Original Research

The Impact of Related Party Transactions on Audit Fees: Evidence from Companies Listed on the Tehran Stock Exchange

- Abstract

- Full text

- Metrics

This study examines the relationship between Related Party Transactions (RPTs) and audit fees in 163 companies listed on the Tehran Stock Exchange over 2014–2024. Despite extensive literature suggesting that RPTs increase audit risk and may affect audit pricing, our findings indicate that in the Iranian context, RPTs do not exert a statistically significant influence on audit fees. Using a panel multivariate regression model controlling for firm- and auditor-specific characteristics, the analysis reveals that other financial and audit attributes such as client importance, firm size, leverage, and auditor characteristics play a more decisive role in determining audit fees. These results diverge from some international evidence and highlight the distinctive institutional environment in Iran, characterized by concentrated ownership, government influence, limited audit market competition, and relatively weak corporate governance mechanisms. The study underscores that audit fees in Iran appear to primarily reflect auditors’ efforts to maintain general audit quality rather than respond to the presence or volume of related party transactions. Implications for policy and practice include the need to strengthen governance mechanisms, improve transparency in financial reporting, and assess how institutional context moderates the interplay between RPTs and audit processes.

The Impact of Related Party Transactions on Audit Fees: Evidence from Companies Listed on the Tehran Stock Exchange

Saeed Alipour

Department of Accounting, Ard.C., Islamic Azad University, Ardabil, Iran

ABSTRACT:

This study examines the relationship between Related Party Transactions (RPTs) and audit fees in 163 companies listed on the Tehran Stock Exchange over 2014–2024. Despite extensive literature suggesting that RPTs increase audit risk and may affect audit pricing, our findings indicate that in the Iranian context, RPTs do not exert a statistically significant influence on audit fees. Using a panel multivariate regression model controlling for firm- and auditor-specific characteristics, the analysis reveals that other financial and audit attributes such as client importance, firm size, leverage, and auditor characteristics play a more decisive role in determining audit fees. These results diverge from some international evidence and highlight the distinctive institutional environment in Iran, characterized by concentrated ownership, government influence, limited audit market competition, and relatively weak corporate governance mechanisms. The study underscores that audit fees in Iran appear to primarily reflect auditors’ efforts to maintain general audit quality rather than respond to the presence or volume of related party transactions. Implications for policy and practice include the need to strengthen governance mechanisms, improve transparency in financial reporting, and assess how institutional context moderates the interplay between RPTs and audit processes.

KEYWORDS: Related Party Transactions, Audit Fees, Audit Quality, Corporate Governance, Tehran Stock Exchange

Introduction

Related Party Transactions (RPTs) are common in many firms’ daily operations, occurring when a company conducts business with affiliates, major shareholders, executives, or other connected parties. While such transactions can facilitate operational efficiency and trust-based networks, they introduce unique risks to financial reporting and auditing due to the lack of independence between involved entities. Improper identification, measurement, or disclosure of RPTs can elevate the risk of material misstatement in financial statements, which is why accounting standards such as ISA 550 mandate specific requirements for recognizing and reporting related party relationships, transactions, and balances.

High-profile corporate scandals, including Enron, WorldCom, Parmalat, and Bankia, have illustrated how RPTs can be misused to transfer benefits to insiders, obscure economic reality, and manipulate reported earnings (Darabi & Davoudkhani, 2015; Elistratova et al., 2023). These cases highlight the dual nature of RPTs: they may serve legitimate business purposes but also present opportunities for managerial opportunism when governance and disclosure are weak. Empirical studies suggest that RPTs often increase audit risk and can influence audit fees. Heightened RPT activity typically requires additional audit procedures to verify financial information, leading to higher audit costs (Kushwaha et al., 2022; Rasheed & Havalder, 2021). However, in environments with concentrated ownership or weak investor protection, audit fees may also reflect client negotiation power rather than pure risk considerations (Elistratova et al., 2023).

Recent evidence from emerging markets deepens our understanding of the mechanisms linking RPTs and audit costs. Zhu and Zhao (2023) show that RPTs exacerbate operational risk in manufacturing firms, which mediates the effect of RPTs on audit fees. This effect is particularly pronounced in non-state-owned enterprises, indicating that ownership structure moderates the relationship between RPTs and audit pricing. Xu and Zhang (2025) find that RPTs increase information asymmetry, worsening the corporate information environment and raising audit fees, especially in firms with weaker internal controls. Together, these studies suggest that RPTs affect audit costs through multiple channels, including operational risk and information asymmetry.

In Iran, concentrated ownership, significant government involvement, and distinctive corporate governance structures may further influence how RPTs affect audit fees. Domestic evidence indicates that RPTs can lead to unexpected increases in audit fees and delays in reporting (Khatiri et al., 2022; Salehi et al., 2020). Nevertheless, few studies systematically examine the mechanisms by which RPTs impact audit fees in Iran, leaving a clear gap in the literature. Investigating this relationship can provide insights for auditors, regulators, and managers, supporting better audit planning, fee-setting, and corporate governance practices.

Literature Review

Research on Related Party Transactions (RPTs) has shown that these transactions, while often legitimate, can significantly influence audit processes and fees due to their potential to increase financial reporting complexity. Historical evidence from corporate scandals including Enron, WorldCom, Parmalat, and Bankia demonstrates that RPTs can serve as mechanisms for managerial opportunism, concealing economic reality and benefiting controlling parties (Elistratova et al., 2023). Regulatory bodies, such as the Financial Accounting Standards Board and the International Auditing and Assurance Standards Board, have emphasized that inadequate disclosure of RPTs can undermine market confidence and distort capital allocation (Cheng et al., 2024; Ding et al., 2024).

Early empirical research provided mixed results regarding the relationship between RPTs and audit fees (Apostolou et al., 2001; Beasley et al., 2001; Bell & Carcello, 2000; Gordon et al., 2007; Louwers et al., 2008; Moyes et al., 2005; Wilks & Zimbelman, 2005). Some studies reported a positive association between RPTs and audit fees due to increased audit risk, whereas others suggested that institutional characteristics, such as ownership concentration, might weaken this relationship (Elistratova et al., 2023). More recent studies in emerging markets have clarified the mechanisms underlying this association.

Zhu and Zhao (2023) provide evidence from Chinese manufacturing firms, showing that RPTs exacerbate operational risk, which in turn increases audit fees. Their analysis highlights that non-state-owned enterprises experience a stronger effect, suggesting that ownership structure moderates the impact of RPTs on audit costs. Similarly, Xu and Zhang (2025) demonstrate that frequent RPTs increase information asymmetry, worsening both internal and external information environments, and leading to higher audit fees. The effect is more pronounced in firms with weaker internal controls, illustrating that governance quality also moderates the relationship. Together, these findings suggest that audit fees are sensitive to both the level of RPTs and the firm-specific risk and control characteristics.

Domestic evidence from Iran further reinforces these observations. Concentrated ownership, government involvement, and unique corporate governance structures may amplify the effect of RPTs on audit fees. Studies show that RPTs can lead to unexpected increases in audit fees and delays in reporting, indicating that auditors adjust fees to account for the additional risk (Khatiri et al., 2022; Salehi et al., 2020). However, systematic examinations of the underlying mechanisms, particularly operational risk and information asymmetry, are limited in Iran, representing a clear gap in the literature.

Considering the combined evidence from global and domestic studies, it is expected that an increase in RPTs raises audit fees through multiple pathways, including elevated operational risk, heightened information asymmetry, and governance-related factors. These insights provide a foundation for formulating the research hypothesis:

H1: An increase in related party transactions increases independent audit fees.

Method

This study is an applied research that examines the relationship between related-party transactions and audit fees in companies listed on the Tehran Stock Exchange, using prior theories as a foundation. It uses preexisting archival data to assess relationships among variables without control methods; it is descriptive-correlational. This section contains data collection, sample selection, variable measurement, regression models, analysis techniques, and a more robust justification of the Tehran Stock Exchange (TSE) firms and their relevance to the institutions.

Data Collection and Sample Selection

We used library-based approaches and document analysis to collect data from databases such as Rahavard Novin 3, Codal, TSE, and Iran Fara Bourse (IFB) after the event. The theoretical framework and literature assessment were based on books, academic journals, dissertations, and official reports. Empirical data were sourced from financial statements and related disclosures in the TSE and IFB databases. The statistical population includes all firms listed on the TSE from 2014 to 2024. Several eligibility criteria were applied to ensure data homogeneity and comparability, including the following criteria:

· Companies with a fiscal year other than March ending are excluded.

· The companies that altered their fiscal year within the framework of the research were not included.

· The exclusion of any investment, holding, and financial intermediary firms was because of the structural variation in their reporting on financial accounts.

· Firms that did not publish or had missing information on their finances were restricted.

· Companies that traded with a suspension of over three months were also deleted.

The final sample, after these filters, consists of 163 companies, which is enough to draw strong statistical conclusions and is reflective of previous study standards. The data structure is panel (longitudinal), integrating cross-sectional and time-series data, which enhances control for unobservable heterogeneity and improves the reliability of the results.

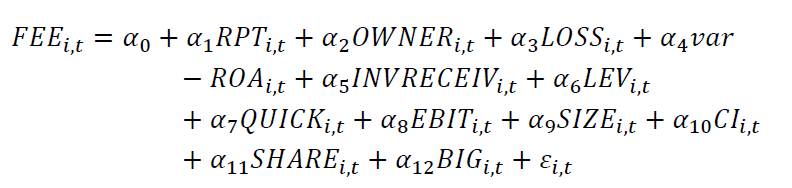

Following Elistratova et al. (2023), this study employs a panel multivariate regression model to examine the effect of related party transactions on audit fees. The data structure is firm-year, and the model is estimated to simultaneously control for firm-specific characteristics and auditor attributes. The empirical model is specified as follows:

Variable Definitions

Dependent Variable

· Audit Fee (FEE): Natural logarithm of the total fee paid to the independent auditor.

Independent Variable

· Related Party Transactions (RPT): Ratio of the total disclosed purchases and sales with related parties to total assets.

Control Variables

· Major Ownership (OWNER): Percentage of shares held by shareholders owning more than five percent (Khatiri et al., 2022).

· Loss (LOSS): Dummy variable equal to one if a loss is reported, and zero otherwise.

· Change in Return on Assets (VAR_ROA): Change in operating profit to total assets compared to the previous year.

· Receivables and Inventory (INVRECEIV): Sum of accounts receivable and inventory divided by total assets.

· Leverage (LEV): Total liabilities divided by total assets.

· Liquidity (QUICK): Cash divided by total assets.

· Profitability (EBIT): Earnings before interest and taxes divided by total assets.

· Firm Size (SIZE): Natural logarithm of total assets.

Auditor-Related Variables

· Client Importance to Auditor (CI): Ratio of the audit fee received from the client to the total fees received by the auditor in the same industry during the same year.

· Auditor Industry Expertise (SHARE): Calculated based on the auditor’s market share in the industry. Market share is defined as the total assets of a firm’s clients audited by a particular auditor in industry k divided by the total assets of all firms in that industry in the same year. An auditor is considered an industry specialist if their market share exceeds a specified threshold based on the number of firms in the industry. The dummy variable SHARE equals one for specialists and zero otherwise.

· Auditor Size (BIG): Dummy variable equal to one if the audit is performed by the Iranian Audit Organization or Mofid Rahbar Institute, and zero otherwise.

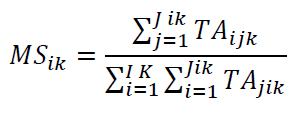

Market share is used as a proxy for the auditor’s industry expertise, reflecting the priority and experience of the auditor in that sector. A higher market share indicates greater industry-specific knowledge and experience relative to competitors. The auditor’s market share is computed as described above.

Auditor Market Share Calculation

The market share of auditing firm i in industry k (MS) is defined as the ratio of the total assets of all clients audited by the firm in that industry to the total assets of all clients in the same industry:

Where:

(MS_{i,k}) = Market share of auditing firm i in industry k

(TA_{j}) = Total assets of client j

I = Identifier of the auditing firm

J = Identifier of the client firm

K = Identifier of the industry

(J_i) = Number of clients of auditing firm I in industry K

Industry Specialist Classification

Auditing firms in this study are considered industry specialists if their market share in the industry satisfies the following condition:

Threshold ≥ MS i,k

Where:

- K= MS i,k Market share of auditing firm i in industry

- N = Total number of firms in industry k

Accordingly, if a firm is audited by an industry-specialist auditing firm, the dummy variable SHARE is assigned a value of one (1); otherwise, it is set to zero (0). This classification captures the relative expertise and experience of the auditor in the industry and is used to examine its influence on audit quality and audit fees.

Results

Descriptive Statistics

As presented in Table 1, the descriptive statistics indicate that the mean change in return on assets (VARROA) is .007, suggesting only marginal growth in firms’ operating performance compared to the previous year. In low-growth conditions, any additional misstatement risk may exert a stronger influence on audit decisions and fee determination, which reinforces the importance of examining the impact of related party transactions on audit risk and audit fees.

The mean ratio of receivables and inventory to total assets (INVRECEIV) is .520, indicating that non-cash current assets constitute a substantial portion of total assets. From an audit risk perspective, these asset categories are typically associated with higher estimation uncertainty and misstatement risk. Firms with higher ratios may therefore require greater audit effort and incur higher audit fees (Elistratova et al., 2023).

Financial leverage (LEV) has a mean of .549, implying that liabilities account for approximately 55 percent of total assets. According to audit risk theory, higher leverage is associated with greater financial complexity and risk, potentially increasing audit effort and audit fees as auditors perform additional procedures to ensure the reliability of financial statements (Bushman & Smith, 2003).

The average liquidity ratio (QUICK) is .046, reflecting limited cash resources. Lower liquidity may expose firms to financial pressure and increase the risk of debt servicing difficulties, thereby affecting audit complexity and fee assessments.

Profitability, measured as earnings before interest and taxes to total assets (EBIT), has a mean of .162. Consistent with financial reporting theory, higher profitability generally signals lower perceived risk and may reduce audit effort and fees, as profitable firms tend to present fewer financial distress concerns (Cao et al., 2024; Hu et al., 2023).

The mean firm size (SIZE) is 14.605. Based on audit complexity theory, larger firms typically have more complex operations, which increases audit effort and, consequently, audit fees (Desender et al., 2013).

Client importance to the auditor (CI) has a mean of .132. This variable reflects the proportion of audit fees received from a specific client relative to the auditor’s total industry fees. Under economic bonding theory, auditors may adjust their level of effort depending on the financial importance of the client (Jiang et al., 2010).

Among the dummy variables, 10% of the firms report losses (LOSS). Approximately 61% of the sample firms are audited by industry specialist auditors (SHARE), and 25% are audited by large and reputable Iranian audit firms (BIG2). Consistent with theoretical expectations, auditor specialization and audit firm capacity may reduce audit risk and enhance audit quality, thereby influencing audit fee determination (Fang et al., 2018).

Overall, the descriptive statistics reveal substantial heterogeneity in financial structure and audit characteristics across sample firms. This variation underscores the importance of examining the relationship between related party transactions and audit fees, as financial conditions and audit attributes may interact with such transactions and alter the underlying risk profile (Kanapathippillai et al., 2024).

Descriptive Statistics of Research Variables

|

Variable |

Symbol |

M |

Mdn |

Max |

Min |

sd |

Observations |

|

Audit Fees |

FEE |

4.67 |

6.32 |

13.47 |

0.00 |

3.53 |

1793 |

|

Related Party Transactions |

RPT |

0.54 |

0.16 |

5.43 |

0.00 |

1.00 |

1793 |

|

Major Ownership |

OWNER |

0.76 |

0.82 |

1.00 |

0.04 |

0.22 |

1793 |

|

Change In Roa |

VARROA |

0.00 |

0.00 |

0.84 |

-0.46 |

0.10 |

1793 |

|

Receivables And Inventory Ratio |

INVRECEIV |

0.52 |

0.51 |

0.96 |

0.00 |

0.19 |

1793 |

|

Leverage |

LEV |

0.54 |

0.55 |

2.07 |

0.01 |

0.22 |

1793 |

|

Liquidity |

QUICK |

0.04 |

0.02 |

0.59 |

0.00 |

0.05 |

1793 |

|

Ebit To Total Assets |

EBIT |

0.16 |

0.13 |

0.84 |

-0.58 |

0.17 |

1793 |

|

Firm Size |

SIZE |

14.60 |

14.38 |

21.32 |

10.16 |

1.71 |

1793 |

|

Client Importance |

CI |

0.13 |

0.01 |

1.00 |

0.00 |

0.25 |

1793 |

Additional Dummy Variables:

· LOSS: Percentage of loss firms = 10%

· SHARE: Industry specialist auditors = 61%

· BIG2: Large audit firms = 25%

Correlation Analysis

Table 2 presents the correlation matrix of the research variables. The results indicate that the correlation between audit fees (FEE) and related party transactions (RPT) is .078. Although relatively small in magnitude, this positive coefficient suggests a weak but direct association between the volume of related party transactions and audit fees. This finding is consistent with audit risk theory, as a higher volume of related party transactions may increase inherent risk and audit complexity, thereby requiring greater audit effort and potentially leading to higher audit fees (Elistratova et al., 2023).

Audit fees (FEE) exhibit the strongest positive correlation with client importance (CI), with a coefficient of .426. This relatively stronger association suggests that as a client’s economic importance to the auditor increases, audit fees also tend to increase. This finding aligns with the economic dependence theory of auditing, which posits that economically significant clients may influence the allocation of audit resources and the level of engagement effort, ultimately affecting fee determination (Jiang et al., 2010). The correlation between audit fees (FEE) and firm size (SIZE) is -.165. This negative relationship indicates that, within the sample, larger firms tend to pay relatively lower audit fees. This result may reflect economies of scale, standardized audit procedures in larger firms, or greater bargaining power. However, a definitive interpretation requires multivariate regression analysis controlling for other firm characteristics. Other control variables—including ownership concentration (OWNER), variability in return on assets (VARROA), receivables and inventory ratio (INVRECEIV), leverage (LEV), liquidity (QUICK), and earnings before interest and taxes (EBIT)—show relatively low correlations with FEE (ranging from -.083 to .002). These low pairwise correlations suggest no strong linear association with audit fees. Nevertheless, the absence of multicollinearity should be confirmed through Variance Inflation Factor (VIF) diagnostics in the regression analysis.

Overall, the correlation analysis indicates that RPT and CI demonstrate the strongest potential association with audit fees, while the remaining variables primarily function as control variables. The observed pattern is consistent with the theoretical framework based on audit risk and the complexity introduced by related party transactions, thereby supporting the study’s empirical model.

Correlation Matrix of Research Variables

|

Variables |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

|

|

1. FEE |

1.00 |

|

||||||||

|

2. RPT |

0.07 |

1.00 |

|

|||||||

|

3. OWNER |

0.02 |

0.09 |

1.00 |

|

||||||

|

4. VARROA |

-0.00 |

0.01 |

-0.00 |

1.00 |

|

|||||

|

5. INVRECEIV |

-0.01 |

0.14 |

0.15 |

0.00 |

1.00 |

|

||||

|

6. LEV |

-0.01 |

0.13 |

0.11 |

-0.09 |

0.26 |

1.00 |

|

|||

|

7. QUICK |

-0.08 |

0.02 |

-0.07 |

0.10 |

-0.10 |

-0.10 |

1.00 |

|

||

|

8. EBIT |

0.00 |

-0.12 |

-0.01 |

0.33 |

-0.05 |

-0.59 |

0.20 |

1.00 |

|

|

|

9. SIZE |

-0.16 |

-0.01 |

-0.10 |

-0.00 |

-0.13 |

-0.07 |

-0.03 |

0.20 |

1.00 |

|

|

10. CI |

0.42 |

-0.07 |

0.00 |

-0.02 |

-0.02 |

-0.01 |

-0.01 |

-0.05 |

-0.11 |

|

Stationarity Test of Research Variables

One of the key assumptions underlying panel regression models is the stationarity of the variables. To examine this property, the Levin, Lin, and Chu (LLC) unit root test was applied to each research variable. The results are reported in Table 3.

As shown in Table 3, the p-values associated with the unit root test statistics for all variables are below the .05 significance level. Accordingly, the null hypothesis of a unit root is rejected for all variables. This indicates that audit fees (FEE), related party transactions (RPT), ownership concentration (OWNER), variability in return on assets (VARROA), receivables and inventory ratio (INVRECEIV), leverage (LEV), liquidity (QUICK), earnings before interest and taxes (EBIT), firm size (SIZE), and client importance (CI) are stationary at their level form.

The stationarity of the variables reduces the risk of spurious regression results and supports the validity of the estimated relationships in the panel regression models. In particular, using stationary variables ensures that the estimated association between related party transactions and audit fees reflects a meaningful economic relationship rather than a common stochastic trend. This methodological consideration strengthens the reliability of the empirical findings (Bushman & Smith, 2003; Elistratova et al., 2023).

Levin, Lin, and Chu (LLC) Unit Root Test Results

|

Variable |

Symbol |

LLC Statistic |

p-value |

Conclusion |

|

Audit Fees |

FEE |

-11.727 |

< 0.001 |

Stationary |

|

Related Party Transactions |

RPT |

-159.286 |

< 0.001 |

Stationary |

|

Ownership Concentration |

OWNER |

-5.942 |

< 0.001 |

Stationary |

|

Variability In Roa |

VARROA |

-32.457 |

< 0.001 |

Stationary |

|

Receivables And Inventory Ratio |

INVRECEIV |

-9.645 |

< 0.001 |

Stationary |

|

Leverage |

LEV |

-15.693 |

< 0.001 |

Stationary |

|

Liquidity |

QUICK |

-27.064 |

< 0.001 |

Stationary |

|

Earnings Before Interest And Taxes |

EBIT |

-12.574 |

< 0.001 |

Stationary |

|

Firm Size |

SIZE |

-10.301 |

< 0.001 |

Stationary |

|

Client Importance |

CI |

-58.063 |

< 0.001 |

Stationary |

Hypothesis Testing

The first research hypothesis examines whether “an increase in related party transactions reduces independent audit fees.” The results of the fixed-effects panel regression model are presented in Table 4.

The overall model is statistically significant (F = 194.639, p < .001). The Durbin-Watson statistic equals 1.826, indicating no serious autocorrelation in the residuals. The Limer test (p < .001) confirms the appropriateness of using panel data, and the Hausman test (p < .001) supports the selection of the fixed-effects model. Variance Inflation Factors (VIF) for all explanatory variables are below 10, indicating no severe multicollinearity. Due to the presence of heteroskedasticity (White test, p < .001), the model was estimated using GLS with White’s robust standard errors. The adjusted R² of 0.984 indicates that approximately 98% of the variation in audit fees is explained by the independent variables.

The regression results show that related party transactions (RPT) have a negative coefficient with audit fees (β = -0.0254), but this effect is not statistically significant (p = .1668). Therefore, the hypothesis that an increase in related party transactions reduces audit fees is not supported in this sample.

Other control variables—including variability in return on assets (VARROA), receivables and inventory ratio (INVRECEIV), leverage (LEV), earnings before interest and taxes (EBIT), firm size (SIZE), client importance (CI), and auditor size (BIG2)—have significant effects on audit fees, highlighting the critical role of financial and audit characteristics in determining fees.

These findings suggest that, within the Iranian economic environment, auditors may set audit fees primarily based on other firm-specific risk factors and financial characteristics, rather than directly on related party transactions. This result differs somewhat from findings in some international studies (Al-Dhamari et al., 2018; Elistratova et al., 2023) and may reflect unique features of Iran’s economic and institutional context, including ownership concentration and regulatory constraints on auditing.

Panel Regression Results for Hypothesis Testing (Fixed Effects Model)

|

Variable |

Symbol |

Coefficient |

Sd Error |

t |

p |

VIF |

|

Related party transactions |

RPT |

-0.02 |

0.01 |

-1.38 |

0.16 |

1.07 |

|

Ownership concentration |

OWNER |

0.13 |

0.09 |

1.43 |

0.15 |

1.09 |

|

Loss |

LOSS |

-0.07 |

0.04 |

-1.65 |

0.09 |

1.34 |

|

Variability in ROA |

VARROA |

0.24 |

0.11 |

2.07 |

0.03 |

1.16 |

|

Receivables and inventory ratio |

INVRECEIV |

0.33 |

0.10 |

3.05 |

0.00 |

1.17 |

|

Leverage |

LEV |

-0.47 |

0.11 |

-4.00 |

0.00 |

1.88 |

|

Liquidity |

QUICK |

-0.18 |

0.24 |

-0.77 |

0.43 |

1.09 |

|

Earnings before interest and taxes |

EBIT |

-0.63 |

0.15 |

-4.14 |

0.00 |

2.27 |

|

Firm size |

SIZE |

0.31 |

0.02 |

15.47 |

0.00 |

1.35 |

|

Client importance |

CI |

8.67 |

0.40 |

21.55 |

0.00 |

1.06 |

|

Auditor industry specialization |

SHARE |

-0.02 |

0.04 |

-0.55 |

0.57 |

1.34 |

|

Auditor size |

BIG2 |

0.38 |

0.05 |

6.43 |

0.00 |

1.19 |

Model Statistics

· Adjusted R² = 0.984

· R² = 0.985

· F-statistic = 194.639 (p < 0.001)

· Durbin-Watson = 1.826

· Limer test = 29.018 (p < 0.001)

· Hausman test = 66.697 (p < 0.001)

· Heteroskedasticity (White test) = 8.431 (p < 0.001)

Conclusion and Suggestions

Audit fees are determined based on the cost of services provided during the audit process and an estimation of potential risks and losses associated with the auditor’s responsibility for the issued financial statements. Multiple factors influence this process, one of which is related party transactions. The present study examined this factor in Iranian listed companies and found that related party transactions do not have a significant effect on audit fees.

Prior literature indicates that auditors play an active monitoring role when related party transactions occur. However, the findings of this study suggest that, in the Iranian economic environment, these transactions do not directly affect the level of audit fees. This outcome can be interpreted from two perspectives: first, audit fees may primarily reflect auditors’ objectives to maintain audit quality rather than the specific conditions of individual firms; second, auditors may, in some cases, be influenced by management, and unusual company activities—including significant related party transactions—may not substantially affect their decision-making.

The results of this study differ from some domestic and international findings. For example, Khatiri et al. (2022) reported a significant positive relationship between related party transactions and unexpected audit fees, while Elistratova et al. (2023) found a negative effect of related party transaction amounts on independent audit fees. These discrepancies may reflect the unique characteristics of the Iranian economic environment, such as limited competition in the audit market, government influence in companies, and constrained effectiveness of corporate governance mechanisms. Consequently, the impact of related party transactions on audit fees in Iran differs from other economic contexts.

Based on these findings, the study proposes the following recommendations:

- Corporate governance mechanisms should be strengthened to ensure that the effects of related party transactions on company processes and decisions are more transparent, enabling stakeholders to accurately assess both the positive and negative consequences of these transactions.

- Future research should separate audit fees into ordinary and extraordinary components and examine the effect of related party transactions on each component individually.

- The moderating role of corporate governance mechanisms in the relationship between related party transactions and audit fees should be tested to clarify the potential impact of internal controls and governance on audit quality and cost.

These recommendations can guide future research on the interaction between related party transactions, audit performance, and corporate governance mechanisms in Iran, ultimately enhancing stakeholder decision-making and improving transparency in financial reporting.

References

Al-Dhamari, R. A., Al-Gamrh, B., Ku Ismail, K. N. I., & Haji Ismail, S. S. (2018). Related party transactions and audit fees: the role of the internal audit function. Journal of Management & Governance, 22(1), 187–212. https://doi.org/10.1007/s10997-017-9376-6

Apostolou, B. A., Hassell, J. M., Webber, S. A., & Sumners, G. E. (2001). The relative importance of management fraud risk factors. Behavioral Research in Accounting, 13(1), 1–24. https://doi.org/10.2308/bria.2001.13.1.1

Beasley, M. S., Carcello, J. V., & Hermanson, D. R. (2001). Top 10 audit deficiencies. Journal of Accountancy, 19(1), 63.

Bell, T. B., & Carcello, J. V. (2000). A decision aid for assessing the likelihood of fraudulent financial reporting. Auditing: A Journal of Practice & Theory, 19(1), 169–184. https://doi.org/10.2308/aud.2000.19.1.169

Bushman, R. M., & Smith, A. J. (2003). Transparency, financial accounting information, and corporate governance. Economic Policy Review, 9(1).

Cheng, Z., Liu, Z. F., Wang, I. Z., & Zhao, X. (2024). Reverse merger audit fee premium: Evidence from China. International Review of Financial Analysis, 94, 103318. https://doi.org/10.1016/j.irfa.2024.103318

Cao, F., Zhang, X., & Yuan, R. (2024). Rookie independent directors and audit fees: Evidence from China. Research in International Business and Finance, 69, 102207. https://doi.org/10.1016/j.ribaf.2023.102207

Darabi, R., & Davoodkhani, M. (2015). The effect of related party transactions on firm value. Financial Accounting and Auditing Research, 7(28), 131–152.

Desender, K. A., Aguilera, R. V., Crespi, R., & García-Cestona, M. (2013). When does ownership matter? Board characteristics and behavior. Strategic Management Journal, 34(7), 823–842. https://doi.org/10.1002/smj.2046

Ding, X., Chourou, L., & Ben-Amar, W. (2024). Carbon emissions and audit fees: Evidence from emerging markets. Emerging Markets Review, 60, 101139. https://doi.org/10.1016/j.ememar.2024.101139

Elistratova, M., Bona-Sánchez, C., & Pérez-Alemán, J. (2023). Related party transactions and audit fees in a dominant owner context. Spanish Journal of Finance and Accounting / Revista Española de Financiación y Contabilidad, 52(2), 294–315. https://doi.org/10.1080/02102412.2022.2058297

Fang, J., Lobo, G. J., Zhang, Y., & Zhao, Y. (2018). Auditing related party transactions: Evidence from audit opinions and restatements. Auditing: A Journal of Practice & Theory, 37(2), 73–106. https://doi.org/10.2308/ajpt-51869

Gordon, E. A., Henry, E., Louwers, T. J., & Reed, B. J. (2007). Auditing related party transactions: A literature overview and research synthesis. Accounting Horizons, 21(1), 81–102. https://doi.org/10.2308/acch.2007.21.1.81

Hu, J., Li, X., & Wan, Z. (2023). Corporate corruption and future audit fees: Evidence from a quasi-natural experiment. Journal of Contemporary Accounting & Economics, 19(3), 100367. https://doi.org/10.1016/j.jcae.2023.100367.

Jiang, G., Lee, C. M., & Yue, H. (2010). Tunneling through intercorporate loans: The China experience. Journal of Financial Economics, 98(1), 1–20. https://doi.org/10.1016/j.jfineco.2010.05.002

Kanapathippillai, S., Yaftian, A., Mirshekary, S., Sami, H., & Gul, F. A. (2024). Director turnover, board monitoring and audit fees: Some Australian evidence. Pacific-Basin Finance Journal, 83, 102246. https://doi.org/10.1016/j.pacfin.2023.102246

Khatiri, M., Ghasemi, A., Darvish Tabar Ahmad Chali, M., & Mehri Namak-Avarani, O. (2022). Related party transactions and unexpected audit fees in loss-making firms: Testing the moderating effect of ownership structure. Financial Accounting Empirical Studies, 19(73), 177–205. https://doi.org/10.22054/qjma.2021.59138.2235

Kushwaha, N. N., Anand, A., Jayadev, M., & Raghunandan, K. (2022). Related party transactions and audit fees: Indian evidence. IIM Bangalore Research Paper, (667), 1–40. https://doi.org/10.2308/AJPT-2022-086

Louwers, T. J., Henry, E., Reed, B. J., & Gordon, E. A. (2008). Deficiencies in auditing related-party transactions: Insights from AAERs. Current Issues in Auditing, 2(2), A10–A16. https://doi.org/10.2308/ciia.2008.2.2.a10

Moyes, G. D., Lin, P., & Landry Jr, R. M. (2005). Raise the red flag: A recent study examines which SAS No. 99 indicators are more effective in detecting fraudulent financial reporting. Internal Auditor, 62(5), 47–52. https://link.gale.com/apps/doc/A138003376/AONE?u=anon~8c0477e5&sid=googleScholar&xid=19fe9acf

Rasheed, P. C. A., & Hawaldar, I. T. (2021). Related party transactions and audit risk. Cogent Business & Management, 8(1), 1888669. https://doi.org/10.1080/23311975.2021.1888669

Salehi, M., Tourchi, M., & Abdollahnajad Khalilabad, R. (2020). The effect of related party transactions on the relationship between political connections and audit delay. Empirical Accounting Research, 10(2), 161–268. https://doi.org/10.22051/jera.2018.19739.1989

Wilks, T. J., & Zimbelman, M. F. (2010). Decomposition of fraud-risk assessments and auditors' sensitivity to fraud cues. Contemporary Accounting Research, 21(3), 719–745. https://doi.org/10.1506/HGXP-4DBH-59D1-3FHJ

Xu, W., & Zhang, P. (2025). Auditor fees and connected transactions. Finance Research Letters, 108092. https://doi.org/10.1016/j.frl.2025.108092

Zhu, X., & Zhao, Z. (2023). A study of related party transactions, operational risks and audit fees from the perspective of the nature of ownership. Proceedings of the 2023 3rd International Conference on Financial Management and Economic Transition (FMET 2023) https://doi.org/10.2991/978-94-6463-272-9_4

Page 1 of

Download Count : 6

Visit Count : 74

Keywords

Related Party Transactions; Audit Fees; Audit Quality; Corporate Governance; Tehran Stock Exchange

Author(s) Information

How to cite this article

Alipour, A. (2025). The impact of related party transactions on audit fees: Evidence from companies listed on the Tehran stock exchange. New Challenges in Accounting and Finance, 14, 33-45. https://doi.org/10.32038/NCAF.2025.14.03

Acknowledgments

Not applicable.

Funding

Not applicable.

Conflict of Interests

No, there are no conflicting interests.

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/