1 of

Download Count : -

Visit Count : 5

Keywords

Fintech; Financial Inclusion; Small and Medium-sized Enterprises; Systematic Literature Review; Bibliometric Analysis

Author(s) Information

How to cite this article

Khlifa, S. H., & Srifi, N. (2026). Fintech and SME financial inclusion: A systematic literature review and bibliometric analysis. European Journal of Studies in Management and Business, 37, 1-22. https://doi.org/10.32038/mbrq.2026.37.01

Funding

This research received no external funding.

Author Contributions

Conceptualization, S.H.K. and N.S.; methodology, S.H.K. and N.S.; software, N.S; validation, S.H.K; formal analysis, S.H.K. and N.S.; investigation, S.H.K. and N.S.; resources, S.H.K. and N.S.; data curation, S.H.K. and N.S.; writing, original draft preparation, N.S; writing, review and editing, S.H.K; visualization, N.S; supervision, S.H.K; project administration, S.H.K.

Conflict of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Generative AI Use Disclosure Statement

No generative AI tools were used in the writing or analysis of this manuscript.

Data Availability Statement

No new data were created or analyzed in this study.

Acknowledgments

Not applicable.

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/