Original Research

Are the RD Costs Significant for the Company’s Market Value in a Normal (Non-Crisis) Decade? – Evidence From the Athens Stock Exchange

- Abstract

- Full text

- Metrics

This article examines the influence of research and development costs on the market value of the business. Based mainly on the Sougiannis model (1994), with data from the Athens stock exchange and listed companies, for the period following the adoption of the International Financial Reporting Standards (2005-2012), an attempt is made to understand the culture on the part of companies and investors about these costs as well as whether the investment in these costs is made consciously with the long-term aim of developing, or linked to the tax benefit they offer.

Are the RD Costs Significant for the Company’s Market Value in a Normal (Non-Crisis) Decade? – Evidence From the Athens Stock Exchange

Emmanouil D. Gkinoglou

University of Western Macedonia, Department of International and European Economic Studies, Koila Kozanis, Greece

ABSTRACT This article examines the influence of research and development costs on the market value of the business. Based mainly on the Sougiannis model (1994), with data from the Athens stock exchange and listed companies, for the period following the adoption of the International Financial Reporting Standards (2005-2012), an attempt is made to understand the culture on the part of companies and investors about these costs as well as whether the investment in these costs is made consciously with the long-term aim of developing, or linked to the tax benefit they offer. |

Keywords: RD, IFRS, Accounting, Intangible Assets, Taxation, Market Value |

Introduction

Over the last 20 years, more and more talk has been made about the concept of intangible assets of an economic unit. A theoretically high turnover, when accompanied by higher than the industry average after-tax profits, indicates the proper management of intangible assets, contributing to the formation of the primary price or the saving of production costs. These companies hold valuable assets, which, of course, are not the materials that all competing companies can acquire. [1]

All intangible assets, like all business assets, can only grow and deliver profits if funds are made available for research and renewal of the technologies they use. Further investment by the company is therefore required to return the asset in question. If, for example, an undertaking reduces advertising costs for only one year, this would have the effect of improving the profit and loss situation by showing higher profits (Fotidou et al., 2007; Fajaria & Isnalita, 2018; Alshehadeh et al., 2024).

Research and development costs

The issue that arises comes from the accounting field and is the achievement of a reliable link between costs and revenues. Given that many intangible assets have future benefits, the basic accounting principle of accrued output and the accounting principle of the periodic cost-income link seems to be in trouble. A typical example is the research and development costs or advertising costs. When these two categories of expenses occur in the business, they are treated as expenses even if future profits from this outflow are expected.[2]

The costs of the research and development of the company, the problems that exist with regard to their accounting treatment, as well as the costs of projecting and consolidating the name of the company, are also present here.[3]

Bushee (1998) found that, oftentimes, companies and investors do not judge research and development costs as a tool for the development of the business.

Ultimately, most research suggests that intangible assets are difficult to identify with a clear and specific definition and often need to be described in more general terms (Edvinsson & Malone, 1997; Stewart, 1998; Bontis et al., 1999; Lev, 2001; Sullivan, 2000, Sanchez et al., 2000; Ordonez de Pablos, 2003; Blair & Wallman, 2001), contribute to the value of the business (Edvinsson & Malone, 1997; Petty & Guthrie, 2000; Sullivan, 2000; Lev, 2001, Gu & Lev, 2001) while also having an impact on the future profits of the company (Edvinsson & Malone, 1997; Stewart, 1998; Blair & Wallman, 2001; Lev, 2001). However, there is also the opposite view (Upton, 2001; Emmanouil & Dimitrios, 2017), which, despite the dispute over recognition as an asset of the company, agrees that they are in possession of the business with a view to its development and ultimately the effect on future profits.

Below, an effort is made to understand the mentality of the administrations of Greek-listed companies regarding the treatment of research and development costs. In other words, if the administrations of Greek companies consider that by investing in research, the company will develop. Also, if investors consider that a company that respects itself, its customers, and its investors, should not rest on existing ones but constantly strive to grow through research by improving their services and products to consumers.

So, there is an approach to whether and to what effect investors respond positively to the decision to spend on research and technology on the part of companies and, ultimately, whether this has an impact on a higher market value or a higher share price. This effort is made considering the peculiarities presented by the Greek money market over the last decade, peculiarities such as the nature and type of Greek companies, the adoption for the application of International Accounting Standards in the representation of their transactions, and other important factors, such as the global and domestic economic crisis.

Literature review

Sougiannis (1994) correlates market value with book value, profits, and research and development costs. The findings of Sougiannis (1994) are that the profit model it calculated shows that the research and development costs adjusted for research and development costs reflect the real benefits of research and development costs. In fact, it found that an increase of one dollar in research and development leads to an increase of two dollars over a seven-year period; that is, investors seem to consider investing in research and development costs too important; this effect of research and development costs on market value can be divided into indirect and direct; essentially, the information on research and development costs provided by profits is more reliable than the variables of costs and development. When companies use them for tax purposes, an increase in research and development costs increases operating costs, and these, in turn, reduce the gross result and, ultimately, the net result, reducing profits or increasing losses accordingly.

Green et al. (1996), using data from the United Kingdom market, examined the relationship between research and development costs and market value based on accounting results. This survey shows the significant impact of residual income on the market value of the company, and that research and development costs are not significant and reliable. This may be because there is a relatively small sample (1990-1992).

Bushee (1998) and Xue and Zhang (2020) examined how research and development costs are treated, i.e., whether they are used for the profitability of the company or are used for tax benefit and profit manipulation, choosing not to carry out research and development costs in order to reverse losses and ultimately to show profits in the annual financial statements.

Stark and Thomas (1998) and Sougiannis (1994) examined the relationship between residual income and the market value of the company. Using data from the United Kingdom, they found a strong positive relationship between residual income and market value, combined with research and development costs and book value, rather than the relationship between profits and market value, combined with research and development costs and book value.

Hall and Oriani (2006) used data from European countries, France, Germany and Italy. Shah et al. (2007) found a positive and statistically significant relationship and impact of research and development costs on company market prices for both manufacturing and non-manufacturing enterprises. Wyatt (2008) does not clearly note the impact of research and development costs on the market value of the company.

Franzen and Radhakrishnan (2009), extending the Ohlson residual income model (1995), concluded that there is a positive link between research and development costs and share prices for loss-making companies, while they found a negative relationship for companies that were making profits, in other words, it seems that companies were using research and development costs as a tool to reduce their profits (profit manipulation) perhaps because of tax benefits, which Sougiannis (1994) and Bushee (1998) pointed out, while at the same time, investors realized this and continued to invest resulting in an increase in the company's price.

Brown et al. (2009) did not find that research and development funding creates a potentially important channel for linking financing and economic development without directly proving that the economic impact is significant in affecting research and development costs. Pandit et al. (2011) and VanderPal (2015) examined the productivity of companies in patents and the effect on the volatility of their profits. In this logic, therefore, they found that the future operating profits of the company are positively correlated with the quality of their patents, and this relationship is more important for productive and innovative enterprises. It was also found that the volatility of future operating profits is negatively correlated with the quality of patents and this relationship is important for companies that show high amounts in research and development costs and own a number of patents. In other words, companies with research and development costs are more productive and less volatile in their future profits.

Tsolingas and Tsalaboutas (2011) argue that the adoption of IFDs also has an impact on the assessment of research and development costs in the case of the United Kingdom, while Duqi and Torluccio (2011) and Pazarzi and Sorros (2018) found a significant positive and strong impact of research and development costs on the market value of the company.

Based, in particular, on the methodology followed by Sougiannis (1994), it is attempted to determine whether investors consider the expenditure of undertakings in research and development positive and whether the value of the company on the money market is linked to those costs or whether the value of the business is linked to other factors (e.g., taxation).

Sample selection and description

The sample used for the analysis comes from Greek companies that were listed during the period considered on the Athens Stock Exchange. [4]

Model sougiannis

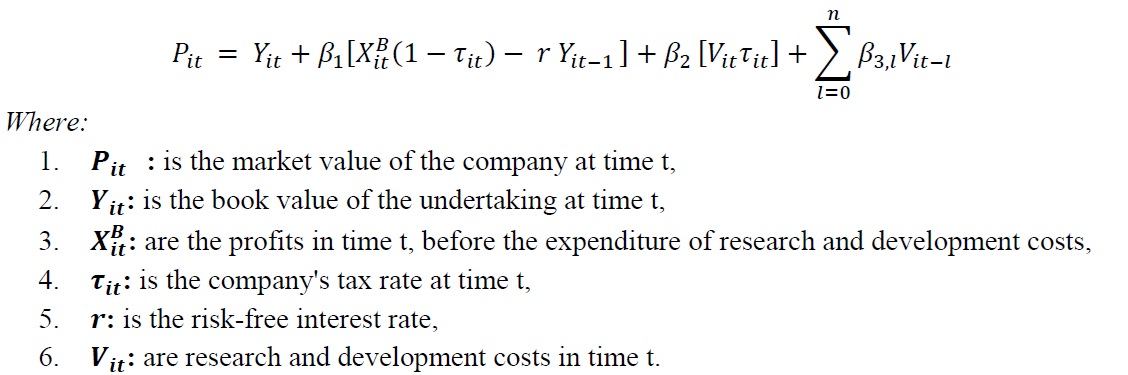

Sougiannis (1994), in his analysis,[5] developed a model based on book valuation, showing that based on the net surplus relationship, the enterprise's market value appears as a function of book value and residual income. Sougiannis was based on Ohlson's original model.

Sougiannis's analysis (1994) focuses on separating research and development costs from profits to show how research and development costs are valued as an element of profits. Last year's research and development costs, which may be significant for the value of the business, should be considered.[6]

Based on all the above, the function takes the following form:

The market value, i.e., is shown as a function of book value, resident income, research and development costs, and tax benefits they offer both in the current and previous years.

As in previous studies (e.g., Kothari & Shanken, 2003), weighting all model variables with book value is used to reduce the problem of heteroskedasticity. To check the robustness of the model and results, other variables were used as deflators, such as market value, book value t-1 and market share.

The problem of the false-false correlation (spurious correlation) due to the common denominator, first mentioned by Lev and Sunder (1979), is not a problem for this model, because the denominator is one of the variables of the model (Maddala & Singh, 1977, Sougiannis, 1994).

The function, therefore, after weighing all variables with book value, takes the form of:

Factor a includes the effects of all those variables not included in the function.

Based on Sougiannis (1994), b0 is expected to be zero coefficients b1 and b2 should be positive and the following sum can be positive, negative or zero.

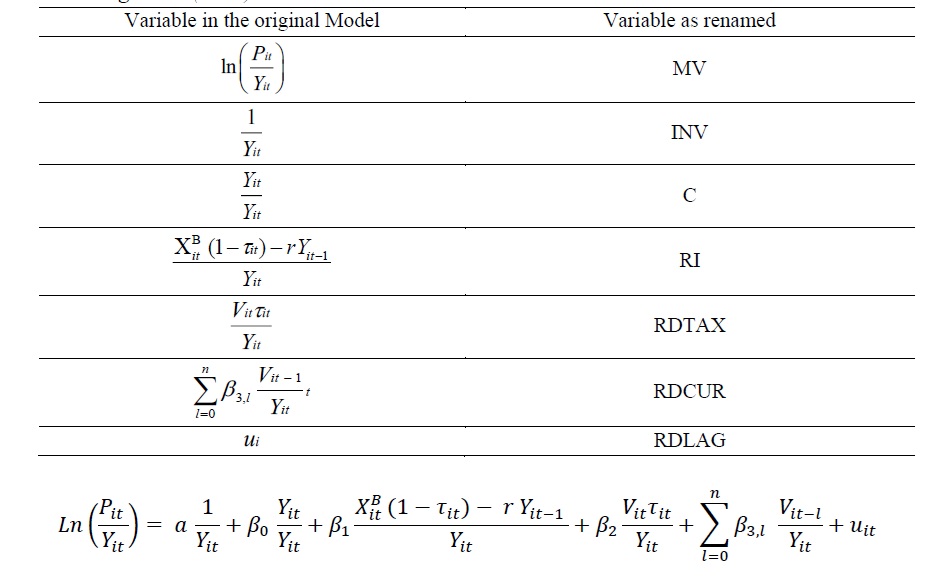

For convenience in this article, the variables will be renamed with this mapping to the variables in the original master, as shown in Table 1:

Table 1

Model Sougiannis (1994)

Statistical analysis of the sample

The following is the sample of the undertakings concerned used in the analysis.

The period initially considered is the entire period after the adoption of International Financial Reporting Standards until 2012. The year 2012 is chosen because it is the second year in which the Greek economy is mired in the economic crisis. In particular, the years 2010-2012 are the worst in terms of shrinking the Greek economy, while from next year, policy changes are already taking place, with the signing of a Memorandum of Cooperation of the Medium-Term Programme 2013-2016, where Greece is beginning to escape the economic quagmire. Given that the publication of the results of the listings on the Athens Stock Exchange was officially introduced in Greece for the year 2005, i.e., from 01/01/2005, they should be excluded from this study in 2003 and 2004, as there would be a disparity in the sample under consideration, due to selective publication with the International Financial Reporting Standards, in those years. For the above reasons, the periods from 2006 to 2012 will be used to examine the two above models.

Firstly, it is important to observe the nature of the companies operating on the Athens Stock Exchange. Greek companies are largely owned by traditional economic sectors such as trade or consumer goods and, to a lesser or lesser extent, by high-tech sectors.

Of the 249 enterprises for the study years (seven years for the Sougiannis model), only undertakings that have presented in some years or have continued to show research and development costs in all years are selected. Finally, a sample of 38 companies for the Sougiannis model (1994) was formed, which presented only 135 observations instead of 1,992 observations, which would be as expected if all the undertakings had all the years under consideration, research, and development costs.

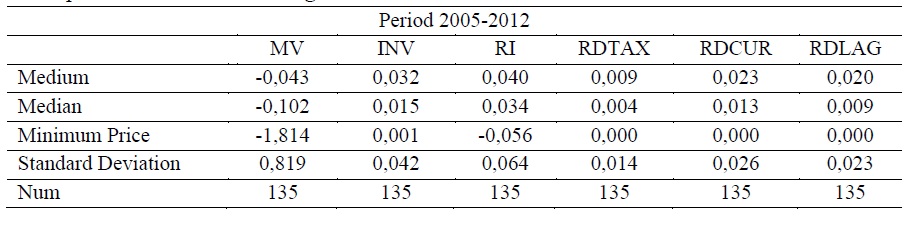

Table 2 includes the analysis of the data based on the Sougiannis model for the whole period considered with 135 observations.

Table 2

Descriptive Model Statistics Sougiannis

Firstly, what is observed, without always being absolute, is that these results may be due to the small number of observations compared with similar surveys (Sougiannis, 1994; Bushee, 1998; Green et al., 1996; Hall & Oriani, 2006; Anagnostopoulou & Levis, 2008; etc.) which took place in other European markets but also in the American market, where companies investing in research and development are significantly more, compared to the Greek stock exchange (e.g., Anagnostopoulou & Levis, 2008, use data from the period 1990-2003, while Sougiannis uses US market data from 1975 to 1985).

An effort is being made to examine the relationship between research and development costs of both the current and last year, the tax benefits they offer, the book value, and the residual income with the market value of the company, based on the Sougiannis model (1994).

Initially, what is being sought is whether, in the sample of companies investing in research and development costs, the companies that spend the most on research and development also have a higher market value. In other words, the market recognizes the investment made by large enterprises, and the more they invest in research and development, the more positively this is judged.

Research hypotheses

In the models developed in the international literature, followed by this research, the market value is shown as a linear relationship of book value, residual income, and research and development costs. Like the view of Ohlson (1995), Sougiannis (1994), Green et al. (1996), Stark and Thomas (1998), Duqi and Torluccio (2011), only research and development costs incurred in the current financial year affect the market value, since the costs incurred in the previous financial year have already been used and produced fixed assets and their performance is shown in residual income.

Η0: Residual Income has a positive impact on the Market Value of the Company

If this is the case in the case of the Greek market, the residual income should be statistically significant and positively correlated with the market value of the company. In other words, if the coefficient of the independent variable RI/BV is statistically significant and positively correlated, then the research hypothesis cannot be rejected.

An effort is also being made to investigate the factors affecting the decision of investors as well as the market value of a business. Griliches (1981), Hirschey (1982), Cockburn and Griliches (1987), Sougiannis (1994), Duqi and Torluccio (2011), and Hall and Oriani (2006) are just some of the studies that found a positive relationship between research and development costs and the market value of the company, although the inclination factors differ between the different studies whether they are European countries (Blundell et al., 1999; Mulkay & Mairese, 2003; Bond et al., 2003; Hall & Oriani, 2006; Anagnostopoulou & Levis, 2008; etc.) or for non-European economies (Sougiannis, 1994; Hall, 1999; Mulkay & Mairesse, 2003; La Porta et al., 1998, 2000; Aboody & Lev, 2000; Hall & Oriani, 2006), by investing in research and development costs.

Similar results are expected for the Greek stock exchange. That means that a positive relationship between research and development costs and the market value of the company is expected. So, our next research hypothesis is:

Η1: Research and development costs have a positive impact on the value of the business

For the above assumption to apply, the coefficient of the variable expressing research and development costs must be positive and statistically significant from the model we use. Therefore, if the analysis shows that the coefficient of the specific independent variable shown as RDCUR is positive and statistically significant, then the research hypothesis cannot be rejected.

Otherwise, which is not the case, this does not mean that research and development costs are not of particular importance to investors and do not have an impact on market value. This means that they are treated myopically by investors and not as a tool for business development.

Below, the empirical results of the listed companies in the C.A.A. -A.S.E are analyzed, and the results of the research cases found in the case of Greece are reported.

Analysis of empirical results

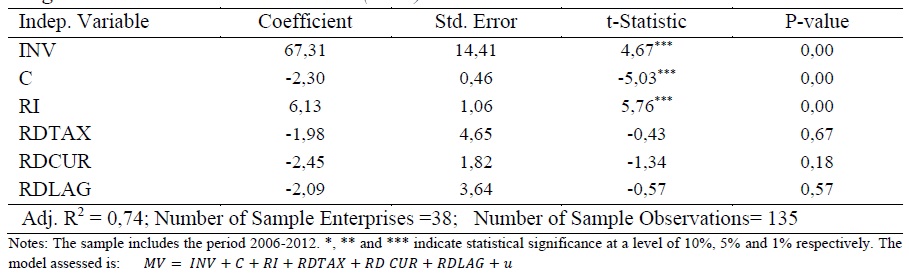

Using the above models and according to the data obtained from the Greek stock exchange, the results are shown below in Table 3.

Table 3

Sougiannis Model Assessment Results (1994)

Table 3 shows the data for the whole period considered, i.e., it contains a total of 135 observations. As shown in the table, the statistically significant variables at a level of less than 1% are the (RI-Resident Income), with a gradient factor of 6.13.

There does not appear to be a strong, positive relationship between market value and research and development costs for the current or previous year (RDCUR and RDLAG, respectively). This means that it does not provide investors with additional market value information on any of the above variables.

Equally important is that the C constant is statistically significant at a level of 1%. This suggests that there are other factors that significantly affect the market value but are not included in the model under consideration. We observed that the other terms are either not statistically significant or marginally not statistically significant.

There are several important conclusions that emerge from the processing of the model. As shown by the factor R2, the percentage of the dependent variable interpreted by the set of independent variables is 82%, indicating a satisfactory interpretation of the sample.

What investors ultimately consider important and positively related to market value is residual income (RI) as well as constant C, which includes other variables that are not considered by this model.

Therefore, as is apparent from the above analysis, research hypothesis H0 is confirmed, while at the same time, research hypothesis H1 is rejected since it is not apparent that investors pay particular attention to the relationship between research and development costs and the market value of the company.

Additional deflators were used to check the reliability of the model other than the book value: (a) the book value at time t-1, i.e., the previous year, (b) the market value in the previous year t-1, and (c) the number of shares (market share). The results obtained are exactly the same, i.e., showing a statistically significant factor, which, according to investors, affects the market value of the company, the residual income.

As variables affecting the market value of the business, it is not the amount a company spends on research costs but only residual income and other factors, as shown by the constant (C), which are not considered in this model. However, the specific variables examined for research and development costs for either the current or previous financial year do not appear to be statistically significant and do not provide additional information to investors who continue and do not consider that companies are using these costs for the tax benefit they are offering.

From the analysis of the data of the listed companies in the C.A.A., what emerges is that investors judge the residual income positively, whereas they consider that this relates to the market value of the company. However, in other countries, investors consider statistically significant and positively correlated with the market value of the company the research and development costs incurred in the current financial year.

Conclusions

With the application of international accounting standards and, in particular, Standard 38, very specific conditions for the recognition of intangible assets have now become very specific for research and development costs. By the above standard, the conditions are laid down, which, if they are not met, then such costs should be deducted from the revenue at the time they are incurred.

In the case of research and development costs, several investigations have been carried out to examine their contribution to the value of the business. Most surveys agree that the costs incurred in this direction because they have a growth objective and character contribute positively most of the time to the valuation of the market value of the company by investors. In particular, from findings in various financial markets such as the United States, the United Kingdom, and other European countries (Germany, France, Italy), what is concluded is the positive response of investors to the market value of those companies whose administrations choose to engage in research.

On the other hand, looking at whether and at what level there are corresponding mentalities and investor responses to the companies of the Greek stock exchange, we see a difference of opinion. The nature and object of Greek businesses, the Greek mentality of short-term strategies, the Greek tax regime, which is unstable and therefore unattractive for stable decisions and strategic investments but above all, the global financial crisis, which also affected the Greek economy, are among the most important factors on which differences in the treatment of research and development costs are based. Regarding the nature of Greek enterprises, the majority of them belong to sectors with low intensity in research. Thus, the sectors that make up the Greek stock exchange are of little expense to research and development costs. This suggests, in the absence of a background, that enterprises should make positive use of any efforts at research in the field of development. In other words, where, in the general environment, undertakings that, by their nature, must be active in the field of research (pharmaceutical, aeronautical, oil, high-tech, etc.) are not included, then the others have the wrong picture of the benefit of investing in research, and there is also a lack of competition, which would contribute to the overall development of the level of operation and organization of even existing enterprises.

The findings from the Greek money market, for the period from the mandatory adoption of IFDs, show that investors do not recognize additional information content in research and development costs and do not associate them with the high market value of the company while it appears a strong link between residual income and the market value of the company, instead of research and development costs as expected. The case for reducing research and development costs is either when the economy is not at a growth rate but is in recession with a decline in GDP, as in the last three years, and when, again, due to recession, businesses see their total annual sales decline. To ensure their sustainability and not lead to economic decline, they are therefore reduced by these costs.

Further study could be to unblock the tax liability for research and development costs, i.e., to disconnect them from the reduction in taxable income. This will show which companies really support their hopes for growth in research and development costs and which companies use them as a tool to beautify their final tax outcome. Moreover, comparing the period of economic recession with the periods after the early signs of recovery of the Greek economy (2015-2019) would be particularly interesting, up to the period when it is interrupted due to the COVID-19 pandemic (2019-2020).

References

Aboody, D., & Lev, B. (2000). Information asymmetry, R&D, and insider gains. The Journal of Finance, 55(6), 2747-2766. https://doi.org/10.1111/0022-1082.00305

Alshehadeh, A. R., Elrefae, G. A., Qirem, I. A., Hatamleh, H. M., & Al-khawaja, H. (2024). Impact of profitability on investment opportunities and its effect on profit sustainability. Uncertain Supply Chain Management 12(2), 871-882. http://dx.doi.org/10.5267/j.uscm.2024.1.001

Anagnostopoulou, S. C., & Levis, M. (2008). R&D and performance persistence: Evidence from the United Kingdom. The International Journal of Accounting, 43(3), 293-320. http://dx.doi.org/10.1016/j.intacc.2008.06.004

Blair, M. M., & Wallman, S. M. H. (2001). Unseen Wealth – Report of the Brookings Task Force on Intangibles. The Brookings Institution. Washington 2001.

Blundell, R., Griffith, R., & Reenen, J. (1999). Market Share, Market Value and Innovation in a Panel of British Manufacturing Firms. Review of Economic Studies, 66(3), 529-554. https://doi.org/10.1111/1467-937X.00097

Bontis, N., Dragonetti, N. C., Jacobsen, K., & Roos, G. (1999). The knowledge toolbox: A Review of the tools available to measure and Manage Intangible Resource. European Management Journal, 17(4), 391-402. https://doi.org/10.1016/S0263-2373(99)00019-5

Bond, S., Harhoff, D., & Van Reenen, J. (2003). Corporate R&D and productivity in Germany and the United Kingdom. Monograph (Discussion Paper). http://eprints.lse.ac.uk/id/eprint/770

Brown, J. R., Fazzari, S. M., & Petersen B. C. (2009). Financing Innovation and Growth: Cash Flow, External Equity, and the 1990s R&D Boom. The Journal of Finance, 64(1), 151-185. https://doi.org/10.1111/j.1540-6261.2008.01431.x

Bushee, B. J. (1998). The Influence of Institutional Investors on Myopic R&D Investment Behavior. The Accounting Review, 73(3), 305-333. https://www.jstor.org/stable/248542

Cockburn, I., & Griliches, Z. (1987). Industry Effects and Appropriability Measures in the Stock Markets Valuation of R&D and Patents. National Bureau of Economic research, Working Paper Series.

Duqi, A., & Torluccio, G. (2011). An analysis of the R&D effect on stock returns for European listed firms. European Journal of Scientific Research, 584, 482-496. https://ssrn.com/abstract=1971159

Edvinsson, L., & Malone, M. S. (1997). Intellectual Capital-the Proven way to establish your company’s real value by measuring its hidden brainpower (p. 22). Judy Piatkus Ltd, London.

Emmanouil, G., & Dimitrios, G. (2017). The Impact of Intangible Assets on Firms Earnings Profitability: Evidence from the Athens Stock Exchange (ASE). Archives of Business Research, 5(8), 50-62. http://dx.doi.org/10.14738/abr.58.3502

Fajaria, A. Z., & Isnalita (2018). The Effect of Profitability, Liquidity, Leverage and Firm Growth of Firm Value with its Dividend Policy as a Moderating Variable. International Journal of Managerial Studies and Research (IJMSR), 6(10), 55-69. http://dx.doi.org/10.20431/2349-0349.0610005

Fotidou, A., Ginoglou, M., & Pestriva, K. (2007). Advertisement Program: An Expense or an Intangible Asset for the Company. Proceedings 5th New Horizons in Industry, Business and Education, Rhodes.

Franzen, L., & Radhakrishnan, S. (2009). The value relevance of R&D across profit and loss firms. Journal of Accounting Public Policy, 28(1), 16-32. http://dx.doi.org/10.1016/j.jaccpubpol.2008.11.006

Green, J. P., Stark, A. W., & Thomas, H. M. (1996). UK Evidence on the market valuation of research and development expenditures. Journal of Business Finance & Accounting, 23(2), 191-216. http://dx.doi.org/10.1111/j.1468-5957.1996.tb00906.x

Griliches, Z. (1981). Market value, R&D, and patents. Economics letters, 7(2), 183-187.

Gu, F., & Lev, B. (2001). Intangible Assets- Measurement, Drivers, Usefulness. Working Paper, Boston University, New York University. http://dx.doi.org/10.4018/978-1-60960-071-6.ch007

Hall, B. H. (1999). Mergers and R&D revisited, Prepared for the Quasi-Experimental Methods Symposium, Econometrics Laboratory, UC Berkeley.

Hall, B. H., & Oriani, R. (2006). Does the market value R&D investment by European firms? Evidence from a panel of manufacturing firms in France, Germany, and Italy. International Journal of Industrial Organization, 24(5), 971-993. https://doi.org/10.1016/j.ijindorg.2005.12.001

Hirschey, M. (1982). Intangible capital aspects of advertising and R & D expenditures. The Journal of industrial economics, 30(4), 375-390.

Kothari, S. P., & Shanken, J. (2003). Time-series coefficient variation in value-relevance regressions: A discussion of Core, Guay, and Van Buskirk and new evidence. Journal of Accounting and Economics, 34(1-3), 69-87.

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., & Vishny, R. (1998). Law and finance. Journal of Political Economy, 106(6), 1113-1135. https://doi.org/10.1086/250042

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of Financial Economics, 58(1-2), 3-27. https://doi.org/10.1016/S0304-405X(00)00065-9

Lev, B. (2001). Intangibles- Management, Measurement and Reporting. the Brookings Institution, Washington, DC.

Lev, B., & Sunder, S. (1979). Methodological Issues in the Use of Financial Ratios. Journal of Accounting and Economics, 1, 187-210. https://doi.org/10.1016/0165-4101(79)90007-7

Maddala, G. S., & Singh, S. K. (1977). A flexible functional form for Lorenz curves. Économie Appliquée, 30(3), 481-486.

Mulkay, B., & Mairesse, J. (2003). The Effect of the R&D Tax Credit in France. EEA-ESEM Conference.

Ohlson, J. (1995). Accounting earnings, book value and dividends: The theory of the clean surplus equation. Contemporary Accounting Research, 11(2), 661-687. https://doi.org/10.1111/j.1911-3846.1995.tb00461.x

Ordonez de Pablos, P. (2003). Intellectual Capital reporting in Spain: a comparative review. Journal of Intellectual Capital, 4(1), 61-81. https://doi.org/10.1108/14691930310455397

Pandit, S., Wasley, C. E., & Zach, T. (2011). The Effect of Research and Development (R&D) Inputs and Outputs on the Relation between the Uncertainty of Future Operating Performance and R&D Expenditures. Journal of Accounting, Auditing & Finance, 26(1), 121-144. https://doi.org/10.1177/0148558X11400583

Pazarzi, G., & Sorros, J. (2018). The effect of R&D expenses on earnings and market value. SPOUDAI: Journal of Economics and Business, 68(2/3), 39-47. https://hdl.handle.net/10419/195213

Petty, R., & Guthrie, J. (2000). Intellectual Capital Literature Review-Measurement, Reporting and Management. Journal of Intellectual Capital, 1(2), 155-176. https://doi.org/10.1108/14691930010348731

Sanchez, P., Chaminade, C., & Olea, M. (2000). Management of Intangibles- an attempt to build a theory. Journal of Intellectual Capital, 1(4), 312-327. https://doi.org/10.1108/14691930010359225

Sougiannis, T. (1994). The Accounting Based Valuation of Corporate R&D. The Accounting Review, 69(1), 44-68. https://www.jstor.org/stable/248260

Shah, S., Stark, A. W., & Akbar, S. (2007). Firm Size, Sector and Market Valuation of R&D Expenditures. Applied Financial Economics Letters, 4(2), 87-91. https://doi.org/10.1080/17446540701537756

Stark, A. W., & Thomas, H. M. (1998). On the Empirical Relationship between Market Value and Residual Income in the U.K. Management Accounting Research, 9(4), 445-460. https://doi.org/10.1006/MARE.1998.0088

Stewart, T. A. (1998). Intellectual Capital- the new wealth of organization, N. Brealey (ed.), (1st ed.). Publishing, London.

Sullivan, P. H. (2000). Value-Driven Intellectual Capital- How to Convert Corporate Assts into Market Value (p. 228). Wiley, New York, NY.

Tsolingas, F., & Tsalavoutas, I. (2011). Value Relevance of R&D in the UK after IFRS mandatory implementation, Applied Financial Economics, 21(13), 957-967. https://doi.org/10.1080/09603107.2011.556588

Upton, W. S. (2001). Business and Financial Reporting, Challenges from the New Economy. Special Report FASB. http://pi.lib.uchicago.edu/1001/cat/bib/4442962

VanderPal, G. A. (2015). Impact of R&D expenses and corporate financial performance. Journal of Accounting and Finance, 15(7), 135-149. https://ssrn.com/abstract=2959290

Xue, H., & Zhang, X. (2020). Investor Sentiment, Institutional Investors and Corporate Innovation Investment —Evidence with Different Ownership Structure from China. Theoretical Economics Letters,10(5), 1166-1192. http;//doi.org/10.4236/tel.2020.105069

Wyatt, A. (2008). What Financial and Non-Financial Information on Intangibles is Value Relevant? A Review of the Evidence. Accounting and Business Research, 38(3), 217-256. https://doi.org/10.1080/00014788.2008.9663336

[1]An example of the benefits of intangible assets is the patenting of a patent, a good working climate resulting from management, with which the company can save resources. Thus, the company can gain a higher price for its product and a higher market share since the optimal production volume is achieved, which leads to increased profits.

[2]Particularly in the case of advertising costs, when it comes to consolidating the name of the company, they should not be treated as expenses, since their financial results for the company are seen over time and not directly. thus, infringing the accounting principle of associating revenue with output.

[3]These costs are not related to future income generated in the company, in breach of the accounting principle of exit income.

[4]The data used were obtained from COMPUSTAT databases and from the C.A.A. From all undertakings, those with a sectoral accounting plan or a specific one was excluded and therefore could not be directly comparable. The period under consideration concerns the years in which Greek companies listed in the C.A.A. publish their financial statements compulsorily based on International Financial Reporting Standards (IAS). B.C.P. The period under consideration is limited to eight years and starts from 2005 to 2012., research and development costs are required during the n-1 period. Thus, the analysis of the sample, modeled on Sougiannis (1994), starts from 2006 and runs until 2012,

[5]For the analysis of his model, Sougiannis relied on Ohlson's model, as detailed in the working paper, which was released in 1989, entitled "Accounting Earnings, book value and dividends: The theory of the clean surplus equation ", Columbia University, New York, NY. Later, Ohlson incorporated this example, which he enriched by taking the final form, in his work (1995), "Accounting earnings, book value and dividends: The theory of the clean surplus equation ", Contemporary accounting research, Volume 11, Issue Ue 2, pages 661-687.

[6] Previous studies, such as those of Cockburn and Griches (1987) and Hall (1999), found that the previous year's research and development costs are significant for the value of the business.

Page 1 of

Download Count : 60

Visit Count : 337

Keywords

RD; IFRS; Accounting; Intangible Assets; Taxation; Market Value

Author(s) Information

How to cite this article:

Gkinoglou E. D. (2024). Are The RD Costs Significant for The Company’s Market Value in a Normal (Non-Crisis) Decade? – Evidence From the Athens Stock Exchange. New Challenges in Accounting and Finance, 11, 1-13. https://doi.org/10.32038/NCAF.2024.11.01

Acknowledgments

Not applicable.

Funding

Not applicable.

Conflict of Interests

No, there are no conflicting interests.

Open Access

This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. You may view a copy of Creative Commons Attribution 4.0 International License here: http://creativecommons.org/licenses/by/4.0/